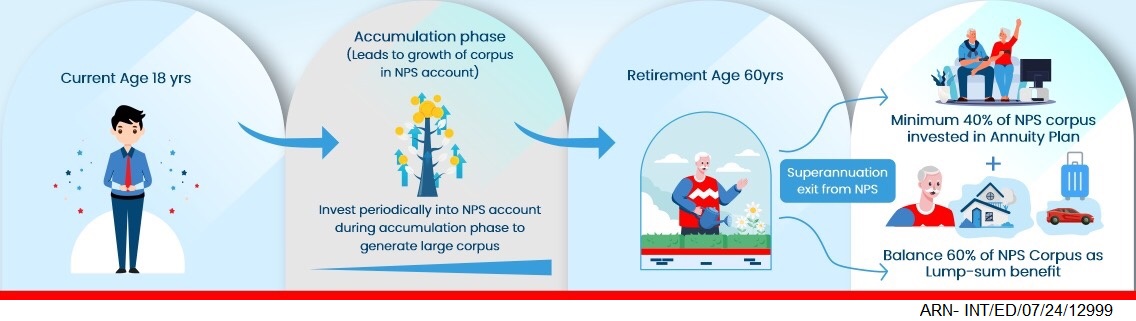

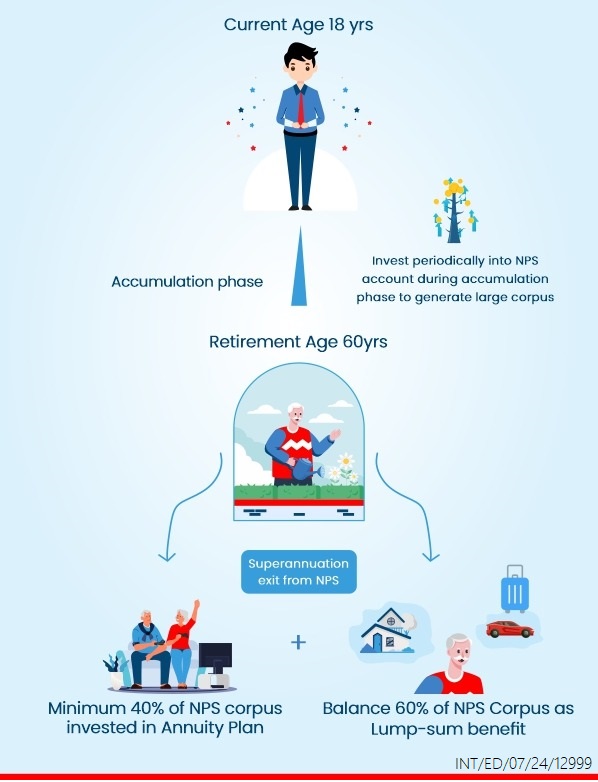

Factors Affecting Annuity Rates in NPS

Annuity rates are the primary benchmark used to calculate your lifelong pension income from the accumulated NPS corpus. These rates are not fixed; they fluctuate based on prevailing economic conditions, the specific annuity plan you select, and the pricing strategy of your chosen insurer. Understanding these variables is essential to predicting your future financial stability.

Interest Rate Conditions

Annuity rates are heavily influenced by prevailing interest rates at the time of purchase. Since insurers invest your corpus in long-term fixed-income securities to fund your pension, higher market interest rates generally translate to higher annuity payouts. Conversely, in a low-interest-rate environment, the same corpus will generate less income.

For example, a ₹50 lakh corpus might yield an annual pension of ₹3.5 lakh at a 7% annuity rate, but only ₹3 lakh if the rate drops to 6% due to economic shifts.

Type of Annuity Chosen

The annuity option you choose directly affects your payout. Each option varies based on risk and benefits. A Life Annuity (single life) usually offers the highest monthly payout. This is because payments stop after the subscriber’s death.

Options like Joint Life or Annuity with Return of Purchase Price (ROP) offer lower payouts. These include added benefits. For example, payments may continue for a spouse, or the purchase amount may be returned to the nominees. This means you trade a higher immediate pension for better long-term financial security for your family.

Annuity Provider Terms

Annuity rates are not uniform across the industry; they differ among the various PFRDA-approved Annuity Service Providers (ASPs). Each provider utilises its own mortality assumptions, administrative cost structures, and investment yields to price their products.

Recent data shows that rates can vary by 50 to 100 basis points between different insurers for the same plan type. Given current market trends, comparing quotes is vital, as even a 0.5% difference in the annuity rate can result in a significant cumulative income difference over a 20-year retirement period.

Age at the Time of Annuity Purchase

Your age at the time of purchasing the annuity is a critical determinant of the rate offered. Generally, the older the subscriber, the higher the annuity rate. This is because the insurer’s expected payout period is shorter, allowing for larger periodic instalments.

For instance, a subscriber purchasing an annuity at age 60 might receive a rate of 6.5%, while someone deferring the purchase until age 70 might secure a rate of 8% for the same corpus. Planning the timing of your exit from NPS can therefore significantly optimise your long-term pension income.