Contact Us

![]()

For NRI Customers

(To Buy a Policy)

(If you're our existing customer)

For Online Policy Purchase

(New and Ongoing Applications)

Branch Locator

For Existing Customers

(Issued Policy)

Fund Performance Check

Login

![]()

![]() Customers

Customers

![]()

![]() Employees

Employees

![]()

![]() Partner

Partner

![]()

- Whole Life Insurance

- What Is Whole Life Insurance

- Types Of Policies

- Benefits Of Buying A Plan

- Why Sum Assured is an Important Factor When it Comes to Term Insurance?

- Features Of Buying A Plan Coverage

- How Does it Work?

- Difference Between Term & Whole Life Insurance

- Why One Should Buy A Whole Life Insurance Policy

- What Are Riders

- Is a Whole Life Insurance Plan Right for You?

- Who Should Purchase a Plan

- Eligibility Criteria For Buying

- How To Buy A Plan Online?

- Factors To Consider When Choosing a Plan

- Summary

- FAQs

- Related Articles

- Popular Searches

- Disclaimers

Whole Life Insurance

Whole life insurance is a policy that provides financial protection for the policyholder’s entire lifetime up to the age of 99 years. This ensures that the nominee receives the benefit whenever the claim arises, as per policy terms.

This policy is also known as permanent life insurance because lifelong protection is guaranteed as long as premiums are paid. A key advantage is the tax-free10 death benefit, which offers long-term financial security for your loved ones. ...Read More

1 Crore Term Insurance@ Rs.19/day***

-

Return of Premium (ROP) Option^

-

Individual Death Claim Settlement Ratio of 99.72%##

-

₹5 lakh instant payout on claim intimation36

-

Special Rates for Salaried & women19

-

0% GST on Premiums#^#

-

Premium Break Benefit35 for up to 12 months

Francis Rodrigues

Francis Rodrigues

Francis Rodrigues has a decade long experience in the insurance sector, and as SVP, E-Commerce and Digital Marketing, HDFC Life, manages the online sales channel, as well as digital and performance marketing. He has had hands-on experience in setting up sales channels and functional teams from scratch over a career spanning 2 decades.

What Is Whole Life Insurance?

A full life insurance is a lifelong protection plan that not only ensures financial security but also builds value over time. It guarantees that the policyholder’s family receives dependable financial support whenever the claim arises, offering coverage up to 99 years.

A major benefit of this plan is the guaranteed death benefit, which provides long-term security for beneficiaries. Additionally, a certain amount of the premium contributes to a cash value component that grows steadily and can be accessed for retirement, emergencies, or important financial goals in life.

Whole life cover insurance combines protection with accumulated cash value or maturity payout, ensuring dual benefits. Generally, premiums remain fixed throughout the policy, making long-term financial planning easier.

Short-term market fluctuations have a lesser impact on this type of insurance compared to market-linked investments, making it a stable investment option. Non-resident Indians (NRIs) can also purchase whole life plans to safeguard their families in India while enjoying similar benefits, subject to applicable regulations.

Types Of Whole Life Insurance Policies

There are different types of whole life insurance policies with unique features and premium structures. To select the right policy that matches your individual financial goals and needs, consider the following types of whole life policies:

1

1

Limited payment of whole life insurance

Limited payment whole life insurance requires premiums to be paid only for a fixed term, such as 15 or 20 years, while coverage continues for life. Since payments are compressed, premiums are higher than regular policies, but this option suits individuals seeking lifelong protection with early premium completion. It ensures premium-free years later, financial relief, and potential tax benefits during the payment period.

...Read More

2

2

Single premium whole life insurance policy

A single premium whole life policy requires a one-time lump sum payment to secure lifetime coverage. After this payment, no further premiums are needed, and the policy becomes “paid-up” immediately.

It is suitable for those with surplus funds seeking both insurance and savings benefits. The premium builds cash value over time, offers borrowing options, and supports inheritance planning, legacy planning, wealth transfer, asset protection planning, succession planning, or tax-efficient wealth transfer.

...Read More

3

3

Modified whole life insurance

Purchasing a modified whole life insurance plan will give you the benefit of lower premiums for the first few years, which later rise to a fixed higher amount. However, the death benefit remains unchanged throughout.

This plan is suitable for individuals expecting future income growth, offering affordable premiums early in their careers. In case the premium increases later, it can be challenging if you experience a financial shift. Therefore, insurers clearly outline premium schedules and amounts in policy documents at the time of purchase.

...Read More

4

4

Variable whole life insurance

With a variable whole life insurance policy, it is possible to invest premiums in stocks and bonds, selected by the policyholder. Cash value and death benefits fluctuate with investment performance, offering growth potential and tax benefits10.

This type of life insurance is suitable for those with a higher risk appetite and who have a flexible outlook for better returns. Policyholders can switch funds, though poor performance may reduce cash value. Moreover, the coverage remains active as long as premiums are paid.

...Read More

5

5

Joint whole life insurance

A joint whole life insurance covers two individuals under one policy, who are often either spouses or business partners. The death benefits are paid upon the first death, after which the policy ends.

Usually, it does not offer survival or maturity benefits but is more cost-effective than two separate policies. This option simplifies financial and estate planning. However, after the first claim, the policy terminates, so the surviving insured must get a separate coverage if needed.

...Read More

6

6

Participating in a whole life insurance policy

Getting a participating policy will provide dividends or bonuses, representing a share of the insurer’s profit. These dividends can be used to reduce premiums, taken as cash, or left to earn interest.

They add extra value beyond the guaranteed death benefit, potentially enhancing cash value and benefits over time. However, dividends are not guaranteed, making this option suitable for those seeking possible additional returns.

...Read More

7

7

Non-participating Whole Life Insurance Policy

With a non-participating whole life insurance policy, you will not be entitled to receive dividends or share in the insurer’s profits. Instead, they guarantee fixed death benefits and stable premiums throughout the policy term.

These types of insurance plans have lower premiums compared to participating plans. They appeal to individuals seeking predictable returns and straightforward coverage.

Therefore, the simplicity and certainty of these life insurance policies make them ideal for conservative policyholders who prioritise guaranteed protection over potential but uncertain bonuses.

...Read More

8

8

Pure whole life plan

Purchasing a pure whole life insurance will require regular premium payments throughout the insured’s lifetime. It provides a fixed death benefit to the nominee upon the policyholder’s untimely demise.

In case of no savings, dividends or maturity benefits, it offers straightforward protection. Premiums and benefits are fixed, making it desirable for individuals who want simple, essential life coverage without investment or bonus components.

...Read More

9

9

Level premium whole life insurance

A level premium whole life policy ensures premiums stay the same throughout the policy, providing stability for long-term budgeting and planning. It guarantees a fixed sum assured to beneficiaries in case of the insured’s demise.

With no increase due to age or health, it offers predictable costs. Though initial premiums may be slightly higher, it is a popular choice for consistent expenses and lifelong financial protection for you and your family.

...Read More

10

10

Indeterminate premium

An intermediate premium whole life insurance has varying premiums over time based on the insurer’s costs and claims experience. However, the premium stayed within a defined range despite changing. This ensured that the policy is continued systematically without any financial strain.

This structure balances fixed and flexible premiums, helping insurers manage risks. Therefore, policyholders should expect adjustments but remain assured of lifelong coverage within the changing, yet predictable, premium amounts.

...Read More

Why Sum Assured is an Important Factor When it Comes to Term Insurance?

Choosing the right sum assured in your term insurance plans is essential for your family's financial security. Moreover, one of the key tax benefits of term insurance is that the sum assured amount received by the nominee is tax-free under the Income Tax Act, 1961*. Hence, choosing a higher sum assured ensures your loved ones are well-supported, covering debts, education costs, and income replacement. A higher sum ensures your loved ones are well-supported, covering debts, education costs, and income replacement. Selecting the right amount is key to ensuring their future is secure. To explore the best term life insurance options and find the ideal sum assured for your needs, click the tabs below.

ARN - ED/02/25/21047

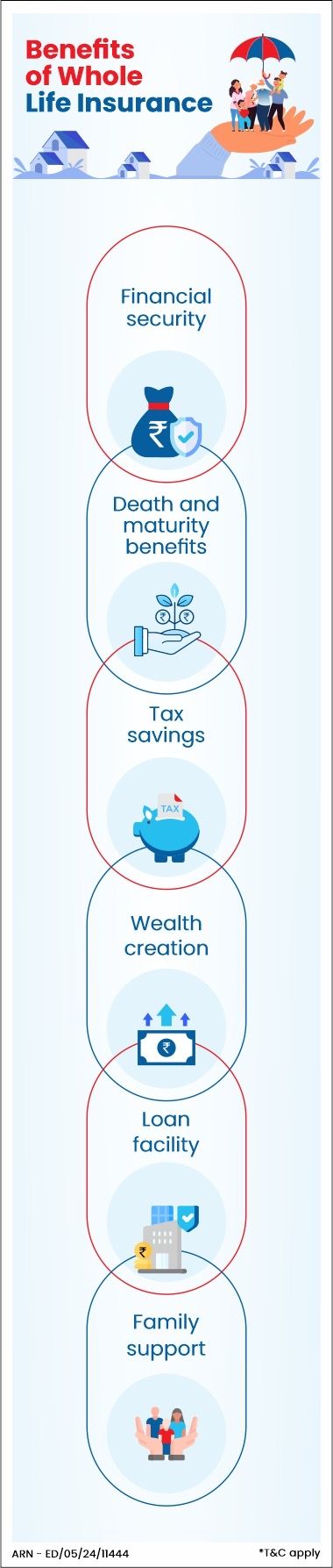

Benefits Of Buying A Whole Life Insurance Plan

With a whole life insurance plan, you will be able to get death benefits if you pay regular payments. Here are the different benefits of buying a whole life policy:

1

1

Financial security

Whole life insurance provides lifelong coverage, ensuring your family’s financial needs are met even after the insured’s death. It helps pay for daily expenses, outstanding debts, and essential costs, giving dependents stability and peace of mind.

Since the coverage never expires, it acts as a guaranteed financial protection. Moreover, it offers reliable and long-term safety for your loved ones.

...Read More

2

2

Death and maturity benefits

A whole life insurance plan offers dual benefits, including death benefits for nominees and maturity benefits for the policyholders. This combination of protection and savings ensures financial continuity for family members under any circumstances.

Additionally, maturity benefits promote disciplined and systematic long-term saving habits. This makes it easier to achieve financial security while balancing protection and wealth building in one single plan.

...Read More

3

3

Tax savings

Deductions under 80C and 10 (10D) of the Income Tax Act or ITA 1961 allow you to avail of tax benefits regarding whole life policy premium payments and payouts. Hence, it helps in long-term financial planning

...Read More

4

4

Wealth creation

A whole life insurance policy allows premiums to accumulate steadily, creating a financial corpus over time. This corpus amount can be used for retirement, legacy planning or achieving life goals such as a child’s education.

Policyholders can optimise coverage and benefits by using a life insurance calculator. Furthermore, guaranteed payouts ensure that planned future milestones are confidently achieved.

...Read More

5

5

Loan facility

Policyholders can borrow against their whole life insurance during financial emergencies, providing quick liquidity without liquidating other investments. This facility helps meet urgent needs while retaining the core policy benefits.

Loans against policies often have more favourable terms compared to unsecured credit. This makes it a practical and low-risk solution for addressing short-term financial requirements effectively.

...Read More

6

6

Family support

With a full life insurance policy, policyholders can ensure dependents can maintain their lifestyle even after the policyholder’s death. It can fund children’s education, support elderly parents, or cover household expenses.

It provides financial stability for your loved ones during difficult times by reducing emotional and financial stress. Moreover, the plan prevents financial disruption, helping families sustain their future with security and confidence.

...Read More

Features Of Buying A Whole Life Insurance Plan Coverage

Whole life insurance comes with several key features that provide both protection and value. Below are the main features of this plan:

Provides Financial coverage

A whole life policy ensures lifelong financial protection till the policyholder’s 99th year, unlike term plans that cover only a fixed duration. This guarantees a payout regardless of when the policyholder’s death occurs, offering peace of mind that dependents will always be protected. Furthermore, premiums will be payable for a limited term or throughout life, depending on the plan’s features.

...Read More

Cash Value

The cash value is the savings component of whole life insurance that grows steadily at a guaranteed rate. Policyholders can access it during their lifetime through withdrawals or loans.

It can be used for major expenses like buying real estate, higher education or family emergencies. The cash value is separate from the death benefit and grows tax-deferred.

...Read More

Dividend Features

Participating whole life policies may offer dividends, which are a share of the insurer’s surplus profits. These dividends can be taken as cash, used to pay premiums, or reinvested to increase coverage and cash value.

Though there is no guarantee, they provide additional value beyond the guaranteed death benefit. This makes the plan more rewarding for policyholders and their families if the insurer performs well.

...Read More

Riders/ Add-ons

Riders are optional add-on features purchased at an extra cost to expand the policy’s benefits. Examples of add-on features include critical illness cover, accidental death benefit, waiver of premium, or disability income benefit.

These riders*# allow customisation of the policy to align with your financial goals and address specific risks. They enhance protection and are more cost-effective than buying separate standalone insurance products.

...Read More

How Does Whole Life Insurance Work?

Whole life insurance works by combining lifetime protection with a built-in savings component, ensuring both financial security and cash value growth. This cash value accumulates over time with consistent premium payments. The accumulated cash value amount can be accessed through policy loans or withdrawals, offering a living benefit to the policyholder while the policy is in force.

Lifelong Coverage Duration

A whole life policy is designed to provide coverage for the insurer’s entire lifetime. This coverage is provided until the age of 99 years or more, as long as premiums are paid.

Moreover, it ensures that beneficiaries receive the death benefit whenever the policyholder passes away. The extended coverage offers financial predictability and stability, making it a reliable tool for long-term financial planning and guaranteeing lifelong security for dependents.

Premium Payments

Premium payments are fixed amounts that policyholders pay monthly, quarterly, or annually to keep the policy active. A portion of each payment covers insurance protection, while the rest contributes to building the policy’s cash value, which can be easily tracked and managed through digital life insurance platforms.

Premiums remain level throughout the term, unaffected by age or health changes. Therefore, consistent payment is essential to maintain coverage and ensure both protection and savings benefits.

Cash Value Accumulation

Cash value is the savings portion of whole life insurance, which grows steadily on a tax-deferred basis. The insurer invests a part of each premium. This guarantees interest and sometimes dividends depending on the policy’s features.

Policyholders can access this value through loans or withdrawals, though doing so may affect the death benefit. It serves as a living benefit in addition to insurance protection.

Death Benefit

The death benefit is the guaranteed lump sum paid to nominated beneficiaries when the policyholder passes away. It remains fixed unless increased with riders and is usually tax-free under applicable laws.

However, loans or withdrawals from the cash value may reduce the final payout. This benefit is the primary purpose of the policy, ensuring financial security for loved ones.

Maturity Payout

If the policyholder survives until the maturity age, often 99 years, they receive a maturity payout. This includes the sum assured along with accumulated bonuses (if applicable) and the cash value.

The payout can serve as a retirement corpus or a lump-sum fund for long-term needs. In some cases, insurers may treat maturity as the policy’s closure.

What Is The Difference Between Term Insurance & Whole Life Insurance?

Parameters |

Term Insurance |

Whole Life Plan |

Time period |

Term insurance plan covers for a specific duration. |

Whole life insurance plan provides coverage for the whole life and can extend up to 99 years of age. |

Premium amount |

The premium amount is usually low. |

The premium amount is comparatively higher as it provides life-long coverage. |

Cash value |

It usually does not offer any cash value. |

It offers cash value that grows with time. |

Wealth creation |

It does not assist in building wealth. |

It helps in wealth creation. |

Suitability |

It is ideal for individuals who only want insurance. |

It is suitable for individuals wishing for insurance along with investment/savings. |

Lapse of policy |

The policy expires after a certain time period. |

The policy doesn’t expire as long as you keep paying premium amounts. |

Legacy |

It may not be an ideal option for building/leaving a legacy for your children. |

It is an ideal option to build a legacy and create wealth for your children. |

Why One Should Buy A Whole Life Insurance Policy?

Going beyond a standard life cover, a whole life insurance policy offers lifelong protection with additional financial benefits, such as cash accumulation over time. It also helps the policyholder achieve long-term financial goals, helping manage debts and other financial obligations. If you are wondering why to get a whole life insurance policy, read the details below:

Builds Cash Value Over Time

Provides Lifelong Financial Protection

Supports Debt and Financial Obligations

Helps Achieve Long-Term Financial Goals

When you invest in a whole life insurance policy through premiums, a part gets allocated for savings purposes within the policy. This component grows over time on a tax-deferred basis and turns into a financial asset.

Depending on policy conditions, policyholders have the full flexibility to access this fund through policy loans or withdrawals. This way, the policy functions as a protector and a long-term financial reserve.

Including a whole life insurance policy in your financial plan can help protect your family from financial burdens in your absence. The death benefit payout can be used to settle outstanding obligations such as home loans, personal loans, or education expenses.

This ensures dependents do not face financial stress or the need to liquidate important assets to meet these commitments.

You can make a whole life insurance policy as a part of your responsible financial planning, too. The death benefit payouts can ensure that your family members will not face any financial burden in your absence.

If there are any outstanding financial obligations, such as paying off home loans, personal loans or education loans, they can use the payouts to settle them.

The accumulated cash component of a whole life insurance policy could be beneficial even when the policyholder is alive. Since policyholders have the freedom to access this fund without surrendering the policy entirely, they can use it for multiple purposes.

For example, they can use it as a supplement to their retirement income, support their children’s education or fund major life milestones. This flexibility allows the policy to support both financial protection and long-term financial planning.

Who Should Purchase A Whole Life Insurance Plan?

Read the following pointers to understand who should purchase a whole life insurance policy:

01

Individuals Who Want to Leave a Legacy

People can leave a financial legacy for their loved ones or charitable causes by purchasing whole life insurance. In addition to offering financial stability and achieving charitable objectives, the tax-free death benefit guarantees asset transfer throughout generations. It provides beneficiaries with money for business, education, or other necessities, ensuring a long-lasting effect.

02

Individuals Seeking Wealth Creation

For people who want to build money over the long term, whole life insurance is perfect. The insurance provides a secure, market-independent savings alternative as its cash value increases gradually over time. By borrowing against this cash value, policyholders may maintain liquidity and accumulate assets that will help them meet their immediate requirements and future financial objectives.

03

People with Financial Dependents

Whole life insurance should be taken into consideration by those who have dependents, such as elderly parents, spouses, or children. In the event of an untimely death, it guarantees that their loved ones would get financial support. The death benefit covers essential expenses like daily living costs, education, and debts, securing their dependents’ financial future.

04

Individuals Planning for Retirement

Whole life insurance builds up cash value over time, making it a useful tool for a comprehensive retirement plan. In order to generate an extra source of income in retirement, policyholders have the option to withdraw or borrow against their savings. In addition to pensions, investments, or other retirement savings programs, this guarantees stability and financial independence.

05

People Looking for Tax Savings

The tax benefits of whole life insurance are substantial. The cash value of the insurance increases tax-deferred, which means that no taxes are due on profits until they are taken out. Beneficiaries are likewise exempt from paying taxes on the death payment. It is a desirable choice for anyone looking for long-term financial stability and effective tax planning because of these tax advantages.

Moreover, the new GST on term insurance has lowered GST rates on premiums for term insurance plans, which can serve as a cost-effective complement to whole life insurance when building a comprehensive financial plan.

06

Individuals Wanting Guaranteed Lifelong Protection

Whole life cover insurance is ideal for those who value uninterrupted financial coverage, unlike term plans that expire after fixed periods. It ensures beneficiaries receive the death benefit whenever the policyholder passes away.

This makes it valuable for lifelong dependents, estate planning, or asset transfer. Hence, the assurance of lifelong protection provides peace of mind, knowing coverage will never lapse.

What Are The Whole Life Insurance Riders?

Riders can be termed as add-ons, which can enhance the coverage of the policy. These riders may add to the premium amount but always come in handy in uncertain times. A few of them are mentioned below.

Waiver of Premium Rider

In this rider, if the insured is diagnosed with a critical illness or met with an accident that left him disabled, the future premiums will be waived while the policy will still remain in force.

Accidental Death Benefit Rider

In this rider, the insurance company pays an additional payout to the nominees or beneficiaries in case the policyholder passes away due to an accident.

Accidental Total Permanent Disability Rider

In the accidental total permanent disability rider, if the policyholder is diagnosed with total permanent disability due to an accident, the insurance company will pay the rider the sum assured to him to cover the medical costs.

Critical Illness Rider

In this add-on, if the insured is diagnosed with a critical illness, the rider can take care of the financial expenses and obligations, including organ transplants, heart treatments, etc.

Terminal Illness Benefit

In this rider, the nominee or the beneficiary receives the sum assured on the insured’s demise after he’s diagnosed with a terminal illness.

Hospitalization Benefits

Under this rider, if you get hospitalized in general or even get admitted to the ICU, a fixed percentage of your policy's basic sum assured would be paid to help take care of your (the policyholder's) medical bills and treatment costs.

You must always select riders or add-ons based on your needs or requirements and must not hesitate to add them to your policy even if they add up to the cost.

Is a Whole Life Insurance Plan Right for You?

Buying a whole life insurance policy would be the right choice for you in the following cases/situations:

- If you want to leave a legacy for your children in the future

- If you want your term insurance coverage to continue even after retirement

- If you want a lifetime coverage against life-threatening diseases

- If you are planning to either get married or start a family soon

- If you want the twin benefits of investment and life insurance coverage

- If you want additional liquidity at the time of retirement

Eligibility Chart for Whole Life Insurance

However, insurers may have differences in specific terms, conditions, and the flexibility they offer. Common criteria include:

Parameters |

Minimum |

Maximum |

Entry Age |

18 years |

65 years |

Maturity Age |

23 years |

99/100 years |

Policy Term |

5 years |

(100 - entry age) years |

Sum Assured |

Rs 25 Lakh |

Rs 20 Crore |

Whole Life Insurance Premium Payment |

Monthly, Yearly, Quarterly, or Semi-Annually |

|

How To Buy A Whole Life Insurance Plan Online?

Follow the directions given below to buy a whole life insurance plan online:

Give Key Details

When buying a whole life insurance plan online, you must provide the following personal information:

Name

Date of Birth

Income

Occupation

Medical History

Furthermore, lifestyle habits like smoking or alcohol consumption are also considered before finalising the policy’s premium. Accurate disclosure ensures fair risk evaluation, correct premium calculation, and smooth claim settlement. Any discrepancies or incomplete details may lead to claim rejection or policy denial.

Determine the Coverage Amount

Select a sum assured that replaces income, clears outstanding education. A common approach is 10 to 15 times your annual income, after considering inflation and lifestyle goals.

Understanding coverage may leave dependents financially insecure, while overestimating leads to unnecessarily high premiums. Hence, with the right balance, you can ensure adequate protection without overburdening you financially.

Personalise Your Policy

Customising a whole life plan means selecting payment modes, tenure, and riders like accidental death or critical illness. Riders add targeted protection at minimal cost. You can also choose payout structures, which can be either a lump sum, a monthly income, or a combination to match your family’s needs.

Younger buyers benefit from locking in lower premiums early. This is because such buyers are generally healthy, which lowers the premium amount.

Make the Premium Payment

The policy begins after premium payment and underwriting approval. Payment options include net banking, UPI, debit/credit cards, ECS, or auto-debit mandate.

Timely payments prevent policy lapse and loss of coverage. Most insurers offer a free-look period to review and act as proof of transaction, ensuring a clear record for future policy servicing or claims.

How To Buy A Whole Life Insurance Plan From HDFC Life?

Purchasing a whole life insurance plan from HDFC Life involves a straightforward process:

1. Research Available Plans: Visit HDFC Life's official website to explore their whole life insurance offerings, such as the HDFC Life Sampoorn Samridhi Plus plan, which provides life cover up to 100 years of age and additional benefits.

2. Assess Your Needs: Determine the coverage amount and premium payment term that align with your financial goals and obligations.

3. Use Online Tools: Use the term insurance premium calculator available on HDFC Life's website to estimate your premiums and understand the benefits of the policy.

4. Consult with Advisors: For personalised guidance, contact HDFC Life's insurance advisors who can assist in selecting the most suitable plan based on your requirements.

5. Application Process: Complete the application form online or offline, providing necessary personal and medical information.

6. Medical Examination: Undergo any required medical tests as part of the underwriting process.

7. Policy Issuance: Upon approval, review the policy document thoroughly to understand the terms and conditions before making the initial premium payment.

By following these steps, you can secure a whole life insurance policy from HDFC Life that aligns with your financial planning objectives.

What Are The Factors To Consider When Choosing A Whole Life Insurance Plan?

When selecting a whole life insurance plan, it is crucial to consider various factors that influence its long-term value and suitability. The following considerations must be taken into account when choosing a whole life plan:

1

1

Coverage amount

The right coverage amount is crucial to maintain your family’s financial security. Not only should it cover present expenses, but also future ones like children’s higher education, debt repayment, mortgage and retirement needs. Many individuals find that a 1 crore term insurance cover provides a strong safety net for such long-term responsibilities. Consulting a financial expert and using an online calculator will help you determine the adequate coverage amount.

Being underinsured can leave your family financially vulnerable. Consequently, overinsuring can lead to unnecessarily high premiums, which can be a financial burden if earnings decrease. Therefore, maintaining a balance between affordability and adequate protection is crucial for financial stability.

...Read More

2

2

Inflation

With the onset of inflation in an economy, the value of money reduces over time. This makes today’s coverage insufficient for the future. For example, ₹2 crore today may not cover the same expenses after 20 to 25 years because of rising costs.

Therefore, taking a policy with riders that increase the sum assured or provide inflation-adjusted benefits will help you safeguard its effects. Considering inflation during selection ensures your plan remains effective and relevant for decades, protecting your family against financial shortfalls caused by eroded purchasing power.

...Read More

3

3

Early Investments

Buying a full life insurance policy at a younger age ensures significantly lower premiums. For instance, a 25-year-old may pay much less than a 40-year-old for the same coverage due to lower health risks. Early investment also allows more time for cash value accumulation, helping policy benefits grow steadily over the years.

Securing coverage early protects against higher premiums or rejection due to age-related health conditions later in life. Therefore, starting young maximises both cost savings and long-term advantages.

...Read More

4

4

Select Add-ons

Add-on features enhance a whole life insurance plan by offering extra protection against specific risks. Here are the common riders which can be included in these policy plans:

Accidental Death Benefit (extra payout on accidental death)

Critical Illness Cover (lump sum or diagnosis)

Waiver of Premium (waives future premiums in case of disability)

However, before selecting add-on features, assess personal factors like lifestyle, family medical history, and occupation. Avoid any unnecessary add-ons as they can excessively increase the premium amount. Ensure to select relevant riders since this customised approach ensures better financial protection.

...Read More

5

5

Go through the policy document

Reading the entire policy document carefully is essential before purchasing. Some of the main areas to check include inclusions, exclusions, waiting periods, grace periods, claim settlement process, and surrender terms.

It is equally important to understand the loan provisions against the policy and available tax benefits. Furthermore, clarifying any doubts directly with the insurer will help avoid unpleasant surprises regarding the premium amount. You will be able to make informed decisions for better long-term financial protection.

...Read More

6

6

Pick the right insurance provider

India's insurance regulatory body, the IRDAI or Insurance Regulatory and Development Authority of India, publish an annual report every financial year that mentions the CSR (claim settlement ratio) of each insurer. Claim Settlement Ratio is the percentage of claims that an insurance company settles in comparison to the total number of claims it received over a specific period of time, like one year.

When picking an insurer for your whole life insurance policy, compare the Claim Settlement Ratio

of various insurers and ideally go for the one having a higher Claim Settlement Ratio, such as HDFC Life, as it ensures the likelihood of your family’s claim being settled in your absence.

...Read More

Summary

Whole life insurance offers lifelong financial protection, up to the age of 99 or 100. With this policy, it is possible to build a savings or investment component that grows cash value over time. Unlike term insurance, which covers only a fixed period, whole life insurance ensures peace of mind by securing your family’s financial future.

While 2 crore term insurance provides significant coverage for a limited time, whole life insurance offers lifelong protection and growing cash value, making it a strong choice for long-term financial security. Selecting a reputable insurer with comprehensive coverage, flexible features, and competitive premiums is essential for maximising benefits. Beyond protection, it supports long-term financial planning, retirement, and legacy goals. Furthermore, it provides potential tax benefits under the Income Tax Act, 196110.

To maintain relevance, policyholders should periodically review and update their coverage as life circumstances change. This ensures the plan continues to serve its purpose of providing financial security.

FAQs On Whole Life Insurance

1

Is whole life insurance better than term life insurance?

Although both whole life and term insurance protect the financial stability of the policyholder's family upon their death, it is hard to say which one is better. Depending on affordability and personal goals, the policyholders can choose.

Whole life insurance has a higher premium, provides lifelong coverage up to 100 years, along with a cash value component that builds over time. In contrast, a term life insurance policy offers coverage for a specific time frame at a lower premium.

2

What is a whole life insurance policy?

A whole life insurance policy provides lifelong financial coverage to a policyholder’s beneficiaries by assuring a death benefit and accumulating cash value over time. The features include guaranteed growth (if available in the policy) and fixed premiums, making it suitable for long-term financial planning, such as estate planning. Policyholders can access the cash value through withdrawals or loans during their lifetime.

3

Is it good to invest in a whole life insurance plan?

Whole or permanent life insurance is worth investing in when you have dependents who rely on you financially. It ensures that your loved ones are taken care of when you are no more.

4

Should I buy a whole life insurance plan for my child?

It is a great option for your child as it protects them for your entire life span. The savings component grows over time and safeguards your child’s future in case of any unfortunate event. If you believe your child may need financial support in the future, you can designate them as your nominee. This makes it one of the best policy for child, ensuring long-term financial security and peace of mind for you and your family.

5

Is buying a whole life insurance plan expensive?

If you compare the premiums or costs involved with other policies like term insurance, then it is certainly costlier. But when you compare the benefits and features, you will find that it helps you leave a legacy for your dependents, which might make the investment worth it.

6

How much coverage should I consider while buying a whole life insurance plan?

You must assess your family’s future living costs, inflation, debts, cost of living, financial goals, etc., to calculate the exact coverage amount. Or you can multiply your annual income by 10 for a rough estimate. Certain online calculators can also make your job easy.

7

Can you borrow against the cash value of whole life insurance?

Yes, you can borrow against the cash value of whole life insurance once it has sufficiently accumulated, subject to the terms and conditions of the policy. This loan can provide easy access to funds for emergencies, education or other needs without liquidating assets. However, using this cash value as collateral for a loan will reduce the death benefit that the beneficiaries receive.

8

Is whole life insurance a good investment for retirement?

Whole life insurance can be a good investment for retirement if you have dependents relying on you financially. It combines lifelong protection with a cash value that grows over time, making it a lucrative investment. Furthermore, it helps build wealth steadily while ensuring financial security for your loved ones.

9

Can you develop a financial legacy with a whole life policy?

Yes, it is one of the reasons why individuals opt for a whole-life policy. Along with providing coverage for your whole life, which can extend to 99 years of age, it helps in wealth creation and leaving a legacy for your loved ones.

10

What is the right age to buy a whole life insurance plan?

The general rule of thumb is the earlier, the better. Hence, today is the right age to buy any permanent life insurance policy.

11

What is the death benefit under the whole life insurance policy?

The death benefit of a permanent life insurance policy is a predetermined amount or sum assured that is paid to the beneficiaries of the policyholder upon his demise.

Related Articles to Whole Life Insurance

Popular Searches

- term insurance

- Term Insurance Calculator

- Investment Plans

- savings plan

- ulip plan

- retirement plans

- health insurance plans

- child insurance plans

- group insurance plans

- saral jeevan bima yojana

- income tax calculator

- bmi calculator

- compound interest calculator

- income tax slab

- Income Tax Return

- benefits of term insurance calculator

- what is term insurance

- why to invest in life insurance

- Ulip vs SIP

- tax planning for salaried employees

- how to choose best child insurance plan

- Retirement Planning

- 1 crore term insurance

- HRA Calculator

- Annuity From NPS

- 2 crore term insurance

- 5 crore term insurance

- 1.5 crore term insurance

- Retirement Calculator

- Pension Calculator

- What is Investment

- Best Investment Plans

- Term Insurance for Housewife

- Money Back Policy

- life Insurance policy

- life Insurance

- Zero Cost Term Insurance

- critical illness insurance

- features of term insurance

- Best Term Insurance Plan for 1 Crore

- personal accident insurance

#Provided we have received all the relevant and required documents and no further investigation is required. Claim settlement process would be completed within stipulated timelines once the claim request is approved

##Individual claim settlement ratio by number of policies as per audited annual statistics for FY 25-26

^ Available under Life & Life Plus plan options

@As per integrated annual report FY24-25, available on www.hdfclife.com. As of May 2025

***Online Premium for Life Option for HDFC Life Click 2 Protect Supreme Plus(UIN:101N189V03), Male Life Assured, Non-Smoker, salaried, 20 years of age, Policy term of 25 years, Regular pay, Monthly frequency, inclusive of 15% online discount (applicable only for 1st year premium) & exclusive of taxes and levies as applicable. (Monthly Premium of 573/30=19).

**If a customer is a Salaried individual and has opted for a cover of INR 2 Cr with Limited pay, then the total discounts applicable shall be: 10% +7% = 17% discount on the first year premiums.

^^9% online discount available on 1st year premium only

~Tax benefits of ₹ 54,600 (₹ 46,800 u/s 80C & ₹ 7,800 u/s 80D) is calculated at highest tax slab rate of 30% on life insurance premium u/s 80C of ₹ 1,50,000 and health premium (Critical illness rider) u/s 80D of ₹ 25,000. Tax benefits are subject to conditions under section 80C, 80D, 10(10D) as per Income Tax Act, 1961. Please consult your tax advisor for more information.

*Online Premium for Life Option, Male Life Assured, Non-Smoker, 20 years of age, Policy term of 40 years, Regular pay, Monthly frequency, exclusive of taxes and levies as applicable.

HDFC Life Sampoorn Samridhi Plus (UIN:101N102V06) is a Non-Linked, Participating, Life Insurance Plan. Life Insurance Coverage is available in this product.

*#Riders / Add-Ons can be availed upon payment of additional premium.

10. Tax benefits & exemptions are subject to the conditions of the Income Tax Act, 1961 and its provisions. Tax Laws are subject to change from time to time. Customer is requested to seek tax advice from his Chartered Accountant or personal tax advisor with respect to his personal tax liabilities under the Income-tax law

19. HDFC Life Click 2 Protect Supreme Plus(UIN:101N189V03) is a Non-Linked, Non-Participating, Individual, Pure Risk Premium/ Savings Life Insurance Plan. Life Insurance Coverage is available in this product: 10% discount on first year premium would be applicable for only Salaried customers, under Regular Pay & Limited Pay. A 15% discount on the base premium rates will be applicable for female lives.

#^# Individual Life Insurance Policies issued on or subsequent to 22nd, September 2025, shall be exempt from GST under the provisions of the Goods and Services Tax, 2017.

35. Applicable if the policy has completed at least five (5) policy years from the risk commencement date and all the due premiums have been received in full and the policy is in force. If the premium break benefit has been exercised in the last 5 policy years, then the next premium break benefit shall not be allowed. The premium break benefit shall not be available during the last policy year of the premium payment term.

36. Applicable for all in force policies after a waiting period of 1 year. Please refer to policy documents for Terms & Conditions

ARN- ED/03/26/32884