Contact Us

![]()

For NRI Customers

(To Buy a Policy)

(If you're our existing customer)

For Online Policy Purchase

(New and Ongoing Applications)

Branch Locator

For Existing Customers

(Issued Policy)

Fund Performance Check

Login

![]()

![]() Customers

Customers

![]()

![]() Employees

Employees

![]()

![]() Partner

Partner

![]()

- Child Plans

- What Are Child Education Plans?

- HDFC Life Child Insurance Plans 2026

- How Child Plans Work?

- Why Invest in Child Plans?

- Why Get Child Education Plan?

- Importance of Life Cover in Child Plans

- Child Insurance Plan Features

- Key Benefits of Child Insurance Plans

- Tax Benefits of Child Education Plans

- Types of Child Plans

- Child Education Investment Options 2026

- How to choose child education plan?

- Tips for Buying Child Education Plan

- Why Plan Early for Child Education?

- How Much to Invest in a Child Plan?

- HDFC Life Child Insurance Plans in India

- Child Insurance Plan Claim Process

- Child Education Plan FAQs

- Share your Valuable Feedback

- Disclaimer

Flexible payout options

Valuable financial protection for your child

Flexible Benefit Payment Preferences

Premium Waiver

What Are Child Education Plans?

Child education plan is designed to enable parents to secure their child’s financial future by investing in a disciplined manner. You need to pay premiums regularly or as a single payment and at the end of the policy term you will receive the maturity benefit.

Child education plans are basically child insurance plans and thus are a combination of insurance and investment.

The life insurance component provides financial coverage to protect the child's future in case of the parent's demise. In case of the parent’s demise, the insurer pays the death benefit ensuring that the child’s education isn’t compromised even in the parent’s absence.

The investment component provides the opportunity to invest in market-linked instruments (ULIPs) or guaranteed return instruments (savings plans) to grow the investment as per the child’s educational requirement. The corpus should be adequate enough to cover the child’s future expenses.

...Read More

How Do Child Plans Work?

Let us take an example to understand how a child plan works:

Mr Mukherjee, a parent of a 5-year-old, plans to start investing in his son's higher education abroad. He is paying a monthly premium of Rs. 8,000 for 15 years.

Note: ROI is 6-8%

Let’s consider two different scenarios to understand how the payout would work.

Situation 1: Mr Mukherjee out-lives the policy term

In such a scenario, Mr Mukherjee will receive a sum assured of Rs. 20-25 lakhs (approx.) at the end of the policy tenure and now it can be used for higher education of his son.

...Read More

Situation 2: Mr Mukherjee dies on the 8th year of the policy term

In this situation, Mr Mukherjee's child and other nominees will receive a lump sum amount as life cover and the remaining premiums will be waived off. The nominees can also make partial withdrawals from the child insurance plan for the child's educational purpose based on the type of policy chosen.

...Read More

Why Invest in Child Plans?

Investing in a child insurance plan helps you systematically build funds for your child’s future needs, such as education, marriage, or other life goals. These plans offer the dual advantage of life insurance protection and disciplined savings ensuring your child’s dreams are not compromised even in your absence. While a child plan provides comprehensive coverage, it’s also worth considering the best term insurance plans to secure your family's future with affordable protection. While a child plan provides comprehensive coverage, it’s also worth considering the best term insurance plans to secure your family's future with affordable protection. Regular contributions help create a well-planned financial roadmap for your child’s key milestones.

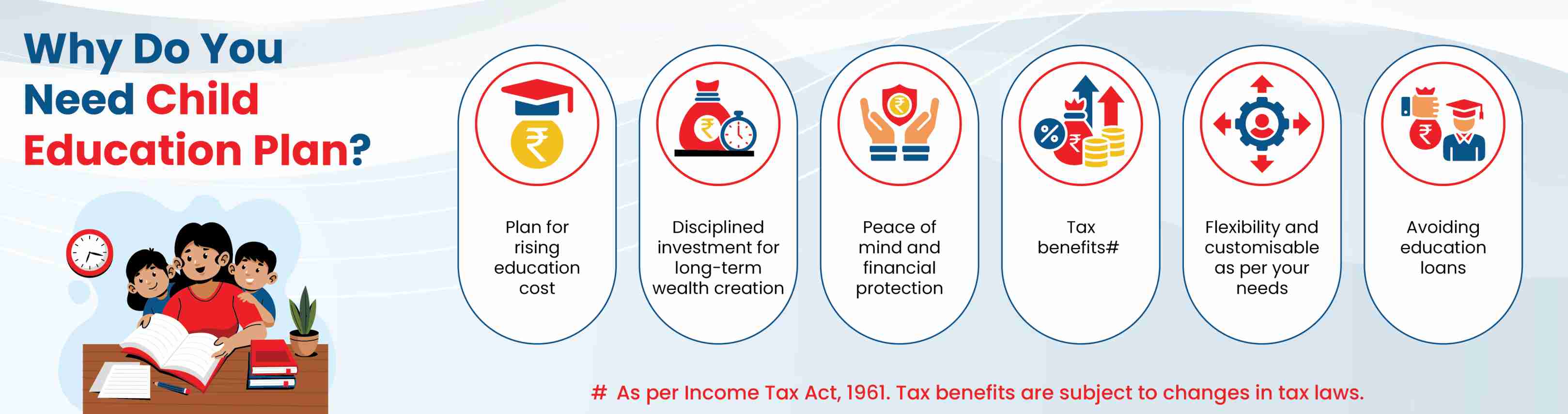

Why Do You Need Child Education Plan?

Child education plan is essential because of the rising cost of education. A child education plan is a dedicated long term investment plan to ensure that your child’s academic pursuits. Here are the reasons to invest in a child education plan:

Plan for rising education cost

rising cost of education in India is becoming a major concern as education expenses increase every year. As per a report by LocalCircles, 44% of the parents surveyed say their children's schools have increased fees by 50-80% (a) or more between 2022 and 2025. When it comes to higher education, the expense of pursuing an average engineering degree, can cost up to Rs. 2 lakhs to Rs. 15 lakhs(b), or more, depending on the institution. Studying overseas is even more expensive as Indian students spend approximately Rs. 10 lakhs to Rs. 60 lakhs (c) annually to study in the US.

Child education policy helps you to build a corpus dedicated for your child’s future education. The best child education plan will help you combat the rising cost of education so that your child’s dreams don’t face any financial constraints.

Disciplined investment for long-term wealth creation

Child plan encourages you to invest in a disciplined manner through regular premium payments. The approach of consistently investing helps in the accumulation of a sizeable amount over the long term. By starting early, you can take advantage of the power of compounding to grow your investments substantially and provide the required funds for your child’s education.

For example, investing Rs.10,000 per month from when your child is 6 until they turn 18 can grow to Rs.40.36 lakh at a 15% expected return.

But if you start later—investing ₹20,000 per month from age 12 to 18—the fund value will be just Rs. 23.42 lakh.

By starting 6 years earlier, even with half the monthly investment, you can accumulate nearly 72% more by investing regularly.

Peace of mind and financial protection

Child education plans are also known as child insurance plans as they have a built-in insurance component. The life insurance component provides a death benefit in case of your untimely demise. The death benefit ensures that your child’s dreams are not compromised even in your absence.

The safety net of the death benefit will give you the peace of mind that even in your absence your child’s future education will be secured.

Tax benefits

Since child plans are essentially child insurance plans these can help you save tax under the various sections of the Income Tax Act, of 1961.

- Section 80C :

All the premiums you pay for a child education plan are eligible for tax deductions under section 80C up to a limit of Rs. 1.5 lakh.

- Section 10(10D):

The maturity amount of a child plan is also exempted from deductions under section 10(10D).

Flexibility and customizable as per your needs

- Premium paying terms :

Child education policy offers you the flexibility to choose your premium payment terms (monthly, quarterly, half yearly, annually, or as a one time investment).

- Payout :

You can choose whether you want the maturity benefit to be paid as a lump sum or in a staggered manner helping your child pay for his education as per his needs.

- Fund options :

In case your child plan is a ULIP then you will have the flexibility to choose the funds you want to invest in depending on your risk appetite and investment horizon.

Avoiding education loans

By starting early and investing regularly in a child education plan for your children’s future you won’t need to take a loan for their education. This will reduce the financial burden on your children once they are done with their education.

Given the rising cost of education and life’s uncertainties, it’s crucial that you start investing early as well. You can look for different newborn investment plans to start securing the financial future of your children from the time they are born.

Why is life cover Important in Child Plans?

Life coverage in a child education plan provides the much needed safety for the child’s financial future. The death benefit payout ensures that the child’s academic goals remain undisturbed if the parent is no more.

Here is why life cover is vital in a child plan:

Secure Your Child's Financial Future

Families often fall into financial turmoil when they lose the primary earning member. The reallocation of financial resources usually leads to cuts in a child’s education-related expenses. However, with a child plan in place, you can ensure that you’re little one’s future education plans remain intact even if you are no longer around.

...Read More

Peace of Mind

A child plan gives you the comfort that life’s uncertainties cannot take a toll on your child’s academic plans. It relieves parents of anxiety about what happens to their child’s future when they are not around. The confidence of having a financial backup helps one focus on nurturing their child’s potential and growth without stress.

...Read More

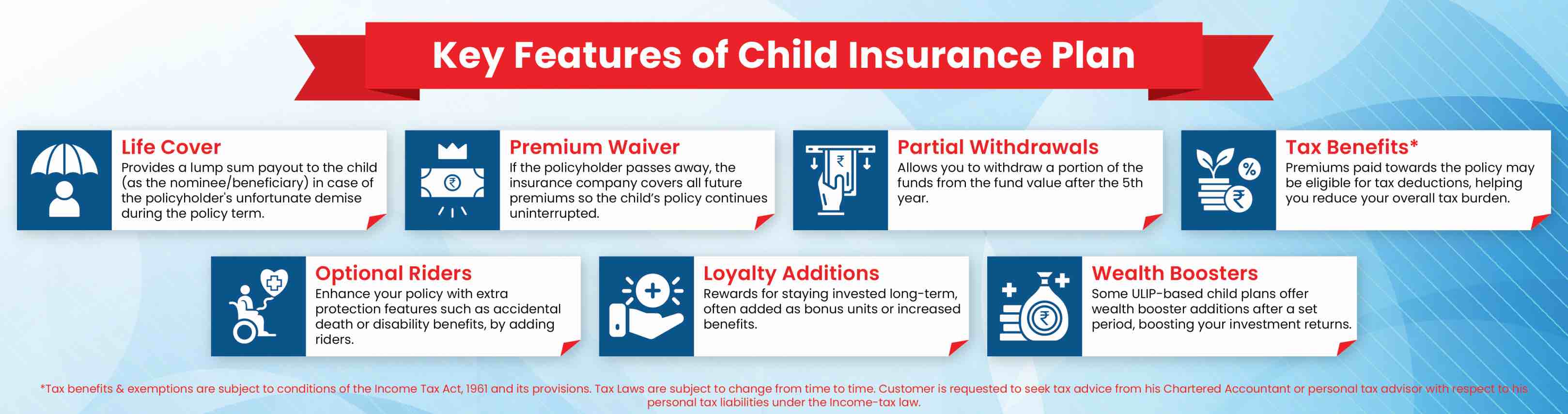

Features of Child Insurance Plans

Here are some of the features of child plans:

Life Cover

If something happens to you, the policy will give a lump sum of money to the people you choose. This ensures that your children's education fund remains secure and they can continue their studies without financial worries.

Premium Waiver

If the policyholder dies unexpectedly during the policy term, the insurance company will cover all the remaining premiums under the premium waiver benefits in child plan. This ensures that the policy stays active, and the child's future, particularly their education, remains secure without any interruptions in premium payments.

Partial withdrawals

The child insurance plans allows partial withdrawals starting from the 6th year (after 5 years). This flexibility helps cover important educational expenses like admission fees, tuition costs, and educational trips.

Sum assured

After partial withdrawals, you will get the remaining balance of the sum assured when the policy matures, in addition to life cover

Tax benefits

You can also be eligible for tax benefits under section 10(D)# and deductions under 80C# of the Income Tax Act. The amount of premium paid toward the policy will be eligible for a tax deduction, hence reducing your overall tax liability.

Flexibility

One of a child education plan's most crucial components is its adaptability. Monthly, quarterly, half-yearly, annual, or one-time lump sum premium payments are among the flexible options available under these policies. In accordance with the child's academic schedule, parents may also select policy lengths and payout schedules. This adaptability ensures greater control over savings and returns by assisting in coordinating financial planning with significant academic achievements.

Riders

A child policy often comes with optional riders that enhance its protection features. These may include premium waiver riders, critical illness riders, and accidental death benefit riders. By paying a small additional amount, parents can significantly increase the financial security offered by the child policy. These riders provide added protection in case of critical illness or unforeseen life events, ensuring that the child’s education continues to be funded even during difficult times.

Loyalty Additions

Many insurers provide loyalty benefits as a way to reward policyholders who remain engaged over longer periods of time. These are bonus sums that are either added to the insurance on a yearly basis or at predetermined intervals. The maturity value is increased by loyalty additions, which raises total returns. Parents may maximise their child's education investment plan and build up a more significant education corpus by remaining invested over the long run.

Wealth Booster

After a certain number of years, many ULIP-specific Child Plans offer unique rewards known as wealth booster enhancements. By adding extra units to the investment fund, these boosters raise the policy's worth without raising the expense. Long-term dedication and regular premium payments are rewarded. This feature dramatically increases the policy's fund worth, assisting parents in covering the rising cost of providing their kids with a high-quality education.

What are the Key Benefits of Investing in a Child Insurance Plan?

Here are the key benefits of investing in a child policy:

Disciplined long term investment

- Systematic investment :

Child insurance plans ensure that you invest in a systematic manner for the policy term to achieve your goal. This approach instils a sense of discipline to save for your children’s education.

- Power of compounding :

By investing in child plans over the long term you can take advantage of the power of compounding to grow your wealth substantially for your children’s education.

Financial Protection

- Life insurance :

The life insurance component of a child insurance plan provides the much needed financial safety net in case of your absence. The death benefit payout enables your children to pursue their goals without any financial constraints.

- Waiver of Premium :

In case the policyholder passes away the insurer waives off the remaining premiums keeping the policy active. The child receives the corpus at the time of maturity of the child policy.

Combating education inflation

Year-on-year education inflation rate for the month of May 2025 is 4.12% (d) in India. On the other hand, as per Funds India, Indian equities have given 15% returns over 20 years (e). In case you choose to invest in a ULIP child plan with a higher exposure in equity then over the long term you will be able to beat the rising education inflation.

Tax benefits

The best child education plans to help you save tax under the various sections of Income Tax Act, 1961.

- All the premiums you pay for a child education plan are eligible for tax deductions under section 80C up to a limit of Rs. 1.5 lakh.

- The maturity amount of a child plan is also exempted from deductions under section 10(10D).

Flexibility

Child education plans offer flexibility in the following manner:

- Types of investments :

Depending on your financial goals, risk appetite, and investment horizon you can choose the type of investment plan between endowment plans (guaranteed returns) or ULIPs (market linked returns).

- Premium payment :

Depending on your comfort you can choose the premium payment frequency and depending on your investment horizon you can choose the premium payment term.

- Partial withdrawal :

In the case of ULIPs after the lock-in period of 5 years you can make partial withdrawals based on your child’s needs.

- Add-on riders :

Along with the base child insurance plan you can choose to add riders (waiver of premium rider, critical illness rider, accidental death benefit rider etc.) as per your needs to enhance the coverage.

Tax Advantages of a Child Education Plan

Under Section 80C of the Income Tax Act, 1961, the premiums paid for a Child Investment Plan qualify for a tax deduction of up to ₹1.5 lakh per financial year, subject to conditions.

Additionally, under Section 10(10D), the maturity benefits of the plan are tax-free if the annual premium does not exceed:

- ₹2.5 lakh for ULIPs (Unit Linked Insurance Plans)

- ₹5 lakh for non-ULIP child investment plans

These tax benefits apply throughout the policy tenure and remain tax-exempt upon policy completion or in case of the parent's demise, subject to conditions.

Sections of the Income Tax Act, 1961# |

Tax Benefits under the Child Education Plan |

Section 80C |

- Premiums paid under this plan are eligible for tax deduction upto Rs. 1,50,000 subject to conditions specified. |

Section 10 (10D) |

- Enjoy tax-free maturity with your child plan, with an annual premium of up to Rs. 2,50,000 for ULIPs or Rs 5,00,000 for other than ULIPs subject to conditions mentioned. - Tax-free benefits are received on death . |

Discover more about the deduction under 80C for the best child education plan.

Types of Child Plans

Different types of child insurance plans are customized for providing different advantages such as education support, financial protection in case of uncertainties, and long-term savings.

Below is a comparison table showing the child plans of 2026:

Plan Type |

Key Benefit |

Ideal For |

Dual benefit of investment and insurance with market-linked returns and Life cover. |

Parents looking for wealth creation and life cover over the long term |

|

Regular savings with insurance coverage and maturity benefits |

Parents aiming for systematic and regular savings |

|

Guaranteed Capital Solutions |

Assured maturity benefits regardless of market performance with Life covers. |

Risk-averse parents seeking capital protection |

Fixed returns with predictable payouts for future milestones along with life cover. |

Parents who want guaranteed funds for education expenses |

Different plans are meant to address diverse financial objectives and risk appetites. Choosing the right one is based on your child's future requirements and investment horizon.

Best Investment Options for Child’s Education in India 2026

Securing your child's future requires careful financial planning paired with smart investments. To understand the best child education plan that you can invest in 2026 to secure your child’s future, read below:

Sukanya Samriddhi Yojana (SSY)

a. Lock-in Period– Until the girl child reaches 21 years or upon marriage after reaching 18 years

b. Investment Type– Government-backed small savings scheme

c. Returns– 8.2% per annum, compounded yearly

d. Tax Benefits– Up to Rs. 1.5 Lakhs under Section 80C# of the Income Tax Act,1961

Unit Linked Insurance Plan (ULIP)

a. Lock-in Period– 5 years

b. Investment Type– ULIPs are essentially life insurance plans that offer market-linked returns along with life cover

c. Returns– Depends on market Conditions

d. Tax Benefits– Up to Rs. 1.5 Lakhs under Section 80C# of the Income Tax Act,1961 and maturity proceeds are tax exempt under Section 10(10D)##subjected to prescribed conditions

Endowment Plan

a. Lock-in Period– 2 years

b. Investment Type – Endowment policy is a combination insurance and guaranteed savings scheme

c. Returns– Usually depends on the terms and conditions of the policy.

d. Tax Benefits– Up to Rs. 1.5 Lakhs under Section 80C# of the Income Tax Act,1961 and maturity proceeds are tax exempt under Section 10(10D)## subjected to prescribed conditions

Savings Plan

a. Lock-in Period– Usually 5 to 10 years, depending on the tenure of the savings plan

b. Investment Type– Traditional life insurance plan

c. Returns– 4% - 6%

Tax Benefits– Up to Rs. 1.5 Lakhs under Section 80C# of Income Tax Act, 1961 and maturity proceeds are tax exempt under Section 10(10D)## subjected to prescribed conditions

Mutual Fund

a. Lock-in Period– No lock-in period

b. Investment Type– Market-linked investment scheme

c. Returns– Usually vary according to fund type

d. Tax Benefits– Up to Rs. 1.5 Lakh deduction under Section 80C# of the Income Tax Act,1961

Note - It is essential to note that the total deduction available under section 80C# of the Income Tax Act, 1961, considering all the above investments allowed under this section should not exceed Rs.1, 50,000 per year. Individuals and HUFs are both eligible for Section 80C# deductions if they have opted for Old Tax Regime.

How to choose the best child education plan?

Choosing the most suitable child education plan as per your children’s education needs is essential. Here is a breakdown of the steps to choose the best child plan for your children –

1.Assess your child’s education goals

- Estimate future expenses :

Find out the present cost of the education your child desires and then adjust it for education inflation in India.

- Investment horizon :

Your investment horizon will be determined by the difference between your children’s current age and the age at which they will require the funds.

- Payout structure :

You can choose to receive the maturity amount either as a lump sum or regular payments depending on the education expenses such as tuition, accommodation, travel, books etc. If you prefer a lump sum payout, a lumpsum calculator can help you estimate the amount you would receive, allowing you to plan better for these expenses.

2.Understand your risk appetite

Depending on your risk appetite and investment horizon you can choose from the following –

- ULIP (Unit Linked Insurance Plan) :

If you have a higher risk appetite and a longer investment horizon (suppose your child is 8 years old and you need the funds when he/she turns 18) you can choose ULIP. A part of your investment is invested in equity and debt assets giving you the opportunity to generate higher returns of the long term.

- Endowment plan :

Endowment plans are a safer option, suitable for people who are risk averse. The returns might be less but guaranteed as the investments are primarily in debt instruments.

- Money back plan :

With a money back policy you receive payouts during the policy term. These are less risky than ULIPs and the payouts will help you manage irregular expenses of your children’s education.

- Government schemes :

As a parent of a girl child, you can consider Sukanya Samriddhi Yojana as a child policy option to secure her financial future. This government-backed savings scheme is specifically designed to support a girl child’s long-term needs. The funds accumulated under this child policy will be available when your daughter turns 18 years old, helping you plan for her higher education or other milestones.

3.Key features to consider

- Maturity benefit :

The maturity amount of your child policy should be sufficient to cover the estimated cost of education. You can choose to receive the payout as a lump sum or in instalments, depending on your child’s education expenses.

- Death benefit :

Child insurance plans provide death benefit to the nominee in case of the policyholder’s demise during the policy term. The death benefit ensures that your child’s financial future is taken care of even in your absence.

- Premium waiver benefit :

In case of your sudden demise or disability due to accident all your future premiums will be waived of while the policy continues.

- Partial withdrawal :

After the initial lock-in period you can withdraw funds from the child policy to address unexpected expenses regarding child’s education.

- Flexibility :

Child plans offer the flexibility to choose policy term and premium payment term (monthly, quarterly and annually). In case you are investing in ULIP then you have the flexibility to choose the funds you want to invest in.

- Add-on riders :

In order to enhance the coverage of child education plan you can choose to add riders such as critical illness rider, accidental death benefit rider etc.

- Tax benefits :

Child plan premiums are exempted from tax deductions under section 80C of the Income Tax Act, 1961. The maturity amount from a child education policy is tax-free under section 10(10D) # of the Income Tax Act, 1961.

4.Evaluate the company :

Check the company’s solvency ratio, claim settlement ratio and past fund performance (in case of ULIPs).

5.Start Early :

The earlier you start investing in a child policy, the longer you’ll have to build an adequate corpus for your child’s education. A longer investment horizon through a suitable child policy allows you to benefit from the power of compounding, helping you significantly grow your wealth over time.

6.Compare different options :

You can compare various child education plans based of features and returns online or consult an insurance agent before deciding the plan you want to buy.

Tips to Consider While Buying the Best Child Education Plan:

You can consider the following tips while purchasing the best child education plan:

Starting Early

Your investment has more time to grow if you start early. This keeps up with inflation and increases your child's education fund, so you will be ready for significant academic milestones like college or studying abroad.

Avail an Investment Based on Your Requirements

Based on your risk level, choose a child plan that offers guaranteed or market-linked returns. Make sure it matches your current financial situation, future education goals, and the flexibility you need in premium payments and benefits.

Check for Premium Waiver

<p>Ensure the child plan provides a premium waiver benefit. In the event of your death, your child will still receive the maturity amount, as the insurer will cover future premiums. This ensures that they will continue to receive financial aid for their education even in your absence education.</p>

Check for the Partial Withdrawal and Feature

Partial withdrawals are permitted under some plans during the policy's duration. This option is helpful when you need money for short-term educational costs like study materials, coaching programs, or school applications without compromising the overall maturity advantage.

How Early Planning for Child Education Can Benefit Your Child’s Future?

Early planning for your child's future, especially related to their education, is significant, and the reasons are discussed below:

More Savings over Time

A child plan makes the most of compounding if you start early. By the time your child is ready for college, even modest early contributions can grow into a sizable corpus, ensuring you're financially prepared.

...Read More

More Time to Find Better Options

If you start preparing early, you can conduct an in-depth study and choose the best child education plan that fits your objectives. This enables you to assess returns, compare various plans, and make informed long-term decisions.

...Read More

Secures Your Child’s Future and Reduces Your Stress

If you start early, you will not be in a financial bind when your child's schooling begins. When you have enough saved, you can stop worrying about money and concentrate on helping your child succeed academically.

...Read More

Inculcate Financial Responsibility

In addition to protecting your child's future, early preparation teaches them the value of investing and saving. By including children in the process, you can help them understand the importance of financial planning and instill a sense of responsibility.

...Read More

How Much Should You Invest in a Child Plan?

The amount you should invest in a child plan depends on your child’s estimated future education costs adjusted for inflation. To begin with, identify your child’s present educational needs and long-term goals. Is it schooling, a graduate course, engineering, medicine, an MBA, or studies abroad? Understand the prevailing cost for the particular program, adjust it for inflation, and then plan your investment.

For a realistic picture of how expensive education is, here are some data points to consider:

According to the Economic Times primary education in private school tuition costs around ₹1.25 lakhs to ₹1.75 lakhs per annum (f)

As per Invest4Edu, at a private college engineering costs between ₹2 lakhs to ₹10 lakhs/year and an MBA costs ₹5 lakhs to ₹50 lakhs (g).

As per the leading education website Shiksha.com an MBA overseas will cost you ₹10 lakhs to ₹1Crore today, depending on the University (h)

Take a look at the table below to understand how the estimated rising cost of education at the rate of 10% is likely to affect you in a year, the next five years, and subsequently over the next 10 years. It thus highlights why an early investment in a child plan with adequate life cover and savings is not just a smart choice, but essential too.

Education Level |

1 Year |

5 Years |

10 Years |

Primary Education Costs (per annum) |

₹1,37,500 – ₹1,92,500 |

₹2,01,314 – ₹2,81,839 |

₹3,24,218 – ₹4,53,905 |

Undergraduate Costs (BBA/BCom/Law) (per annum) |

₹55,000 – ₹5,50,000 |

₹80,526 – ₹8,05,255 |

₹1,29,687 – ₹12,96,871 |

BTech Costs (per annum) |

₹2,20,000 – ₹11,00,000 |

₹3,22,102 – ₹16,10,510 |

₹5,18,748 – ₹25,93,742 |

MBA Costs at Top Indian Institutions (2 years) |

₹22,00,000 – ₹38,50,000 |

₹32,21,020 – ₹56,36,785 |

₹51,87,485 – ₹90,78,099 |

MBA Costs Overseas (2 years) |

₹11,00,000 – ₹1,10,00,000 |

₹16,10,510 – ₹1,61,05,100 |

₹25,93,742 – ₹2,59,37,425 |

An MBA costing ₹20 lakhs today will cost anywhere over ₹67+ lakhs in 15 years. (i) Do these numbers not urge for preparedness?

“Hope is not a strategy. A child’s future needs a plan, not a prayer.”

To plan smartly, use an online child education planner. This calculator is a free online tool that helps you estimate future costs based on your child’s goals. The inputs needed include your child’s age, target education (inland or overseas), expected inflation, and investment horizon. Remember, the ideal investment depends on your child’s individual aspirations and how soon you will need the funds. With the right plan, every child’s dream, however different, can be achieved.

List of Child Insurance Plans in India Offered by HDFC Life

Securing your child's future is one of the most crucial financial decisions you can opt for. With the gradually rising costs of education, selecting the child insurance plans ensures fulfilling your child's dreams and makes sure to safeguard it during your absence.

HDFC Life provides some of the top child insurance plans in India, which offer both savings and life cover. These plans help you build a strong financial base for your child’s future. Each child plan is made to support important goals like marriage, higher education, or other future needs.

The table below showcases some of the child insurance plans options:

Plan Name |

Type |

Key Benefits |

Best For |

Action |

HDFC Life Click 2 Wealth (UIN: 101L133V03) A Unit Linked Non-Participating Individual Life Insurance Savings Plan |

ULIP |

Wide variety of fund options, comprehensive life coverage, no allocation charges, market-linked returns |

Creation of wealth for a child in the long term |

|

HDFC Life Click 2 Achieve (UIN: 101N186V07) An individual non-participating, non-linked savings life insurance plan |

Savings Plan + Life Insurance |

Comprehensive life coverage, flexible options of payout for children, guaranteed benefits |

Providing security to child’s educational goals |

|

HDFC Life Sampoorn Nivesh Plus (UIN: 101L180V01) A Unit Linked Non-Participating Individual Life Insurance Savings Plan |

Market Linked Returns + Life Insurance |

Multiple options for funds, comprehensive life coverage, loyalty additions |

Balanced savings and career goals |

Top Government Schemes for Child Education (2026)

To provide your child's education with a secure financial future, a number of government-sponsored saving schemes provide stability, tax relief, and competitive interest rates.

The following is a brief comparison of the schemes available in 2026.

Scheme Name |

Type |

Key Benefits |

Eligibility |

Lock-in Period |

Sukanya Samriddhi Yojana |

Government Savings |

High interest, tax benefits#, specifically for a girl child |

Girl child under 10 years |

Till age 21 |

PPF (Public Provident Fund) |

Long-term Savings |

Tax-free# returns, flexible yearly contributions |

Indian citizen |

15 years |

NSC (National Savings Certificate) |

Fixed Income |

Guaranteed fixed interest, tax-saving investment# |

Indian citizen |

5 years |

These plans are best for parents who want to invest long-term in a low-risk plan with the benefits of income tax exemptions under Section 80C#. So select the best according to the age of your child and your time frame for financial planning.

What is the Claiming Process for Children Insurance Plans?

The child plan claim process is simple. The steps to follow are:

Notifying the Insurance Company

Whether it is to claim maturity benefit or death benefit, inform the insurance company. It can be done by accessing the company’s website, sending an email or SMS, calling their toll-free number, or visiting their branch.

Documentation

Claim Form

Fill out the claim form with the following details:

Details of the Child Education Plan

Policy details such as number, date of purchase, and maturity date

Date of the incident and cause of the incident in case of a death benefit

Nominee/beneficiary’s name

Policy Document

Provide the policy document

Medical Records

In case of a death claim you should enclose the following medical records:

Death Certificate

Medical Certificates

Prescriptions

Lab Reports

Proof of Identity

Enclose any one of the following identity proofs:

Aadhar Card

Voter’s ID Card

Driving Licence

PAN

Passport

Incident-related Documents

In case of unnatural death, the following documents will be required:

FIR copy

Post-mortem report

Submitting the Documents

Submit the relevant documents along with the claim form.

Verification and Review

On receiving the claim form along with the documents the insurer will conduct an investigation and verification of the incident. The company will appoint a surveyor wherever necessary.

Claim Settlement

After the investigation and verification are done and the claim is approved, the claim settlement amount is credited to the beneficiary/nominee’s account.

FAQ's on Child Education Plan

What are the best Child Insurance plans?

The best child insurance plan is the one that caters to your child's financial needs the best. Here are some of the child insurance plans you should consider:

1. Sukanya Samriddhi Yojana (SSY)

2. Unit Linked Insurance Plan (ULIP)

3. Endowment Plan

4. Mutual Fund

5. NPS Vatsalya

How can I buy a best child insurance plan online?

Purchasing a best child insurance plan online is quite easy and simple. Simply visit the HDFC Life home page. From the navigation bar, go to "Investment Plan" and click on 'Child Plan’. Then from the interface choose the plan as per your requirement and click on ‘Buy Now’ to initiate your purchase.

What is the eligibility to buy a child insurance plan?

The eligibility criteria to buy a child plan are- the child must be an Indian citizen, the parents or the legal guardian must be an Indian citizen and there are age criteria which vary from plan to plan and insurer to insurer.

What are the tax benefits of children's education plans in India?

There are two types of tax benefits you can enjoy- firstly you will be eligible for tax deductions on the amount of premium paid of up to Rs. 1.5 lakh under Section 80C of Income Tax Act 1961#. Moreover, up to Rs. 2.5 lakh per year is exempted from tax on the life cover or sum assured amount received from the insurer u/s 10(10D).

What are the government plans for child education in India?

Some of the top government policies for child education in India are the Sukanya Samriddhi Yojana, CBSE Udaan Scheme, Dhanlaxmi Yojana, Balika Samriddhi Yojana etc.

Can I customize a child plan as per my specific requirements?

Yes, you can customise a child plan based on your own requirements which can be factors like pay-out structure, policy term, premium amount and other perks aligning with your child’s requirements.

What is the importance of investing in a child plan?

There are several important reasons for investing in a child plan which are- funding higher education, using this policy as collateral during financial constraints, partial withdrawal for medical treatment of the child and tax benefits.

When can one withdraw money from child plan?

One can withdraw money from a child education insurance plan only when it matures. Otherwise, only partial withdrawals are possible. The amount of these varies based on the selected plan. Usually, after five years since policy inception, policyholders can withdraw a maximum of 20% of the fund value without paying any fee or penalty. Also a Lump sum partial withdrawal from the fund is allowed after completion of five policy years, provided the life assured is at least 18 years of age. Partial withdrawal before completion of policy years would result in termination of the policy.

Is child plan tax free?

Child plans are subject to tax benefits on death or maturity claim profits under Sec 10(10D) of Income Tax Act, 1961#. The premiums paid towards insurance plan are also eligible for tax deduction under Section 80C. Benefits are applicable as per prevailing tax laws

When to buy a child plan?

There is no right time to buy a child plan. You should buy it when you are ready and the earlier the better. According to experts, it is ideal to begin a child plan within 90 days of the child's birth as you don’t want to miss out on the compounding effect. The sooner parents start a child insurance plan, lower is the risk and they stand to make better returns.

How will child plan secure your child's future?

Child plans are investment cum insurance plans that help to plan your child's future financial requirements by accumulating money over a period of time. On maturity, a lump sum amount is paid to the child to cover their education or marriage expenses.

Child plans come with Waiver of Premium (WoP) feature which is applicable if the parent dies in a stipulated period. In case of an unfortunate demise, the sum assured is paid to the nominated beneficiary, while the insurance company continues to pay the due premium for the remaining policy term. Upon maturity of the policy, the child stands to receive the maturity amount as mentioned.

You can withdraw money from the child plan during the tenure of the investment. This money can be used for any medical emergency that might arise for the child and reduce the finanaical burden on the family.

Parents can take the right step in fulfilling their responsibility in securing their child’s future by investing in a child plan.

What is child life coverage?

Child life coverage refers to the decided upon amount that the nominee receives in case anything happens to the policyholder during the policy term.

Can I purchase a child insurance plan for my 15-year-old child?

Yes, you can purchase a child plan for your 15-year-old child. However, when it comes to investments, the earlier you start the better.

What is the difference between a nominee and a beneficiary?

In a child plan, the nominee refers to the person who will help look after the child and the policyholder’s financials if anything happens to them during the policy term. The nominee is responsible for ensuring that the money goes to the intended individual. The beneficiary is the child or the individual who should receive the payout from the policy. In certain situations, the nominee and beneficiary can be the same.

Why is beneficiary or nominee important in a child plan?

The beneficiary is the individual who receives the payout from the policyholder or parent. Parents must ensure that their beneficiary is somebody who can handle the responsibility of receiving the child plan benefits. If not, they should appoint a responsible nominee.

What are the Documents Required to Buy a Child Insurance Plan?

The documents required to buy a Child Insurance Plan include - proof of age, proof of identity, proof of income, proof of address, and the proposal form.

How to calculate child education allowance?

A child education planner will be very useful for determining how much a parent needs for his child’s education allowance. It takes inflation, changing lifestyles, and the child’s growing needs into account to arrive at a correct child education allowance figure.

How to select a child education plan?

A child education insurance plan is generally chosen based on the child’s age and the number of investment years. You can also decide whether you want child ULIPs (unit-linked life insurance plans) or guaranteed plans. Factor in the payout method, associated costs, past performance of the plan, and the claim settlement ratio before you select a plan.

When can one withdraw money from a child plan?

In case you are investing in ULIP, then you can choose to partially withdraw after the lock-in period of 5 years to cover any financial emergency or child education expenses.

What is the concept of a child insurance plan?

A child plan provides savings and protection, which ensures your child’s higher education and future goals are financially secure, even if something happens to you.

What is the best age to start a child plan?

The earlier, the better. Beginning a plan when your child is between 0 and 5 years old gives more time for the investment to grow, minimising future financial stress.

Are child insurance plans safer than then any other investment plan?

Yes. They are relatively safer, as they club life with assured or market-associated returns, which ensures your child’s future goals are not impacted by market volatility.

What are high-growth potential child investment plans?

These are market-linked child insurance plans (like Unit-Linked Insurance Plans (ULIPs)) that assist your money in growing at a rate higher than inflation, ensuring your child’s education fund retains its actual value over time.

Need Help to Buy a Right Plan?

Our expert will assist you in buying a right plan for you online.

Reach us between 9 AM - 9 PM IST.

For existing policy related assistance, click here.

A certified expert of HDFC Life will help you.

99.72% Claim Settlement Ratio

For FY 2025-2026

~5 Cr. Number Of Lives Insured

For FY 2024-2025

Disclaimer: By submitting your contact details, you agree to HDFC Life's Privacy Policy and authorize ...Read More

99.72% Claim Settlement Ratio

For FY 2025-2026

~5 Cr. Number Of Lives Insured

For FY 2024-2025

Share your Valuable Feedback

Thank you for submitting your feedback

Here's all you should know about Child Investments.

We help you to make informed insurance decisions for a lifetime.

Popular Searches

- term insurance plan

- term insurance calculator

- Best Investment Plans

- Investment Calculator

- Investment for Beginners

- Guaranteed Returns

- Best Short Term Investments

- Best Long Term Investments

- 1 Crore Investment Plan

- 5 year Investment Plan

- 10 year Investment Plan

- 20 year Investment Plan

- Insurance vs. Investments

- savings plan

- ulip plan

- retirement plans

- health insurance plans

- child insurance plans

- Best Child Investment Plans

- group insurance plans

- saral jeevan bima yojana

- income tax calculator

- bmi calculator

- compound interest calculator

- income tax slab

- Income Tax Return

- benefits of term insurance calculator

- what is term insurance

- why to invest in life insurance

- Ulip vs SIP

- tax planning for salaried employees

- how to choose best child insurance plan

- tips for buying retirement plan

- 1 crore term insurance

- HRA Calculator

- Annuity From NPS

- Retirement Calculator

- Pension Calculator

- What is Investment

- ULIP Calculator

- nps vs ppf

- short term investment plans

- safest investment options

- one time investment plans

- types of investments

- best investment options

- best investment options in India

- Money Back Policy

- life Insurance plans

- life Insurance

- Zero Cost Term Insurance

- critical illness insurance

- Whole Life Insurance

- benefits of term insurance

- types of life insurance

- types of term insurance

- Endowment Policy

- Benefits of Life Insurance

- Term Insurance for NRI

- Term Insurance for Women

- Term Insurance for Self Employed

- child savings plan

- Benefits of Health Insurance

- Health Insurance for Senior Citizens

- Health Insurance for NRI

- Saving Schemes

- Ulip for NRI

- Life Insurance for NRI

- Investment Plans for NRI

- Savings Calculator

- Best Term Insurance Plan for 1 Crore

- features of term insurance

- personal accident insurance

1. Provided all due premiums have been paid and the policy is in force.

^. Save 46,800 on taxes if the insurance premium amount is Rs.1.5 lakh per annum and you are a Regular Individual, Fall under 30% income tax slab having taxable income less than Rs. 50 lakh and Opt for Old tax regime.

## Subject to conditions specified u/s 10(10D) of the Income tax Act, 1961.

HDFC Life Sampoorn Nivesh Plus (UIN: 101L180V01) is a Unit Linked Non-Participating Individual Life Insurance Savings Plan.

HDFC Life Click 2 Wealth (UIN: 101L133V03) is a Unit linked Non- Participating Individual Life Insurance Saving Plan. Life Insurance coverage is available in this product.

HDFC Life Click 2 Achieve (UIN: 101N186V07) A Non-Linked, Non-Participating, Individual, Savings Life Insurance Plan Life Insurance Coverage is available in this product.

Unit Linked Insurance products do not offer any liquidity during the first five years of the contract. The policyholders will not be able to surrender/withdraw the monies invested in Unit Linked Insurance Products completely or partially till the end of fifth year.

Unit Linked Life Insurance products are different from the traditional insurance products and are subject to the risk factors. The premium paid in Unit Linked Life Insurance policies are subject to investment risks associated with capital markets and the NAVs of the units may go up or down based on the performance of fund and factors influencing the capital market and the insured is responsible for his/her decisions.

HDFC Life Insurance Company Limited is only the name of the Insurance Company, The name of the company, name of the contract does not in any way indicate the quality of the contract, its future prospects or returns. Please know the associated risks and the applicable charges, from your Insurance agent or the Intermediary or policy document of the insurer. The various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns.

#Tax benefits & exemptions are subject to the conditions of the Income Tax Act, 1961 and its provisions. Tax Laws are subject to change from time to time. Customer is requested to seek tax advice from his Chartered Accountant or personal tax advisor with respect to his personal tax liabilities under the Income-tax law

a. https://www.localcircles.com/a/press/page/school-fee-increase-survey

b. https://www.shiksha.com/engineering-chp

c. https://www.upgrad.com/study-abroad/articles/cost-of-bachelor-degree-in-usa/

d. https://www.pib.gov.in/PressReleasePage.aspx?PRID=2135927

e. https://fundsindia.com/blog/wp-content/uploads/2025/05/202505-FundsIndia-Wealth-Conversations.pdf

f. http://https/economictimes.indiatimes.com/news/india/the-cost-of-raising-a-child-in-india-school-costs-30-lakh-college-a-crore/articleshow/93607066.cms

g. https://www.invest4edu.com/blog/education-costs-india-trends-financial-planning

h. https://www.shiksha.com/studyabroad/mba-in-abroad-dc11508

i. https://www.crisil.com/en/home/newsroom/press-releases/2023/04/education-inflation-in-india-zooms-past-consumer-price-index.html

ARN: ED/10/25/27496