Explore the range of investment plans from HDFC Life that suit your needs:

With investment plans from HDFC Life you can opt for market linked returns or guaranteed1 returns as per your financial goals -

Contact Us

![]()

Login

![]()

![]() Customers

Customers

![]()

![]() Employees

Employees

![]()

![]() Partner

Partner

![]()

Save tax up to 46,800/-3

Returns that might help you beat inflation

Guaranteed1 Returns

Life Cover

Francis Rodrigues has a decade long experience in the insurance sector, and as SVP, E-Commerce and Digital Marketing, HDFC Life, manages the online sales channel, as well as digital and performance marketing. He has had hands-on experience in setting up sales channels and functional teams from scratch over a career spanning 2 decades.

Whether you are looking to secure your child's education or protect your finances from the impact of inflation, investing early is key. It enables you to create wealth systematically. So, some of the best child investment plans in India that you can consider are discussed below:

ULIPs are among the best child investment plans as they provide the dual advantages of life insurance and investment. They help you create wealth to cover long-term goals such as your children’s higher education and marriage.

Among the 2-part premiums paid towards ULIPs, one part ensures life insurance coverage, and the other part gets invested in various market-linked funds of your preference.

Here are some of its features:

● Flexibility to personalize investments based on your risk appetite.

● Partial withdrawal or liquidity helps to handle immediate expenses.

● Assists in goal-based planning, such as wealth generation or retirement planning.

● Tax deductions are applicable under Section 80C of the Income Tax Act, 19612 on premiums paid subject to the prescribed overall limit of Rs. 1, 50, 000

● Tax-free switching between equity and debt funds.

● Starting to invest in ULIPs early can maximize returns.

● Maturity amount from ULIPs may become tax-free under Section 10(10D) of the Income Tax Act, 1961 subjected to conditions prescribed.

● Death benefits are completely exempted from tax under Section 10(10D) of the Income Tax Act, 1961.

Traditional life insurance plans like endowment plan or whole-life policies provide guaranteed payouts either on maturity or in case of the policyholder’s death. These ensure the child’s needs are met without financial strain, offering safety and predictable returns.

Here are some of its features:

● The maturity benefit provides a lump sum that secures a child’s future. You can use a lumpsum calculator to estimate how this lump sum could grow over time and help with long-term planning.

● Flexibility to pay the premium on a monthly, quarterly, half-yearly and annual basis.

● Beneficiaries receive the sum assured as a death benefit.

● The lump sum received ensures the family’s financial requirements are met.

● Premiums are tax-deductible up to ₹1.5 Lakh under section 80C of the Income Tax Act, 19612

● A traditional life insurance plan, such as an endowment, provides life cover as well as a maturity benefit.

● It is completely safe and promises guaranteed returns.

Similar to ULIPs, IRDAI ensures that the life insurance plans offered by insurers are free from ambiguity and financially sound.

SIPs are such investment plans for children that let parents invest fixed amounts regularly in mutual funds, enabling disciplined saving for long-term goals like education. They benefit from rupee cost averaging, compounding, and flexibility, with child-specific SIPs or equity funds offering better inflation-adjusted returns.

Features that make SIPs a perfect child investment plan is:

● Small, regular investments that grow your wealth through compounding over time.

● You can start SIP with a minimum of ₹500, and the tenure can be for 10 to 15 years.

● Based on your risk tolerance, you can choose between equity and hybrid funds.

● Equity fund investments have return potential that can shield against inflation.

● When the children reach 18 years of age, withdrawal of the whole SIP amount supports their child’s education.

● SIPs offer flexibility to start or stop investments.

● Diversification of a portfolio is possible through investing in multiple funds.

● Investment in Equity linked saving Scheme (ELSS) provides the benefit of claiming deduction up to ₹1.5 Lakh under section 80C of the Income Tax Act, 19612

Fixed Deposits (FDs) and Recurring Deposits (RDs) are among the safest child investment options, offering stability, predictable returns, and protection from market volatility. Parents who are looking for the best investment plan for 5 years for their kids, both FDs and RDs provide excellent options to build a secure corpus for education, marriage, or emergencies but, they differ in deposit structure:

● FDs: A lump-sum investment for a fixed tenure.

● RDs: Small, regular monthly deposits over a chosen period.

Here are some features of fixed deposits:

● Ideal for creating long-term security and even a financial legacy.

● Encourages financial discipline when explained to children.

● Tenure ranges from 7 days to 10 years.

● Early withdrawal allowed with minimal penalty.

● Loan facility up to 90% of the FD value.

● Interest rates: 2.50%–8.50%.

● Section 80TTA of the income tax act, 1961 provide a deduction of up to Rs 10,000 on the income earned from interest on fixed deposits made in bank, co-operative society, post office.

Here are some features of recurring deposits:

● Monthly deposits starting from ₹500.

● Tenure ranges from 6 months to 10 years.

● Builds disciplined saving habits; penalties apply for late payments.

● Interest rates: 2.50%–8.50%.

Both FDs and RDs ensure steady growth, making them reliable tools for child investment plans in India to secure their future.

A government-backed savings scheme for the girl child, it offers high interest rates (reviewed quarterly), tax exemption under Section 80C of the Income Tax Act, 19612, and maturity at age 21. The scheme is part of the Beti Bachao Beti Padhao campaign. Families with a girl child prefer this scheme since, besides incentives, it offers triple tax benefits. Also, early account opening maximises benefits.

Features include:

● When a girl child reaches the age of 10, her parents can open an account in her name.

● The interest amount for this scheme is 8.2% per annum.

● The minimum amount to start the scheme is ₹250, and the maximum is ₹1.5 Lakh.

● The maturity benefit can be availed from 21 years of age.

● Under section 80C of the Income Tax Act, 19612, the deposited amount under the scheme is eligible for tax deduction up to ₹1.5 Lakh.

● Withdrawal is allowed only for educational purposes.

● The returns from this scheme are tax free.

Gold is a traditional investment that holds value and acts as an inflation hedge. You get options like gold exchange-traded funds (ETFs), gold mutual funds, sovereign gold bonds or physical gold in the form of bars or jewellery.

Not only does it have high liquidity, but it also has the power to protect against inflation. This is why it is considered one of the best child investment plans in India.

Here are some reasons to consider gold as your children's investment plan:

● One of the oldest and traditional investment options.

● Offers safety, security, liquidity and profitable returns.

● Returns from gold are proven to be an ideal hedge against inflation.

● A fixed interest rate of 2.5% semi-annually is gained from sovereign gold bonds.

● During the maturity of a gold bond, the amount can be redeemed in INR (₹).

PPF is a government-backed savings scheme, making it one of the safest child investment options. It not only offers fixed, guaranteed returns but also comes with EEE tax status, meaning tax exemption on deposits, interest earned, and maturity amount. This triple benefit makes it highly attractive for long-term child financial planning.

Key features include:

● Deposit Range: ₹500 to ₹1.5 lakh per financial year.

● Interest Rate: 7.1% for FY 2025–26.

● Tenure: 15 years, extendable by 5 years.

● Liquidity: Partial withdrawals allowed after 5 years in emergencies.

● Loan Facility: Option to avail loans against your PPF balance.

● PPF’s stability and tax efficiency make it a reliable cornerstone for a child’s future fund.

● PPF contribution are eligible for deduction under Section 80C , interest earned on investment is tax-free and maturity is also tax-free.

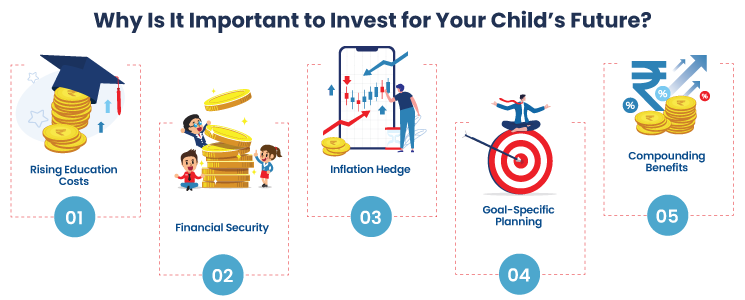

From primary schooling to international university degrees, education expenses are increasing rapidly due to inflation and rising living standards. For example, an MBA that costs ₹25 lakh today could exceed ₹50 lakh by 2040.

Starting investments early helps parents accumulate enough funds to provide quality education without financial strain, ensuring children can pursue their dreams without compromise.

Life is unpredictable, but your child’s future should not be. Child investment plans with insurance components, like ULIPs or endowment policies, provide a safety net in case of a parent’s death or disability. They ensure that education fees, life goals, and essential needs are covered, even if the primary earner is no longer around.

This financial security offers both emotional reassurance and practical stability, allowing children to continue their education without disruption during challenging times.

An inflation hedge refers to an asset that protects against the decreased purchasing power of currency resulting from a lack of value triggered by inflation. Sovereign gold bonds, SIPs and ULIPs are ideal to protect your finances against inflation. So, ₹10 lakh today might only buy goods worth ₹5–6 lakh in 15–20 years, but you can grow this ₹10 lakh over time by investing in the right plan.

Financial goals are similar to destinations at the end of the road, whereas investments are similar to the journey. Whether it is saving up for your child’s MBA course or marriage, in order to reach your destination, you need to take the journey. Investing in multiple instruments will lead you to take that journey and enable you to reach your destination in the future.

In the context of investment, compounding refers to the process by which earnings of an investor are added to their principal amount. Then, that amount grows further with time to help investors reach their financial goals. Compounding child investment plans helps in growing your wealth faster, yet in a strategic manner.

If you are wondering when is the right time to start saving for your children, the right time to start investing in a children investment plan can be well explained with the following critical factors that are to be considered.

Long term investment plans have the advantage of investing less and earning higher returns. Time is a critical factor in wealth creation. So, the earlier you start investing in the best investment plan for child, the lower the burden on your pocket.

Several child investment plans in India provide the benefit of investment as soon as your child is born. Take advantage and start saving from the day your child is born so that you will have a longer time frame to build a huge corpus.

Besides inflation, other expenses like higher education, weddings, etc., can impact your financial goals. It is necessary to start saving early and invest through an investment plan for child to build a stable financial situation, as early investments tend to generate better returns.

Goal-based savings will help assess the financial requirement at a future date to fulfil goals at different life stages. Planning investment early in a children investment plan to align with each financial goal will help build a corpus adequate to fulfil each goal separately.

The cost of education, from primary education to college education, can rise with inflation. Planning early to provide for education expenses at every level of education is important to fulfil the education goals of your children.

The following are the benefits of investing in a child plan:

Choosing investment plan for child like unit-linked plans, will give the dual benefit of financial protection and investment. Your child will get a lump sum in case of any eventualities, and the investment component will provide high returns.

...Read More

The child investment plans in India are life insurance plans. Section 80C under the Income Tax Act 1961 provides for a deduction of up to Rs. 1.50 lakhs in a financial year for these plans. Some plans also offer tax benefits on the maturity/death benefit under Section 10(10D).

...Read More

Child investment plans in India provide a lump sum amount on the maturity of the plan. The choice of the time frame for maturity to align with the financial goals is provided.

...Read More

The ULIP allows partial withdrawals of funds to meet emergency financial needs after the lock-in period.

...Read More

The best investment plan for child ensures the policy remains active in case of an unforeseen incident. Premium payments are waived, but the investment continues to grow until maturity, helping secure your child’s education.

...Read More

The children investment plan serves as emergency reserves with loans available against the policies in times of need.

...Read More

Investing monthly is far easier and more effective than waiting to accumulate a large lump sum later. Regular contributions allow you to benefit from compounding, reduce the burden on your budget, and stay disciplined.

For example**, if your child is 3 years old and you aim to fund an MBBS degree in 15 years, the current cost of ₹30 lakh could rise to around ₹84 lakh at 8% inflation. By starting a SIP in a mix of equity and debt funds at ₹13,000/month (assuming 20% annual returns), you could achieve this comfortably.

Disclaimer - ** Please note that these values are used just for illustrative purpose and actual return may vary.

Use child plan calculators to personalise these numbers based on your child’s age, the goal amount, and your expected return rate. Additionally, learning how to save money from salary and diverting a portion towards such investments can make a big difference in meeting your child’s financial goals.

Sample Monthly Investment Estimates (Assuming 8% Inflation & 20% Returns from SIPs)

Goal |

Current Cost |

Child’s Age |

Target Year |

Estimated Future Cost (at 8% inflation) |

Monthly SIP Needed |

MBBS in India |

₹30 Lakh |

3 years |

In 15 years |

₹95,16,507 |

₹10,113 |

Engineering + MS Abroad |

₹45 Lakh |

5 years |

In 13 years |

₹1,22,38,307 |

₹19,317 |

Marriage |

₹25 Lakh |

2 years |

In 20 years |

₹1,16,52,393 |

₹4,778 |

You can select the best child investment plan by following a few criteria that we have discussed below:

Assess your comfort with investment risks. While investors who are willing to take on more risk in exchange for perhaps larger profits can choose equities mutual funds or Unit Linked Insurance Plans (ULIPs), conservative investors might choose fixed deposits or Public Provident Funds (PPF).

Establish the duration of your investment. Since equity investments usually yield larger returns over more extended time periods, they may be advantageous for long-term objectives like higher education. In contrast, short term investment plans work well for goals that require funds sooner, such as a child's immediate educational needs. Recurring deposits or debt instruments may also be more appropriate for such short-term goals.

Examine all related expenses, such as exit loads, management fees, and administrative charges. Over time, lower expenses can greatly increase net profits which is important while choosing the best investment plan for child. For example, as compared to actively managed funds, index funds frequently offer lower expense ratios.

Think about how simple it is to get your money when you need it. Some investments provide more liquidity than others, including savings accounts or specific mutual funds, while others, like PPF, have lock-in periods. Make sure the investment fits your projected cash flow requirements.

Engage your youngster in financial planning as they get older. By knowing their ambitions, investments can complement their particular academic or professional objectives, encouraging financial literacy and a sense of responsibility.

Make consistent contributions to the investing plan of your choice. For instance, rupee cost averaging can help Systematic Investment Plans (SIPs) in mutual funds, which encourage regular saving practices and may eventually increase returns.

Investments in eligible child-focused financial products can help parents claim tax deductions under Section 80C of the Income Tax Act, 19612. As of FY 2025–26, the maximum deduction limit is ₹1.5 lakh per financial year. Qualifying options include Public Provident Fund (PPF), Sukanya Samriddhi Yojana (SSY), Child ULIPs, and life insurance premiums for a child.

It is essential to note that the total deduction available under section 80C of the Income Tax Act, 1961, considering all the prescribed investments allowed including NPS, PPF, ELSS, Tuition fee, etc under this section should not exceed Rs.1,50,000 per year and is available under the Old Tax Regime only.

To be eligible, the product must be either IRDAI-approved (for insurance-linked plans) or government-notified (for schemes like PPF or SSY). These deductions reduce your taxable income, helping you save tax while building a secure fund for your child’s education, marriage, or other milestones.

Certain child investment plans offer tax-free maturity or withdrawal benefits under Section 10(10D) of the Income Tax Act, 19612subject to the conditions prescribed. This means the proceeds you receive, whether from a ULIP, life insurance plan, or government scheme, are fully exempt from tax, provided conditions are met.

For example, ULIPs with annual premiums up to prescribed limits and SSY accounts (where both interest earned and maturity amount are tax-free) qualify. Exceptions apply if premium-to-sum-assured ratios exceed allowed thresholds or if the plan is not IRDAI-approved or government-notified.

This provision ensures your child’s corpus remains intact without erosion from taxes.

From preschool to higher grades, schooling costs in Tier 1 cities can range from ₹5,000 – ₹50,000 annually for preschool to ₹1.5 lakh or more for high school. With inflation, these figures will only rise.

So, starting early with structured child investment plans like SIPs or ULIPs can help parents build a dedicated education corpus, ensuring quality learning without financial strain. Even a modest monthly SIP can accumulate into a sizable fund for tuition and admission fees over time.

In the modern world, education goes beyond academics. Besides traditional academic sessions, skill development in extracurricular activities such as sports, music, coding, and dance plays a crucial role. As per the increased demands, the charges for these classes are going up, too.

Hence, to cover such expenses, you can consider investing in debt funds or bonds. These instruments offer guaranteed, predictable income. So, if you have a solid budget, you can cover the fees for such classes with the returns gained.

Costs of higher studies such as MBBS, engineering or an MBA degree could go up to as high as ₹50 Lakh by 2035. To cover such a huge amount, investing in a child investment plan with high interest and high returns will be beneficial, such as ULIPs or PPFs. If you are not sure about how much to invest, you can use the investment calculator available online to get clarity.

The cultural as well as financial significance of marriage in India is hard to ignore. Many times, parents struggle with the thought of their children’s marriage. On average, in a tier 1 city, marriage expenses range from a minimum of ₹10 Lakh to ₹25 Lakh. Arranging such a lump sum without a proper strategy is difficult. Therefore, starting with a disciplined investment plan is advisable.

Life is uncertain, and so are emergencies. Having financial stability with the best investment plan for a child reduces quite a lot of the burden when faced with sudden emergencies. To ensure your financial stability during emergencies, starting with a robust investment plan is of utmost importance. You can build your emergency funds with child endowment plans, as such plans offer liquidity and complement your recurring deposits.

The Child Education Planner calculator helps you estimate the future cost of your child’s education based on their current age, the age when they will start the course, the current cost, the inflation rate, and more. It enables you to set realistic savings goals to ensure you prepare for your child’s educational expenses.

The Marriage Expense Calculator aids in estimating the cost of your child’s wedding. It allows you to plan your investments and give your child the wedding they deserve.

The easy-to-use investment calculator empowers you to plan your investments, estimate returns, and navigate the world of financial security.

Securing your child’s future is one of your greatest responsibilities as a parent. A life insurance calculator can help you determine the ideal coverage to safeguard their future. By evaluating your current income, debts, obligations, inflation, expenses, and both short and long-term financial goals, you can ensure your family’s financial stability in the face of unexpected events.

Planning for your child’s future requires discipline, foresight, and the right strategy. Avoiding these common mistakes can help you meet your child’s education, marriage, and life goals without financial stress and ensure a smoother investment process over the long term.

Many parents postpone investing due to misinformation or fear of risks, losing valuable growth years. The key to maximising child investment plans is starting early. For instance, a ₹5,000/month SIP from birth grows steadily over 18 years, creating a sufficient corpus for higher education.

Delaying even by a few years can cause a shortfall of ₹10–20 lakh, forcing you to compromise on your child’s dreams or take costly loans. Early action ensures financial readiness and peace of mind.

The cost of living is increasing consistently over time. During such circumstances, not factoring in inflation, while investing; is a mistake. Among all the best child investment plans, ULIPs are most efficient when it comes to ensuring that your investment is shielding you against inflation.

Choosing a low-return investment option is also not beneficial since it will not be sufficient in the long run. The best way to ensure efficiency in investment is through diversification. Instead of investing a lump sum in a single product, diversifying the same amount into multiple instruments will ensure that you have a balanced financial growth that contributes to your child’s future.

Nobody knows what the future holds. Ignoring life cover, therefore, is a huge mistake. Life cover offers financial security to your family members in your absence, which is not the case with any other child investment options. Whether you want to secure your child’s future or you want to keep your family financially independent, life cover investment is significant.

Investing in child investment plans without a specific goal is like pouring water into an already filled cup. As a parent, making such a mistake could become a disaster. It is always wise to make a strategic plan and budget before starting with the investment. That way, you will know that you are working towards an achievable goal.

Check out HDFC Life Click 2 Achieve1 plan to save for child’s future.

The key factors to consider when choosing a child investment plan are risk involvement, the financial goal, tenure, liquidity, volatility, and the credibility of the Company.

Yes. You can withdraw funds from a child investment plan after the lock-in period.

Long-term investments with both the life cover and the investment component are the best investment plan for child.

Loan against child investment plans depends on the plan that you are going with.

The best plan depends on your financial goals, risk tolerance, and investment horizon. ULIPs are ideal for those seeking market-linked returns with insurance coverage. Traditional life insurance and endowment plans provide a mix of protection and savings. You can consult a financial advisor to determine the most suitable plan for your child’s future.

Investing for a 7-year-old involves considering a combination of factors, including the investment horizon, risk appetite, and financial goals. Child-specific investment plans are popular choices. Tailor the investment strategy based on your child’s future needs and your risk tolerance.

HDFC Life offers child plans that help you build a corpus for your child’s future needs. Our offerings provide financial security for both boys and girls. Parents looking for plans for girls can consider the Sukanya Samriddhi Yojana.

Yes, you can start an SIP for your child. Many financial companies offer SIP options specifically to help you meet your child’s future financial goals. These plans often have a lock-in period until the child reaches adulthood, helping in disciplined savings for their future.

You can buy bonds for your child through various channels, including banks, financial institutions, or online platforms. Consider government savings bonds or fixed-rate bonds for stable returns. Consult with a financial advisor to understand the best options based on your child’s investment horizon.

Investing for a newborn involves a long-term perspective. Consider starting with options like child insurance plans, SIPs, or fixed deposits. Remember, a longer investment horizon allows for a more aggressive and potentially rewarding investment strategy.

Giving kids a piggy bank or starting a small savings account will help them learn to save. To inculcate financial responsibility from an early age, teach them how to create a budget, stress the value of differentiating between necessities and wants, and provide them incentives for saving money.

Conservative ULIPs or balanced mutual funds, which provide a combination of debt and equity exposure to balance risk and return, may be appropriate for a five-year horizon. For people looking for capital protection with modest returns, fixed deposits or recurring deposits are also an option.

Overall, early and thoughtful preparation is necessary to secure your child's financial future. There are a variety of kid investing plans available, each designed to help achieve different financial objectives, including marriage and schooling. These plans offer guaranteed benefits or market-linked returns, life insurance, and possible tax benefits under the 1961 Income Tax Act4. To help you estimate potential future costs and plan your investments effectively, a child education plan calculator can be a useful tool. By evaluating variables such as investment horizon, risk tolerance, and financial goals, parents may select a plan that fits their child's future requirements.

#Tax benefits & exemptions are subject to conditions of the Income Tax Act, 1961 and its provisions.

#Tax Laws are subject to change from time to time.

#Customer is requested to seek tax advice from his Chartered Accountant or personal tax advisor with respect to his personal tax liabilities under the Income-tax law.

1. HDFC Life Click 2 Achieve (UIN: 101N186V07) A Non-Linked, Non-Participating, Individual, Savings Life Insurance Plan Life Insurance Coverage is available in this product.

2. Tax benefits & exemptions are subject to conditions of the Income Tax Act, 1961 and its provisions. Tax Laws are subject to change from time to time. Customer is requested to seek tax advice from his Chartered Accountant or personal tax advisor with respect to his personal tax liabilities under the Income-tax law.

The Unit Linked Insurance products do not offer any liquidity during the first five years of the contract. The policyholders will not be able to surrender or withdraw the monies invested in Unit Linked Insurance Products completely or partially till the end of fifth year.

Unit Linked Life Insurance products are different from the traditional insurance products and are subject to the risk factors. The premium paid in Unit Linked Life Insurance policies are subject to investment risks associated with capital markets and the NAVs of the units may go up or down based on the performance of fund and factors influencing the capital market and the insured is responsible for his/her decisions. HDFC Life Insurance Company Limited is only the name of the Insurance Company, The name of the company, name of the contract does not in any way indicate the quality of the contract, its future prospects or returns. Please know the associated risks and the applicable charges, from your Insurance agent or the Intermediary or policy document of the insurer. The various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns.

3. Save 46,800 on taxes if the insurance premium amount is Rs.1.5 lakh per annum and you are a Regular Individual, Fall under 30% income tax slab having taxable income less than Rs. 50 lakh and Opt for Old tax regime.

4. Subject to conditions specified u/s 80C of the Income tax Act, 1961.

Tax benefits & exemptions are subject to conditions of the Income Tax Act, 1961 and its provisions. Tax Laws are subject to change from time to time.

Customer is requested to seek tax advice from his Chartered Accountant or personal tax advisor with respect to his personal tax liabilities under the Income-tax law.

ARN - ED/08/25/26278