Contact Us

![]()

For NRI Customers

(To Buy a Policy)

(If you're our existing customer)

For Online Policy Purchase

(New and Ongoing Applications)

Branch Locator

For Existing Customers

(Issued Policy)

Fund Performance Check

Login

![]()

![]() Customers

Customers

![]()

![]() Employees

Employees

![]()

![]() Partner

Partner

![]()

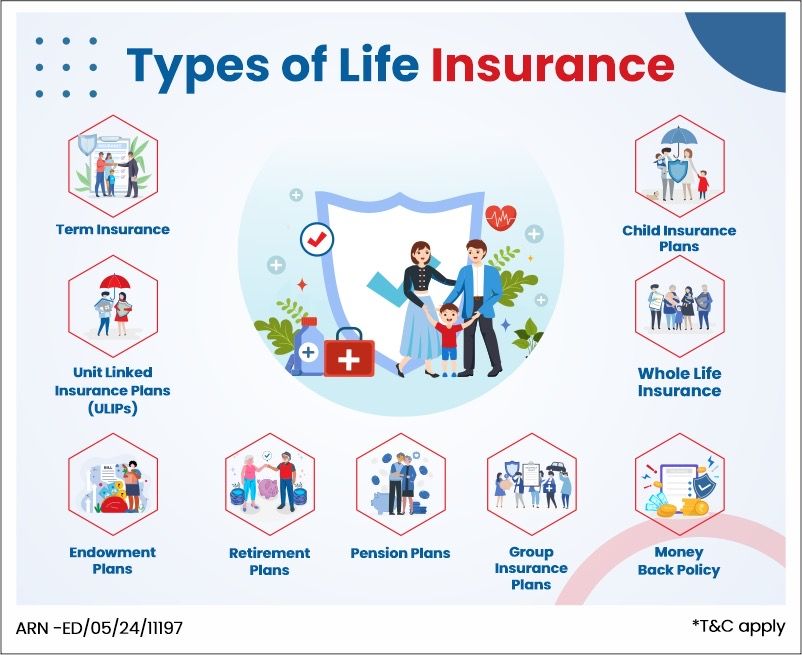

Types of Life Insurance

Life insurance is a contract between an individual and an insurance company. Here, the insurer promises to pay a fixed sum to the nominee in the event of the policyholder's death, or to the policyholder on maturity in some plans.

There are different types of life insurance policies customised to meet varied financial goals. These goals might be family protection, wealth creation or post-retirement planning. Note that the correct policy depends on factors like age, income, financial objectives and risk appetite.

Life Cover of 1 Crore @ 19/day***

To delay is to regret

You may not always be around to take care of your family. And that’s when a term plan ensures your family is well protected.

-

Return of Premium (ROP) Option^

-

Individual Death Claim Settlement Ratio of 99.72%##

-

Immediate payout up to Rs. 5 Lakhs on claim intimation

Types of Life Insurance

Term Life Insurance

Unit Linked Insurance Plan (ULIP)

Endowment Plan

Child Insurance Plan

Whole Life Insurance

Money Back Policy

Retirement Plan

Pension Plan

Group Insurance Plan

Looking to buy a term insurance plan?

With so many considerations, let us help you to make easy decisions for your life insurance needs

What is Life Insurance

A life insurance policy is not just a financial product; it is a well-secured safety net for your loved ones and dependents. Here is the life insurance meaning:

Legal agreement:

A life insurance policy is a formal contract between you (the policyholder) and the insurance company.

Payout on death:

The insurer assures to give the agreed amount to your family members (i.e., nominees) if something happens to you.

Maturity benefit:

A few policies even assure a return of money if you survive the policy term. This makes it a perfect savings/investment product.

Financial security:

It ensures your family members can manage expenditure, repay debts or attain future goals.

Tax benefits*:

Premiums as well as payouts qualify for deductions/exemptions as per Sections 80C and 10(10D) subject to the conditions as specified.

Different plans, different goals:

Cover, benefits and costs differ. So, the correct plan must be based on your income, life goals, and stage of life.

9 Types of Life Insurance

Life insurance comes in distinct forms, each tailored to mitigate specific financial needs as well as life goals. No matter whether you want pure protection, savings, investment, or retirement income, there is a policy suited for you. Below is a snapshot of the 9 major types of life insurance policies in India and what they offer:

Type of Life Insurance |

What It Offers |

Payout Structure |

Features |

Term Life Insurance |

Pure protection plan at a low premium |

Lump sum to the nominee if the policyholder dies during the term |

High sum assured, fixed premium, riders available, no maturity benefit |

Unit Linked Insurance Plan (ULIP) |

Life cover + investment in market-linked funds |

Fund value on maturity or to the nominee on death |

Invests in equity/debt, 5-year lock-in, fund switch option, dual benefit |

Endowment Plan |

Life cover + guaranteed savings |

Maturity amount or death benefit |

Fixed returns, goal-based savings, low risk, bonuses (if applicable) |

Child Insurance Plan |

Life cover + savings for child’s future |

Lump sum at maturity or on claim; premium waiver if the parent dies |

Funds child’s education, premium waiver, dual benefit, lock-in till 18/21 |

Whole Life Insurance |

Coverage for entire life (up to 99–100 years) |

Paid to the nominee on the policyholder's death |

Lifelong protection, cash value in some plans, option to borrow |

Money Back Policy |

Life cover + periodic returns during policy term |

Regular payouts + lump sum on maturity |

Survival benefits, liquidity, bonus additions, fixed-term cover |

Retirement Plan |

Builds a corpus for post-retirement years |

Corpus at vesting; annuity thereafter |

Tax-deferred growth, guaranteed vesting, lump sum + annuity |

Pension Plan |

Regular income after retirement |

Lifetime annuity payments |

Guaranteed monthly income, joint life option, immediate/deferred annuity |

Group Insurance Plan |

Covers multiple individuals under one policy |

Lump sum to nominee/member as per terms |

Covers employees/members, affordable bulk premiums, and includes riders |

The growing variety of life insurance plans reflects the rapid expansion of India’s insurance sector. The domestic market has risen at a compound annual growth rate (CAGR) of 17 per cent over the last two decades and is projected to reach ₹19,30,290 crore (i.e., US$222 billion) by FY26.

In FY24, the industry recorded a 5.1 per cent YoY rise in New Business Premium (NBP) to ₹3.97 lakh crore (US$46.5 billion) while individual NBP grew by 11 per cent to ₹1.74 lakh crore (US$20.36 billion). This specific surge has been supported by over 11 lakh new insurance agents and digitisation, making life insurance more accessible and relevant than ever.

Each plan serves a different purpose, from safeguarding your family's future to creating wealth or ensuring a steady retirement income. Selecting the insurance after prudent consideration allows you to zero in on the right kind of insurance that is in alignment with your financial goals and journey.

Term Insurance

ULIPs

Endowment Plans

Child Insurance Plans

Whole Life Insurance

Money Back Policy

Retirement Plans

Pension Plans

Group Insurance Plans

Term insurance is an affordable and simple form of life insurance. It endows a fixed assured sum of money to the nominee (the individual legally entitled to avail the benefit) if the policyholder expires during the policy term. To keep the plan in active form, the policyholder pays regular premiums (monthly, quarterly or annually).

Unlike savings-linked plans, a term insurance policy does not offer a maturity benefit if the policyholder survives the policy term, unless they go for the return of premium feature. Note that with its low cost and pure protection focus, a term insurance policy is the best way to secure the financial future of your family.

Term Insurance with Critical Illness Rider

A critical illness rider is an optional add-on. This add-on is available with term insurance at an affordable extra premium. It endows a lump sum payout if the policyholder is diagnosed with a serious illness (i.e., cancer, heart attack or stroke) in the course of the policy term.

This amount helps cover treatment costs, recovery expenses, or income loss, while the base life cover of the policy remains unaffected unless stated otherwise in the terms.

Term Insurance with Return of Premium

A term insurance with return of premium (TROP) plan offers both protection and value. In this type of policy, if the policyholder survives the entire term, all the premiums paid are returned as a maturity benefit, unlike regular term plans that only provide a death benefit.

If the policyholder passes away during the term, the nominee still receives the sum assured. While premiums for TROP plans are slightly higher, they highly appeal to those who prefer protection with the add-on benefit of getting their money back.

ULIP is a unique product. This product combines life insurance protection with market-linked investments. When you pay premiums, one part of it goes to securing life cover. The remaining premium gets invested in funds, i.e., equity, debt, hybrid or money market options, based on your financial goals as well as risk appetite.

ULIPs have a five-year mandatory lock-in, which makes them the best for long-term goals like retirement planning, your child’s education or wealth creation. An imperative advantage is the fund-switching flexibility, which permits you to shift between distinct funds without any tax implications, helping you adapt to changing market conditions or risk preferences.

After the lock-in, ULIPs also allow partial withdrawals, making them handy for meeting interim financial needs. While they offer opportunities for market-associated growth, it is important to note that the investment risk is borne completely by the policyholder. ULIPs are transparent too, with disclosures on fund value, NAV as well as charges, which ensures clarity at every life stage.

An endowment plan is a life insurance policy that blends protection with savings, which makes it a dual-benefit product. It ensures that your loved ones are financially secure while also helping you build a guaranteed corpus for the future.

There are two possible outcomes:

● If the policyholder passes away during the term, the nominee receives the death benefit.

● If the policyholder survives the complete term, they get the maturity benefit. This is basically the guaranteed payouts along with bonuses (if the plan is participating).

For example, suppose someone buys an endowment plan of 20 years' term and a sum assured of ₹10 lakh. Here, if the person expires in the course of the term, the nominee will get ₹10 lakh. And in case the person survives, they will receive the maturity amount plus applicable bonuses.

Since endowment policies are non-market-linked as well as low-risk in nature, they are best suited for individuals who want guaranteed returns for goals such as education, retirement or long-term savings.

A child insurance plan is a life insurance product that blends protection with long-term savings, ensuring funds are available for your child's milestones. In such plans, the parent or legal guardian is both the life assured and the premium payer, while the child is the beneficiary.

One vital feature is that the policy continues even if the parent expires. Future premiums in this plan are usually waived. The plan matures when the child reaches adulthood. The maturity benefit can be timed to achieve goals like higher education, skill development or marriage. Based on the insurance, payouts might be provided as a lump sum, periodic amounts or via ULIP-based investment growth.

For instance, a parent buying a child plan equaling ₹10 lakh for their five-year-old can ensure that when the child turns 18, the funds are available for college expenditures, irrespective of life's uncertainties. A few plans also offer partial withdrawals or loyalty additions, adding more flexibility.

Whole life insurance endow cover of up to 99 or even 100 years of age, making sure the death benefit is paid off whenever the policyholder expires. Unlike a term insurance policy, which ends after a fixed duration, this plan assures lifelong protection. This makes it crucial for legacy planning or securing dependents for the long run.

Premiums can either be paid for the entire policy term or for a limited duration, such as 10–15 years, depending on the variant chosen. Many plans also build cash value, and participating policies may add bonuses over time. In some scenarios, a surrender value or maturity benefit is available if the policy is discontinued or survives beyond the defined term.

For example, a 35-year-old purchasing a whole life plan can ensure a guaranteed payout for their children many years later, creating a solid financial legacy. It's important to understand the impact of GST on whole life insurance, as it can influence the premium costs and overall financial planning for the policyholder.

A money back policy is a life insurance plan that combines life cover with periodic survival benefits, making it ideal for those who want liquidity during the policy term. Under this plan, the policyholder gets a percentage of the sum assured at regular intervals. For instance, in a 20-year policy, you might get 20% every five years and the remaining 40% at the time of maturity.

Along with these payouts, the plan still offers a death benefit. If the insured passes away during the policy term, the nominee receives the full sum assured, regardless of the payouts already made. If the policyholder survives till the end, they even get the maturity benefit, which may be bonuses if the plan is participating.

This structure makes money-back policies particularly beneficial for short to mid-term goals. These goals may be paying children’s school fees, funding EMIs or meeting personal expenditures. Unlike endowment plans that pay benefits just at maturity, money back plans offer regular returns as well as protection across the policy term.

Retirement plans are long-term life insurance products. They assist you in building a retirement corpus and ensure a steady income flow in your golden years. These plans work in two phases, i.e., the accumulation phase, where you regularly invest premiums to grow your savings and the annuity or payout phase, where the accumulated corpus offers you a regular income.

At the time of vesting (i.e., retirement), you can withdraw a portion of the corpus as a commuted value while the remaining amount is utilised to purchase an annuity plan. Options are deferred annuity (i.e., income starts after a set period) or immediate annuity (i.e., income starts right away). You can also opt for flexible payouts, i.e., lifetime income, joint life annuity or return of purchase price.

For instance, saving ₹5,000 per month for a span of 20 years can assist you in generating a ₹30,000 monthly pension post-retirement. Moreover, premiums qualify for tax benefits as per Section 80CCC of the Income Tax Act,19611, with tax rules applying during maturity.

Pension plans are particularly designed to provide an assured stream of income post-retirement by converting a lump sum corpus into regular pension payments. Unlike retirement plans that concentrate on building savings over time, pension plans emphasise the income phase once you reach or approach retirement.

These plans can be structured as single premium annuity plans, where you invest a lump sum at once, or as systematic contribution plans that accumulate funds before vesting. At vesting, the accumulated corpus is utilised to purchase an annuity, which then pays you income on a monthly, quarterly or annual basis.

You can select from distinct annuity options, such as a life annuity, a joint annuity for a spouse or an annuity with return of purchase price to your nominee. For example, a 60-year-old investing a sum equaling ₹10 lakh in a pension plan might receive around ₹6,500 per month for life, ensuring financial stability in retirement.

Group insurance plans are policies that provide life insurance coverage to multiple members under a single contract. This is usually offered by employers or associations. In these plans, the employer or group administrator serves as the master policyholder while employees or members automatically become insured as part of their employment or membership.

Coverage may be uniform for all members (e.g., ₹5 lakh each) or vary depending on salary, designation, or role. One of the major advantages is affordability. Group plans usually come with low premiums, minimal paperwork and often zero medical underwriting for most members. The life cover usually ends if the employee leaves the company or exits the group.

For instance, a company may provide a ₹5 lakh group term insurance benefit to every employee as part of their package. Some plans also include add-ons like accidental death or critical illness cover, and may be fully employer-funded or contributory in nature.

How to Buy a Life Insurance Policy in India?

You need to do a few things when purchasing different types of life insurance in India to ensure you have the right coverage. An all-inclusive guide is provided here:

Assess your current and prospective financial obligations and those of your dependents before you buy a life insurance policy. Using a life insurance calculator can help you evaluate your exact insurance needs by factoring in your financial responsibilities, family size, and future goals. This will make it easier to determine how much insurance you need to safeguard your family's financial stability.

Learn more about different life insurance coverage types offered in India, including term, retirement plans, endowment, ULIP, and money-back policies. Ensure you know what each kind can do and the restrictions on payment for critical illness.

Determine which insurance providers are the best by looking at their customer service reputation, financial stability, and claim settlement ratio. Choose a reputable insurance company that has been around for a while.

To calculate the premium for term insurance, you may use an online term insurance calculator. The policyholder's age, coverage amount, policy duration, and extra riders influence the premium rates displayed by the online term insurance calculator.

To calculate the retirement corpus you will need for your retirement, you can use the retirement calculator.

Decide on a life insurance plan that best suits your needs. Once you have finalised your life insurance plan, start filling out the application form. It will require you to share some personal information, such as your name, health habits, date of birth, etc. Any information you share must be true and complete.

Depending upon your age and the amount insured, the insurance company ask for some medical tests to be done. Please note that you must complete all tests on time and work with the insurance company's medical staff.

While applying, make sure that all required documents are attached. Some examples of those documents are birth certificates, utility bills, bank records, driver's licenses and, if needed, medical records.

Be careful to study the insurance policy papers properly before buying insurance. It also covers the plan's advantages, limitations, payment terms, premium due dates, and the rider (if available).

Use your chosen payment method (cash, online payment or cheque) to pay the premium. Pay your premiums on time so the policy remains active, and you may continue to get coverage.

The insurance company will issue the policy paperwork after the papers and payment have been verified. Before putting the paper away, double-check it for accuracy.

In the event of a claim, share all of the information your life insurance company needs, including your policy number, insurer’s contact details, etc., to process your claim amount.

.

How to Choose the Right Type of Life Insurance Policy In India?

Selecting the correct life insurance policy must be based on your goals, responsibilities and affordability. The ideal financial plan differs at distinct life stages (from young professionals securing their first income to parents planning out for their kids' education or retirees looking out for a steady income).

NRIs must also factor in parameters like currency risk, international claim settlement and tax implications before choosing. Below are some decision points to guide you better.

Life Goals

The purpose of life insurance differs for each person. It may be to replace lost income, finance a child’s higher education, secure loan repayments or build a retirement corpus. Figuring out clearly what financial event or responsibility you want to safeguard helps narrow down favourable policy types and benefit structures.

Sum Assured

The sum assured is the guaranteed amount paid to the nominee if the policyholder expires. Experts recommend a coverage of at least 10–15 times your annual income, adjusted for debts and future expenditures. A higher sum ensures your family can comfortably manage living expenditures, liabilities and long-term goals with zero financial stress.

Policy Term

Your policy duration must be in line with when your financial dependents are expected to become self-reliant. For instance, you might select a cover until retirement or until kids complete their education. Purchasing early is advantageous. Why? This is because it locks in lower premiums for longer terms while providing extended protection.

Riders

Riders are optional add-ons. They enhance your base policy by covering particular risks. Popular options are critical illness cover, accidental death benefit and waiver of premium in case of disability. Choosing the correct riders must be based on your health, lifestyle risks and budget, and they can significantly expand your thorough protection.

Credibility of the Insurer

The reliability of the insurer is just as important as the plan. Look out for insurers with a claim settlement ratio of over 95% (note that HDFC Life has a claim settlement ratio of 99.72%## for FY 2025-2026), a strong solvency ratio and good customer service.

Assessing Insurance Regulatory and Development Authority of India (IRDAI) annual reports or independent ratings can assist you in assessing the insurer’s stability, ensuring hassle-free claim settlements.

Why Sum Assured Is an Important Factor When It Comes to Term Insurance?

Sum assured is the assured amount your nominee gets if you, the policyholder, pass away during the term of the policy. It is the main advantage of a term insurance plan, ensuring the financial security of your family.

The amount must be sufficient to replace your income, take good care of outstanding liabilities (like home or car loans) and also finance future needs such as children’s education, marriage or day-to-day expenses.

If the sum assured is very low, the very purpose of term insurance is defeated; your dependents may struggle to maintain their lifestyle or meet financial commitments. A common thumb rule is to go for a cover that is at least 10 to 15 times your annual income. However, it must be customised to factors such as current debts, age, dependents and long-term goals.

Example: A person earning ₹12 lakh per year with a home loan might need a cover of ₹1.2–₹1.5 crore for adequate protection. To make the apt choice, you can make use of an online term insurance calculator that factors in your personal finances as well as provides you with a tailored sum assured recommendation.

1 Crore Term Insurance

2 Crore Term Insurance

5 Crore Term Insurance

1.5 Crore Term Insurance

50 Lakh Term Insurance

75 Lakh Term Insurance

Why Sum Assured is an Important Factor When it Comes to Term Insurance?

Choosing the right sum assured in your term insurance plans is essential for your family's financial security. This sum provides crucial protection in case of unexpected events, giving you peace of mind. A higher sum ensures your loved ones are well-supported, covering debts, education costs, and income replacement. Selecting the right amount is key to ensuring their future is secure. To explore the best term life insurance options and find the ideal sum assured for your needs, click the tabs below.

Tax Benefits on Different Types of Life Insurance in India

Life insurance in India not only protects your family but also helps you save on taxes. Different tax benefits* apply at various stages (premium payments, riders and maturity) under Section 80C, Section 80D and Section 10(10D). By better understanding these provisions, you can maximise your savings while ensuring thorough compliance with tax rules and regulations.

Section 80C

You can claim a deduction of up to ₹1.5 lakh per financial year on premiums paid within the said Financial Year, for yourself, spouse and children under a life insurance policy.

It is essential to note that the total deduction available under section 80C of the Income Tax Act, 19611, considering all the prescribed investments allowed including NPS, PPF, ELSS, Tution fee, etc under this section should not exceed Rs.1,50,000 per year and is available under the Old Tax Regime only.

Section 80D

While Section 80D is mainly for health insurance, it also covers critical illness riders added to life insurance. The deduction under this section is applicable for health insurance premiums paid on the health of self, spouse, children and parents.

The maximum deduction available for the family shall be ₹25,000. In case the insurance premium paid on the health of a senior citizen in the family then an additional deduction of ₹25,000 shall be available. Additionally, they can claim up to ₹25,000 for premiums paid for their parents, wherein the limit is increased up to ₹50,000 if the parents are senior citizens. In totality the maximum deduction available can be ₹1,00,000 if both self/family and parents are senior citizens.

In addition to above, amounts paid on account of preventive check-up for the family, deduction for a maximum ₹5000 can be claimed in a financial year..

Remember, this applies only to health-linked riders, not regular life insurance premiums, making it useful if you’ve enhanced protection with medical benefits.

Section 10(10D)

As per Section 10(10D) 1, payouts from life insurance policies are tax-exempt at the time of maturity , subject to conditions prescribed and death benefits is completely exempt for tax

Death benefit

Completely tax-free for the nominee, irrespective of the premium and sum assured amount

Maturity benefit

Returns are taxed as follows:

In the case of ULIPs issued on or after February 1, 2021, if annual premium does not exceed Rs.2.5 lakh then the maturity proceeds are tax-free subject to other conditions prescribed. However, if the policy does not satisfy the conditions, then at the time of maturity, long term Capital gain (LTCG) will be taxable @ 12.5%, under the head "Income from Capital Gains”, an exemption of LTCG upto Rs 1.25 lac shall also be available annually.

In case of non-ULIP issued on or after April 1, 2023, if annual premium does not exceed Rs. 5 lakhs then the maturity proceeds are tax-free subject to other conditions prescribed. However, if the policy does not satisfy the conditions prescribed then, at the time of maturity, net income under such policy would be chargeable to tax as 'Income from Other Sources' under section 56(2)(xiii) of the Act.

Surrender value

In case of ULIP, if you surrender post the lock in then the surrender value less premium paid is added to your income and taxed at 12.5% under the head "Income from Capital Gains”, an exemption of LTCG upto Rs 1.25 lac shall also be available annually. However, if such policy is compliant with the conditions mentioned in Section 10(10D) then such surrender is tax free. It is also essential to note that if you stop paying premiums before the minimum required period of 5 years, you will lose the tax deduction (if availed) for premiums paid in that year. Also, all deductions you claimed for earlier years will be added back to your income in that year and taxed.

In case of non-ULIP, if you surrender before the policy term such surrender is taxable in case the policy is not compliant under Section 10(10D) of the Income Tax Act, 19611. It is also to be noted that if you stop paying premiums before the minimum required period of 2 years, you will lose the tax deduction for premiums paid in that year. Also, all deductions you claimed for earlier years will be added back to your income in that year and taxed.

Conclusion

Life insurance is not just about protection; it is even about planning for every stage of life. No matter whether you want pure financial security, savings for your child's future, a retirement income or market-linked growth, there is a policy designed for you.

Besides assured benefits or maturity returns, many plans even offer valuable tax benefits1 as per sections 80C, 80D, and 10(10D), making them a prudent addition to your portfolio. The key here is to examine your financial goals, life stage, budget and risk appetite level before choosing.

So, do not procrastinate, zero in on the correct plan today to secure your tomorrow with utter confidence.

Note: If assessee has opted for Old tax regime, assessee shall be eligible to claim deduction under chapter VI-A (like Section 80C, 80D, 80CCC, etc). If assessee opted for New tax regime only few deductions under Chapter VI-A such as 80JJAA, 80CCD(2), 80CCH(2) are available.

FAQs on types of life insurance

What are the types of life insurance?

Life insurance comes in various forms. They are term plans, endowment plans, whole life policies, money-back plans, ULIPs, retirement/annuity plans, child plans and group insurance schemes. These are tailored to mitigate diverse needs such as income protection, savings, retirement planning or financing kids' education.

What are the three major categories of life insurance?

Life insurance policies fall into protection plans (i.e., term insurance), investment-cum-protection plans (i.e., ULIPs, endowment or money-back), and retirement/annuity plans. This categorisation assists policyholders in choosing whether they want pure protection, wealth creation or guaranteed income in later years.

What is the most basic type of life insurance?

The most basic life insurance form is a term insurance plan. It offers high cover at low premiums and pays a lump sum (i.e., sum assured) to the nominee in the event of the policyholder's death. Since it concentrates totally on protection, it does not provide maturity or investment benefits.

Is it possible to purchase two different types of life insurance policies at the same time?

Yes. You can definitely hold multiple life insurance policies simultaneously. For instance, you might purchase a term plan for pure protection and a ULIP or endowment plan for the purpose of savings. Holding multiple policies offers great flexibility, broader coverage and additional financial security for your family.

What type of life insurance is the most popular in India?

Term insurance is a popular life insurance because it offers high coverage at affordable premiums. It is very simple to understand, ensures financial security for dependents and provides mental peace by covering risks with zero need for mixing investment components.

Are riders a type of life insurance policy?

No. Riders are not independent policies. They are add-on benefits that enhance a base life insurance policy. Popular riders are critical illness cover, accidental death benefit and waiver of premium. They endow extra protection against specific risks at a nominal additional cost.

Which type of life insurance policy is best for married couples?

For married couples, a joint life insurance policy works well. It covers both spouses under a single plan and ensures that the surviving partner gets financial support in the event of the other's demise. Alternatively, couples can buy a separate term or endowment plan for greater flexibility.

Which type of life insurance policy is best for single individuals?

Single individuals often find term insurance most suitable. This is because it provides affordable protection. Moreover, ULIPs or endowment plans can be chosen if they want to club protection with savings or investments to build wealth for future needs like buying a home or retirement planning.

Which type of life insurance policy never expires?

A whole life insurance policy never expires as it provides cover for the insured's entire lifetime (often up to 99 or even 100 years). It ensures a death benefit for beneficiaries and might even build a cash value over time, making it a lifelong safety net.

Need Help to Buy a Right Plan?

Our expert will assist you in buying a right plan for you online.

Reach us between 9 AM - 9 PM IST.

For existing policy related assistance, click here.

A certified expert of HDFC Life will help you.

99.72% Claim Settlement Ratio

For FY 2025-2026

~5 Cr. Number Of Lives Insured

For FY 2024-2025

Disclaimer: By submitting your contact details, you agree to HDFC Life's Privacy Policy and authorize ...Read More

99.72% Claim Settlement Ratio

For FY 2025-2026

~5 Cr. Number Of Lives Insured

For FY 2024-2025

1. Tax benefits & exemptions are subject to the conditions of the Income Tax Act, 1961 and its provisions. Tax Laws are subject to change from time to time. Customer is requested to seek tax advice from his Chartered Accountant or personal tax advisor with respect to his personal tax liabilities under the Income-tax law.

*Tax benefits are subject to conditions under Sections 80C, & Section 10(10D) and other provisions of the Income Tax Act, 1961. Tax Laws are subject to change from time to time.

#Provided we have received all the relevant and required documents and no further investigation is required. Claim settlement process would be completed within stipulated timelines once the claim request is approved.

In unit linked policies, the investment risk in the investment portfolio is borne by the policyholder. The Unit Linked Insurance products do not offer any liquidity during the first five years of the contract. The policyholders will not be able to surrender/withdraw the monies invested in Unit Linked Insurance Products completely or partially till the end of fifth year.

Unit Linked Life Insurance products are different from the traditional insurance products and are subject to the risk factors. The premium paid in Unit Linked Life Insurance policies are subject to investment risks associated with capital markets and the NAVs of the units may go up or down based on the performance of fund and factors influencing the capital market and the insured is responsible for his/her decisions. The name of the company, name of the brand and name of the contract does not in any way indicate the quality of the contract, its future prospects or returns. Please know the associated risks and the applicable charges, from your insurance agent or the intermediary or policy document of the insurer. The various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns.

**If a customer is a Salaried individual and has opted for a cover of INR 2 Cr with Limited pay, then the total discounts applicable shall be: 10% +7% = 17% discount on the first year premiums.

***Online Premium for Life Option for HDFC Life Click 2 Protect Supreme Plus (UIN:101N189V03), Male Life Assured, Non-Smoker, salaried, 20 years of age, Policy term of 25 years, Regular pay, Monthly frequency, inclusive of 15% online discount (applicable only for 1st year premium) & exclusive of taxes and levies as applicable. (Monthly Premium of 573/30=19).

^ Available under Life & Life Plus plan options

@As per integrated annual report FY24-25, available on www.hdfclife.com. As of May 2025

##Individual claim settlement ratio by number of policies as per audited annual statistics for FY 25-26

~Tax benefits of ₹ 54,600 (₹ 46,800 u/s 80C & ₹ 7,800 u/s 80D) is calculated at highest tax slab rate of 30% on life insurance premium u/s 80C of ₹ 1,50,000 and health premium (Critical illness rider) u/s 80D of ₹ 25,000. Tax benefits are subject to conditions under section 80C, 80D, 10(10D) as per Income Tax Act, 1961. Please consult your tax advisor for more information.

*Online Premium for Life Option, Male Life Assured, Non-Smoker, 20 years of age, Policy term of 40 years, Regular pay, Monthly frequency, exclusive of taxes and levies as applicable.

ARN - BC/08/25/25975