Contact Us

![]()

For NRI Customers

(To Buy a Policy)

(If you're our existing customer)

For Online Policy Purchase

(New and Ongoing Applications)

Branch Locator

For Existing Customers

(Issued Policy)

Fund Performance Check

Login

![]()

![]() Customers

Customers

![]()

![]() Employees

Employees

![]()

![]() Partner

Partner

![]()

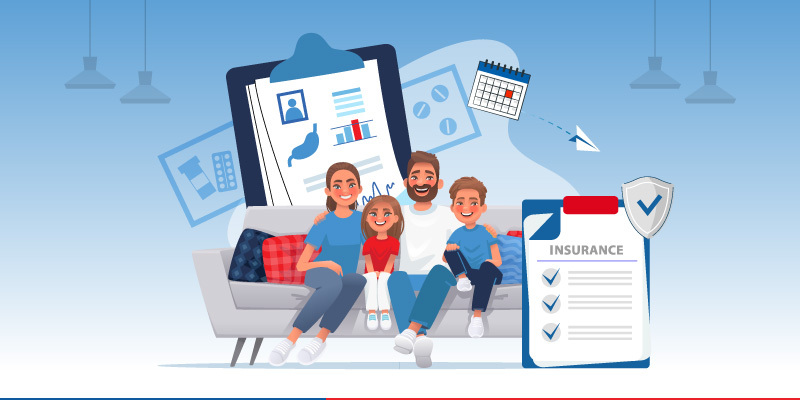

How History of Illness is Important While Buying Term Insurance

In these days where financial support systems matter the most for ensuring a stress-free financial life and for futuristic benefits for the loved ones, a term insurance plan serves your best financial interests. A basic term insurance plan is a pure life insurance plan that provides guaranteed main plan benefit i.e. the sum assured in the event of the policy holder’s demise during the policy term. Although there are no maturity proceeds involved, yet many insurance providers offer return of premium option that entitles the policy holder to receive the paid premiums after maturity of the policy term. While purchasing a term insurance plan, there are certain factors that must be borne in mind. At the time of application for a term insurance policy, a person’s medical history and health record is of prime importance, together with any details pertaining to habits that may have a significant impact on her/his health.

For an insurance provider, complete and thorough information about the policy subscriber’s health is very important. This is because, for an insurance provider, a policy holder suffering from any pre-existing condition like a heart disorder, disability, critical illness etc. comes in the high-risk category of potential investors. In fact, there are certain cases which are liable to be rejected in the application stage due to the presence of any such pre-existing condition. This is where a full disclosure about the history of illness of a person is very important and critical while purchasing a policy. This history may not include only the probable policy holder’s medical history but the general medical history of her/his entire family as well.

As per the guidelines of IRDAI (Insurance Regulatory and Development Authority of India), disclosure of medical history at the time of policy-purchase is mandatory. Moreover, different insurance providers have to follow a common set of guidelines while processing the applications and while evaluating and recording the medic al history of the applicants. This means that the process of medical history-checking and processing the applications is not arbitrary but is transparent. For the applicants, this means that the claim made is liable to get rejected in the event of any withholding of medical information or suppression of medical facts by the policy holder.

While providing coverage for pre-existing medical conditions, insurance providers keep a certain time period as waiting-period before the benefits of the policy can be accrued. This waiting period is generally between 2-4 years, depending on the pre-existing condition or disorder in question. Moreover, the rate of payable premiums is also quite higher than that chargeable when no such conditions are present. However, the higher rate of premiums should not deter you from purchasing the policy as the coverage that is being offered is generally sufficient for your needs and requirements.

HDFC Life offers various term insurance plans that are meant to act as a futuristic platform for the financial security of your loved ones and have been formulated keeping your financial requirements in mind. For details, click on the mentioned link: https://www.hdfclife.com/term-insurance-plans.

Related Articles

- Term Insurance Buying Guide - HDFC Life

- Should You Buy Term Insurance For Senior Citizens?

- How to find best term insurance plan in India

- Are You Underrating Term Insurance Policy

- Understand group term insurance plans

- Why do I need a Term Insurance Plan?

ARN: ED/12/19/17049

Term Plan Articles

Term Plan Articles

Investment Articles

Savings Articles

Life Insurance Articles

Tax Articles

Retirement Articles

ULIP Articles

Subscribe to get the latest articles directly in your inbox

Health Plans Articles

Child Plans Articles

Popular Calculators

Insurance Advisor Articles

Francis Rodrigues

Francis Rodrigues

Francis Rodrigues has a decade long experience in the insurance sector, and as SVP, E-Commerce and Digital Marketing, HDFC Life, manages the online sales channel, as well as digital and performance marketing. He has had hands-on experience in setting up sales channels and functional teams from scratch over a career spanning 2 decades.

Here's all you should know about life insurance.

We help you to make informed insurance decisions for a lifetime.

HDFC Life

Reviewed by Life Insurance Experts

HDFC LIFE IS A TRUSTED LIFE INSURANCE PARTNER

We at HDFC Life are committed to offer innovative products and services that enable individuals live a ‘Life of Pride’. For over two decades we have been providing life insurance plans - protection, pension, savings, investment, annuity and health.

Popular Searches

- Term Insurance Calculator

- Investment Plans

- Investment Calculator

- Investment for Beginners

- Best Short Term Investments

- Best Long Term Investments

- 5 year Investment Plan

- savings plan

- ulip plan

- retirement plans

- health plans

- child insurance plans

- group insurance plans

- income tax calculator

- bmi calculator

- compound interest calculator

- income tax slab

- Income Tax Return

- what is term insurance

- Ulip vs SIP

- tax planning for salaried employees

- HRA Calculator

- Annuity From NPS

- Retirement Calculator

- Pension Calculator

- nps vs ppf

- short term investment plans

- safest investment options

- one time investment plans

- types of investments

- best investment options

- best investment options in India

- Term Insurance for Housewife

- Money Back Policy

- 1 Crore Term Insurance

- life Insurance policy

- NPS Calculator

- Savings Calculator

- life Insurance

- Gratuity Calculator

- Zero Cost Term Insurance

- critical illness insurance

- itc claim

- deductions under 80C

- section 80d

- Whole Life Insurance

- benefits of term insurance

- types of life insurance

- types of term insurance

- Benefits of Life Insurance

- Endowment Policy

- Term Insurance for NRI

- Term Insurance for Women

- Term Insurance for Self Employed

- Benefits of Health Insurance

- Health Insurance for Senior Citizens

- Health Insurance for NRI

- Best Term Insurance Plan for 1 Crore

- personal accident insurance

- Annuity Calculator

- Life Insurance Calculator

- Term Insurance Comparison

- Digital Life Insurance

- Child Education Planner