Contact Us

![]()

For NRI Customers

(To Buy a Policy)

(If you're our existing customer)

For Online Policy Purchase

(New and Ongoing Applications)

Branch Locator

For Existing Customers

(Issued Policy)

Fund Performance Check

Login

![]()

![]() Customers

Customers

![]()

![]() Employees

Employees

![]()

![]() Partner

Partner

![]()

- Term Insurance Calculator

- What is a Term Insurance Calculator?

- Benefits of Using a Term Insurance Calculator?

- Step-by-Step Guide to Use the Term Insurance Calculator *

- How does a term insurance premium calculator work?

- How to calculate your term insurance premium without personal information?

- Common Mistakes People Make After Using a Calculator

- Impact of smoking on term insurance premiums

- How does Occupation Impact Term Insurance Premium Calculation?

- How much term insurance cover do I need?

- Does Age impact your term life insurance premiums?

- Steps to buy a term plan online

- Experiences of term insurance buyers

- What happens when you don’t use a term insurance calculator?

- Term Insurance Plans in India by HDFC Life

- Real-Life Examples based on different Life Stages of Policyholders

- FAQ's on Term Insurance Calculator

- Here's all you should know about life insurance.

- Term Insurance Related Articles

- Customer Reviews

- Share your Valuable Feedback

- Popular Searches

- Disclaimers

17% Online Discount**

60 Critical Illness covered12

No commission guaranteed10

Immediate Claim Payout#

100% Claims guaranteed11

Return of Premium (ROP) Option^

Special Rates for Salaried & women19

0% GST on Premiums#^#

Premium Break Benefit35 for up to 12 months

Get Rs. 1 Cr. Life Cover at just Rs.573/month***

Term Insurance Calculator

Enter accurate details. The term insurance calculator estimates your premium based on age, cover amount, and lifestyle information.

Please wait while we are calculating your term insurance premium

What is a Term Insurance Calculator?

A term insurance calculator is a free online tool that helps you calculate your term insurance premium for the ideal life cover and policy benefits. It evaluates key details such as age, gender, current income, marital status, health, and dependents to guide you in choosing a term insurance that matches your personal and financial objectives. Utilize HDFC Life's term plan calculator to strategically plan your term insurance.

Benefits of Using a Term Insurance Calculator?

These are the benefits of using a term life insurance calculator:

Saves Time

Term insurance calculator allows you to quickly analyse different life insurance plans without calculating policy details manually. It streamlines the process and saves your time and effort so you can focus on other financial decisions.

Ease to Compare Plan Options

A term plan premium calculator enables you to compare multiple plans side by side, helping you evaluate coverage, premium costs, and policy duration to choose the one that best fits your needs.

Helps to Estimate Whether the Premium Fits Your Budget or Not

By entering your financial details and desired coverage, you can determine if the premium amount aligns with your budget and confirm that you select a plan that is both effective and affordable for your pocket. For those seeking complete family protection can consider exploring the best term insurance plan for 1 crore to secure their loved ones financial future.

Helps to Evaluate Sum Assured Amount

The term insurance calculator India helps to evaluate the ideal sum assured based on your income, expenses, and financial obligations. This ensures that your family receives adequate financial protection in case of an unforeseen event.

Available Online for Free

Most term life insurance calculators are available online at no cost and allow you to explore various insurance options from the comfort of your home without any additional expense.

Helps in Making Informed Decisions

By providing detailed insights into policy features of term insurance, its coverage, and premium costs, the calculator helps you make well-informed choices, minimizing the risk of selecting a policy that may not fully meet your requirements.

Note: Know what is term insurance first and then buy term insurance plan for your loved ones.

Step-by-Step Guide to Use the Term Insurance Calculator *

1

1

Enter Your Name

Type your full name as it appears on official ID proofs, such as Aadhar card or PAN card.

...Read More

2

2

Select Your Residential Status

Select "Yes" if you are a Non-Resident Indian (NRI); otherwise, select "No."

...Read More

3

3

Select Your Gender

Choose your gender from the provided options.

...Read More

4

4

Let us know if you consume

Select "Yes" if you are a smoker; otherwise, choose "No."

...Read More

5

5

Enter Your Date of Birth

Select your date of birth from the date picker.

...Read More

6

6

Enter Your Annual Income

Choose the range that best matches your annual income.

...Read More

7

7

Enter Your Mobile Number

Enter your mobile phone number in the provided field.

...Read More

8

8

Enter Your Email

Provide your email address in the given field.

...Read More

9

9

Your Term Insurance Premium

After filling out all the details in the term insurance calculator, click the 'Get Free Quote' button. This will display the calculated premium along with suitable plan options.

...Read More

How does a term insurance premium calculator work?

As mentioned in the above step-by-step guide, you need to provide the following details to calculate your term insurance premium:

- Date of Birth

- Gender

- Tobacco consumption

- Income

- Life cover

The above information about you will help the calculator evaluate the premium for your term insurance customised as per your financial protection needs. Let’s understand how term insurance calculator works with the help of an example:

Ajay, a 25-year-old man, earning 10 Lakhs per annum, wishes to secure his family’s future with a term insurance. After assessing his financial protection needs, he decides that he would need a term insurance of 1 crore. He uses the Term Insurance Calculator by entering his male, smoking, 10 Lakh, 25 years and 1 crore respectively for gender, tobacco consumption habits, income, age and life cover. The estimated premium for Ajay’s term plan was Rs 14127 per month9 for HDFC Life Click 2 Protect Supreme Plus (Life option)10 (UIN:101N189V03).

How to calculate your term insurance premium without personal information?

You can easily calculate an estimated term insurance premium without sharing any personal information. While contact details help us provide personalized service, they're completely optional to basic term insurance quotes.

Two simple ways to get started:

When you know your desired sum assured?

If you know your desired coverage amount, just provide your age, gender and tobacco consumption/smoking status for an instant premium estimate.

When you haven’t decided your sum assured?

If you're unsure about your life coverage needs, share your approximate annual income along with your age, gender and tobacco consumption/smoking for us to help you with a recommended sum assured and its estimated premium..

The above approach lets you explore your options and plan your financial protection needs without the need to provide your personal information.

Common Mistakes People Make After Using a Calculator

Although term insurance calculators offer helpful estimates, many people misinterpret the results. Seeing an affordable premium often leads to rushed decisions, unrealistic expectations, or inadequate life cover. This, in turn, can weaken long-term financial protection if key assumptions and future needs are ignored.

Assuming Calculator Results Are Final and Guaranteed

Many individuals mistakenly believe calculator results are final and guaranteed. In reality, these figures are only indicative and can change after underwriting. The following factors may increase or decrease the final premium:

Detailed health disclosures

Medical test outcomes

Lifestyle habits

Occupation risk assessments

Therefore, understanding this helps set realistic expectations and prevents confusion or disappointment during the policy application process.

Treating the Lowest Premium as the Best Plan

Choosing a term plan or a whole life insurance policy solely because it shows the lowest premium can lead to inadequate protection. Lower premiums often reflect:

Shorter policy tenure

Reduced sum assured

Limited features such as riders and payout options

While affordability matters, it should not come at the cost of meaningful coverage. Hence, a balanced approach ensures dependents receive sufficient financial security when it is most needed.

Underestimating the Required Sum Assured to Reduce Cost

Reducing the sum assured simply to lower premiums is a common but risky mistake. Insufficient coverage may fail to:

Replace income

Clear outstanding liabilities

Support future expenses

The sum assured should be based on financial responsibilities and long-term needs. Therefore, a calculator is meant to guide coverage adequacy first, with cost considered only after protection requirements are met.

Ignoring Policy Tenure While Focusing Only on Premium Amount

Focusing only on premium amounts often leads to selecting a shorter policy tenure. While this lowers immediate costs, it can leave individuals unprotected during later earning years or when dependents still rely on income. Policy tenure should match:

Career span

Family responsibilities

Retirement plans

Hence, prioritising long-term security over short-term savings ensures continuous and reliable financial protection.

Overlooking Rider Relevance after Seeing the Base Premium

Many users focus on the base premium shown by calculators and overlook the value of riders. Riders##* such as critical illness cover or waiver of premium can provide crucial support during illness or income loss, despite increasing cost. These add-ons should be evaluated based on:

Personal risk exposure

Financial vulnerability

Existing insurance coverage

Dependents’ reliance on income

They must not be dismissed solely because they raise the premium amount. This ensures protection remains comprehensive and aligned with real-life uncertainties.

Delaying the Purchase After Calculating an Affordable Premium

After seeing an affordable premium, many people delay purchasing the policy. This can be costly, as premiums often rise with age or changes in health status. Calculator results are time-sensitive and reflect the current risk profile only. Key reasons to act promptly include:

Premiums generally rise with increasing age

New health conditions can raise costs or restrict coverage

Existing insurance coverage

Lifestyle or occupation changes may affect eligibility

Early purchase secures long-term protection at lower rates

Once coverage suitability and affordability are confirmed, timely action helps lock in lower costs and ensures uninterrupted financial protection.

Impact of smoking on term insurance premiums

Smoking is a major factor that affects your life insurance premiums. It also raises the risk of health issues such as throat cancer, lung disease, and heart conditions. Hence smokers are considered high-risk individuals by insurers. Even occasional smoking is considered "smoker" when applying for insurance, which impacts premiums. Insurance companies verify this through medical history checks and nicotine testing.

If you have used tobacco—cigarettes within the last 12 months before purchasing a Term Insurance Plan, you will be categorized as a smoker. This means you will have to pay a higher premium for the same coverage that a non-smoker would gets at a lower cost.

For example4 , Divesh, a 30 year-old healthy male opting for a term insurance policy with a ₹1 crore sum assured may see a 100% increase in premium if he is a smoker (for a policy tenure and premium paying term of 30 years)

Quitting smoking and maintaining a tobacco-free record over time might help reduce your premiums, as insurers may reassess your risk profile during policy renewals or new applications.

Age |

Coverage |

Non-Smoker Premium@@@@ |

Smoker Premium@@@@ |

Extra Cost for Smoking |

Lifetime Extra Cost |

25 |

₹1 crore (30-yr) |

₹ 8,034 |

₹ 14,060 |

₹6,026/year |

₹ 1,80,780 |

30 |

₹1 crore (30-yr) |

₹ 10,294 |

₹ 18,015 |

₹7,721/year |

₹ 2,31,630 |

35 |

₹1 crore (25-yr) |

₹ 14,440 |

₹ 22,152 |

₹7,712/year |

₹ 1,92,800 |

40 |

₹1 crore (20-yr) |

₹ 17,002 |

₹ 29,753 |

₹12,751/year |

₹ 2,55,020 |

Disclaimer: @@@@ The above premium rates ...Read More

How does Occupation Impact Term Insurance Premium Calculation?

When determining the term insurance premium, insurers consider the policyholder’s occupation. Insurers categorise jobs by risk level, such as low, medium, and high. On one hand, jobs in aviation, mining, military, and construction are considered high-risk professions. On the other hand, jobs in government offices, bookkeeping, and teaching are low-risk professions.

Those in riskier professions need to pay higher premiums than those in low-risk occupations. This is because a higher-risk profession has a greater risk of death than a low-risk profession. For example, a pilot will pay a higher premium compared to a school teacher or someone with a desk job.

To estimate the premium, based on your profession, use the HDFC Life online premium calculator. It is easy to use and requires fundamental information.

It is essential to be honest and transparent about your occupation to ensure accurate premiums and smooth claim approval.

How much term insurance cover do I need?

When using our term insurance calculator, we'll ask for a few key details to help estimate your premium based on your desired coverage and to determine how much term insurance do I need. You'll need to provide your:

Annual income

Anticipated years of working

Personal expenses

Estimated annual increase in income

Additionally, we'll consider factors such as your age, gender, date of birth, the type of term insurance plan you prefer, the duration of the policy, and the amount of coverage you want. We also take into account lifestyle factors, such as whether you smoke, and other personal habits that may impact your premium.

By filling in these details, you'll receive an accurate estimated tailored term insurance plan to your needs and circumstances.

...Read More

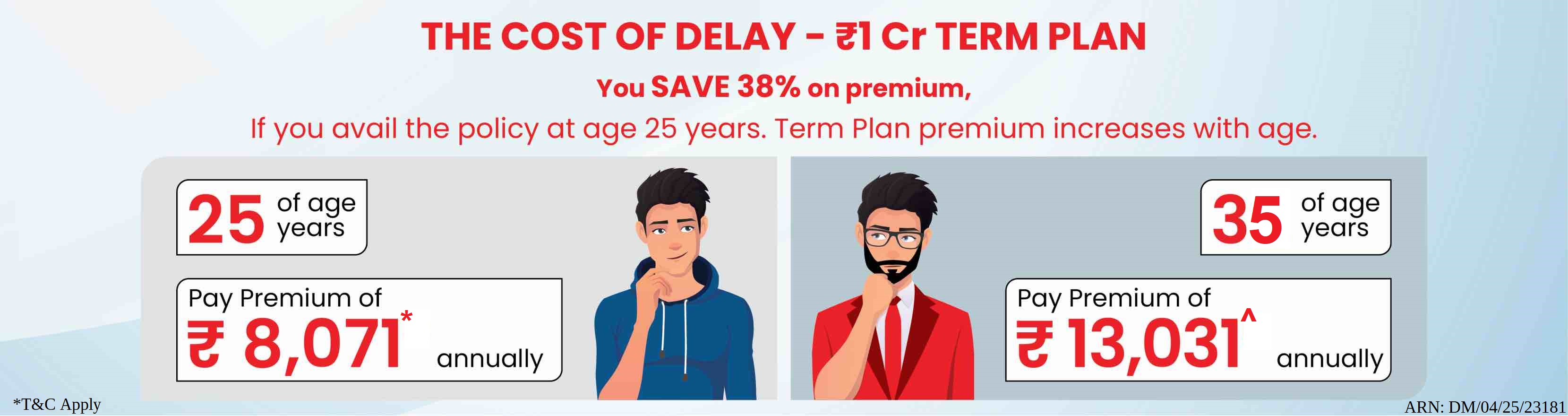

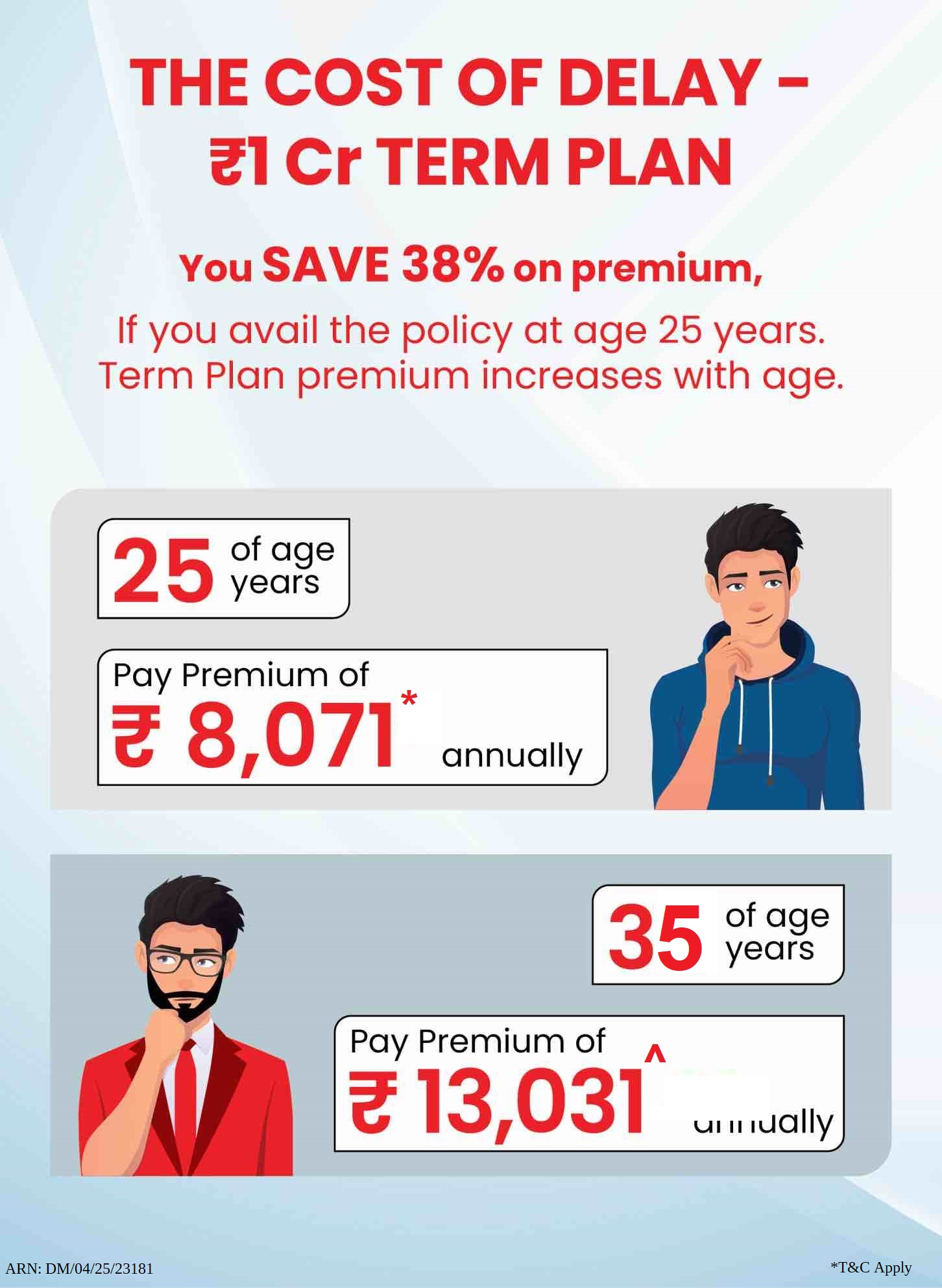

Does Age impact your term life insurance premiums?

You can enjoy term insurance tax benefits on premiums during the policy term, irrespective of age. However, buying a term plan early in in your life helps to keep the premium low. Take a proactive step today—review the table below to understand how premiums increase with age and make the smart decision to invest in term insurance now.

Purchase Age |

Annual Premium (₹1 Crore, till age 60) |

Total Premiums@@@ Paid |

Years of Coverage |

25 years |

₹ 9,025 |

₹3,15,875 |

35 years |

30 years |

₹ 10,294 |

₹3,08,820 |

30 years |

35 years |

₹ 12,658 |

₹3,16,450 |

25 years |

40 years |

₹ 17,002 |

₹3,40,040 |

20 years |

45 years |

₹ 21,691 |

₹3,25,365 |

15 years |

Disclaimer - Read More...

Steps to buy a term plan online

1

1

Evaluate Plans & Calculate Premium

Check the available plan and calculate insurance premium online.

...Read More

2

2

Evaluate add-on options

Enhance your cover by adding riders to your sum assured, then compare your online quotes to find the best plan for your needs.

...Read More

3

3

Fill the application form

Complete the online application form by providing the necessary details and uploading a few documents for verification. After that, our team will schedule a medical test for term life insurance.

...Read More

4

4

Submit and Pay Premiums

Submit the application and pay the premium amount.

...Read More

Experiences of term insurance buyers

We spoke to some term insurance plan customers and here is what they had to say13:

Rohit Verma, 31 years | Pune

I came to know about term insurance in my mid twenties when I started my professional career. Due to lack of awareness at that time I was looking to invest first and grow my wealth. 5 years down the line when I got married to struck me that even though I am investing to grow my wealth but do I have enough financial cover for my family in case of an unfortunate event and the answer was NO! Then I started my research to identify a financial product that would give an adequate life cover. The answer was pretty simple – term insurance. But I should have taken term insurance earlier.

Liza Mathews, 28 years | Mumbai

Once anyone decides to get a term insurance it can be a overwhelming process to go through the entire process of buying it. The same was the case with me. With so many options available online I got a bit confused on which option should I choose? I took a step back and followed the steps – Calculated my premium online, decided whether I needed any add-ons, evaluated the claims settlement ratio of various brands, consulted representatives of various brands and then took an informed decision. The actual process of buying once you have decided it’s that difficult. Good thing is that most of the things are online and hassle free. Now I am proud that I took a term plan for financial protection.

Sanjay Jha, 35 years | Delhi

I come from a family where money management is given a lot of importance. Thanks to the awareness I had I knew it was imperative to financially protect my future before I started investing to grow my wealth. The first thing I did when I started to earn was to get my financial future sorted with a term plan. Now a days it’s not that difficult to get a term life insurance online with so many options to choose from. At the beginning I calculated my premium for 1 crore life cover and then had to go through the usual process for the policy to get issued.

Ashish Dhade, 37 years | Nagpur

For me buying term insurance proved to be a challenging task since I wasn’t conversant about financial products. Since I lacked the understanding of a term insurance, I did a lot of research online and spoke to few of my colleagues who had already bought a term insurance. In my journey to buy term insurance I understood why it was necessary to get term insurance. For me term life insurance has a crucial purpose to fulfill – financial protection. I opted for term insurance at the age of 34 and realized that I could have saved on my premiums if I would have bought it earlier.

Rohit Ghosh, 27 years | Lucknow

When I started to earn, I was inclined towards growing my wealth and started to consult others. My brother introduced me to term life insurance and explained why getting term insurance was a necessity early in life. A term insurance serves the purpose of protecting the financial future of my dependents. Once I understood the benefits of a term plan I went ahead and did some research as to which one I should opt for. There are a few things that helped me make the decision – credibility of the brand, claims settlement ratio and ease of claim settlement.

Priya Yadav, 34 years | Dubai

Being an NRI I wanted to get extensive financial protection for my family. Post my research online, I got to know many life insurance providers in India have started providing term insurance for NRIs at reasonable premiums along with add-on riders such as critical illness and accidental death benefit rider. To my surprise it was a hassle-free experience of buying a term insurance plan.

Manoj Sharma, 34 | Kolkata

I decided to buy term life insurance when I had my first child and realized that as the primary earner, I must secure my family's financial future. To determine the sum assured, I considered our current expenses, future goals like my child’s education, and our home loan. Once sure of the amount, I evaluated riders for critical illness and accidental death. Term insurance is vital for financial planning, so assess all factors carefully before choosing your sum assured and provider.

What happens when you don’t use a term insurance calculator?

When we don’t use a term insurance calculator we might end up choosing a term plan that doesn’t meet our financial protection needs and it’s in our budget. A term insurance calculator gives us a fairly accurate estimation of the term life cover we need along with the premium amount for the same.

1

1

Paying a higher premium

By calculating the premium amount without taking your financial protection needs into consideration you might end up paying a higher premium that doesn’t fit your budget.

...Read More

2

2

Inadequate life cover

By only considering the premium amount while buying the best term life insurance policy in India, you might end up getting a life cover that is inadequate as per your financial needs.

...Read More

About HDFC LIFE

HDFC Life is one of India's leading life insurance company offering a range of individual and group insurance solutions that meet your various needs such as Protection, Pension, Savings & Investment, Health and more.

As per HDFC Life Integrated Annual Report FY 2024 - 2025

SUPERBRAND FOR THE 10TH TIME

Superbrand 2026

SUM ASSURED

13.8 lakh crore

New Business

BRANCHES

652

Across in India

ASSETS UNDER MANAGEMENT

3.4 Lakh crore+

In FY 24-25

NUMBER OF LIVES INSURED

~5 crore

In FY 24-25

As per HDFC Life Integrated Annual Report FY 2024 - 2025

Term Insurance Plans in India by HDFC Life

Here are the term insurance plans offered by HDFC Life:

Term Insurance Plans |

Customer profile |

Sum assured |

Premium amount9 |

Action |

HDFC Life Click 2 Protect Supreme Plus (Life option) (UIN:101N189V03) |

For all between 18-65 years |

1 Crore |

Rs.70614 |

|

HDFC Life Click 2 Protect Elite Plus (UIN:101N182V01) |

Salaried segment |

2 Crore |

Rs.115316 |

|

HDFC Life Click 2 Protect Life (UIN – 101N139V08) |

Salaried segment |

1 Crore |

Rs.119117 |

|

HDFC Life Click 2 Protect Ultimate (UIN: 101N179V01) |

Annual income >Rs.10 Lakhs |

2 Crore |

Rs.140015 |

|

HDFC Life Sanchay Legacy (Life option) (UIN:101N177V04) |

Mature HNI segment |

1.2 Crore |

Rs.1,00,00018 |

Real-Life Examples based on different Life Stages of Policyholders

These related examples tell you why getting the best term insurance plan is smartest decision at different stages in your life.

Nehal, 35 years - A small business owner

Nehal runs a small home-based bakery, and her income often fluctuates with seasonal orders. She wants to protect her family financially, but committing to long-term payments worries her. She finds the HDFC Life Click 2 Protect Supreme Plus ideal, as it offers flexible premium payment options that match her fluctuating cash flow.

Nehal chooses the limited-pay option so she can complete her premium payments earlier, while her life cover continues for years ahead. She also likes that after 5 years, she can consider the premium break benefit35 for up to 12 months if the business slows down, without losing life cover. And as her responsibilities grow, she can increase her insurance coverage30 to keep up with her expanding bakery and family needs.

With this plan, Nehal can focus on growing her dream business while ensuring her family’s future stays protected.

FAQ's on Term Insurance Calculator

ALL CALCULATORS

-

Retirement Calculator

-

Income Tax Calculator

-

Pension Calculator

-

ULIP Calculator

-

Human Life Value Calculator

-

Cost Of Delay Calculator

-

Compound Interest Calculator

-

BMI Calculator

-

Investment Calculator

-

Child Education Planner

-

Marriage Expense Calculator

-

Term Insurance Calculator

-

SIP calculator

-

PPF Calculator

Here's all you should know about life insurance.

We help you to make informed insurance decisions for a lifetime.

Customer Reviews

-

![Amrita]()

I was surprised to see how detailed and informative the information was served to me. It just made my online buying experience worth the time.

Amrita![location]() Delhi

Delhi

-

![Vijayraj]()

Thank you HDFC Life team, you have lived upto your expectation. Your simple claim settlement process just made my life easier.

Vijayraj![location]() Kolkata

Kolkata

-

![Mohit]()

It was a seamless online policy purchase process for me, thanks to HDFC Life.

Mohit![location]() Mumbai

Mumbai

-

![Vibhali]()

Thank you team for your support throughout the claim process and I really appreciate the efforts of everyone involved

Vibhali![location]() Ahmadabad

Ahmadabad

-

![Trisha]()

I was really delighted with the online buying experience. Upto date information and online guidance really helped me. Tx

Trisha![location]() Delhi

Delhi

-

![Bhagyashree]()

My experience with HDFC Life has been really good. I specifically remember the process of online onboarding it was really smooth and hasslefree

Bhagyashree![location]() Mumbai

Mumbai

-

![Sanjna]()

Appreciate you keeping me upto date with your weekly newsletters. Tx

Sanjna![location]() Bangalore

Bangalore

-

![Prerana]()

The online buying process was simple and quick. Good guidance by the HDFC Life team.

Prerana![location]() Jaipur

Jaipur

-

![Anchal]()

The online payment process was smooth and I was able to complete my premium payment easily!

Anchal![location]() Pune

Pune

-

![Shreya]()

HDFC Life representatives explained the product well and helped me buying completing the process online reall quick. Thank you!

Shreya![location]() Lucknow

Lucknow

Share your Valuable Feedback

Thank you for submitting your feedback

HDFC Life

Reviewed by Life Insurance Experts

HDFC LIFE IS A TRUSTED LIFE INSURANCE PARTNER

We at HDFC Life are committed to offer innovative products and services that enable individuals live a ‘Life of Pride’. For over two decades we have been providing life insurance solutions - protection, pension, savings, investment, annuity and health.

Popular Searches

- term insurance

- term insurance calculator

- Investment Plans

- savings plan

- ulip plan

- retirement plans

- health insurance plans

- child insurance plans

- group insurance plans

- saral jeevan bima yojana

- income tax calculator

- bmi calculator

- compound interest calculator

- income tax slab

- Income Tax Return

- benefits of term insurance calculator

- what is term insurance

- why to invest in life insurance

- Ulip vs SIP

- tax planning for salaried employees

- how to choose best child insurance plan

- Retirement Planning

- 1 crore term insurance

- HRA Calculator

- Annuity From NPS

- 2 crore term insurance

- 5 crore term insurance

- 1.5 crore term insurance

- ULIP Calculator

- Pension Calculator

- Money Back Policy

- life Insurance policy

- life Insurance

- Zero Cost Term Insurance

- critical illness insurance

- Whole Life Insurance

- benefits of term insurance

- types of life insurance

- types of term insurance

- Benefits of Life Insurance

- Endowment Policy

- Term Insurance for NRI

- Term Insurance for Women

- Term Insurance for Self Employed

- Benefits of Health Insurance

- Health Insurance for Senior Citizens

- Health Insurance for NRI

- Saving Schemes

- Life Insurance for NRI

- Investment Plans for NRI

- Best Term Insurance Plan for 1 Crore

- features of term insurance

- personal accident insurance

**If a customer is a Salaried individual and has opted for a cover of INR 2 Cr with Limited pay, then the total discounts applicable shall be: 10% +7% = 17% discount on the first year premiums.

##*Riders / Add-Ons can be availed upon payment of additional premium.

^#Online Premium for Life Option for HDFC Life Click 2 Protect Supreme Plus (UIN:101N189V03), Male Life Assured, Non-Smoker, salaried, 20 years of age, Policy term of 25 years, Regular pay, Monthly frequency, inclusive of 15% online discount (applicable only for 1st year premium) & exclusive of taxes and levies as applicable. (Monthly Premium of 376 i.e 13 per day)

^ Available under Life & Life Plus plan options

The product can also be purchased online via company website

~Tax benefits of ₹ 54,600 (₹ 46,800 u/s 80C & ₹ 7,800 u/s 80D) is calculated at highest tax slab rate of 30% on life insurance premium u/s 80C of ₹ 1,50,000 and health premium (Critical illness rider) u/s 80D of ₹ 25,000. Tax benefits are subject to conditions under section 80C, 80D, 10(10D) as per Income Tax Act, 1961. Please consult your tax advisor for more information.

*Online Premium for Life Option, Male Life Assured, Non-Smoker, 20 years of age, Policy term of 40 years, Regular pay, Monthly frequency, exclusive of taxes and levies as applicable.

#Applicable to all in force policies of HDFC Life Click 2 Protect Elite Plus after a waiting period of 1 year, with a base sum assured of INR 2 Crore or more. Claim payout to be restricted to 5 lakhs. Rest of the claim amount will be released after completion of investigation. T&C apply.

##Individual claim settlement ratio by number of policies as per audited annual statistics for FY 25-26

#^#Individual Life Insurance Policies issued on or subsequent to 22nd, September 2025, shall be exempt from GST under the provisions of the Goods and Services Tax, 2017.

***Online Premium for Life Option for HDFC Life Click 2 Protect Supreme Plus(UIN:101N189V03), Male Life Assured, Non-Smoker, salaried, 20 years of age, Policy term of 25 years, Regular pay, Monthly frequency, inclusive of 15% online discount (applicable only for 1st year premium) & exclusive of taxes and levies as applicable. (Monthly Premium of 573 i.e 19 per day).

1. The above are based on the current Income-tax law . Tax benefits are subject to changes in tax laws.

2. Subject to conditions mentioned u/s 80C of the Income tax Act, 1961. The customer is requested to seek tax advice from his Chartered Accountant or personal tax advisor with respect to his personal tax liabilities under the Income-tax law.

3. The premium amount is exclusive of taxes & levies.

4. HDFC Life Click 2 Protect Supreme Plus (UIN: 101N189V03) is a Non-Linked, Non-Participating, Individual, Pure Risk Premium/ Savings Life Insurance Plan. Life Insurance Coverage is available in this product

5. Online Premium for Life Option for HDFC Life Click 2 Protect Supreme Plus (UIN: 101N189V03), Male Life Assured, Non-Smoker, 20 years of age, Policy term of 25 years, Regular pay, Annual frequency, exclusive of taxes and levies as applicable. (Monthly Premium of Rs1047/30=34.9)

6. Discount is applicable only on first year premium.

7. The premium price is subject to change based on variations in customer profile, policy term, premium payment term, and selected death benefits.

8. Online Premium for Life Option for HDFC Life Click 2 Protect Supreme Plus(UIN:101N189V03), Male Life Assured, Non-Smoker, salaried, 20 years of age, Policy term of 25 years, Regular pay, Monthly frequency, inclusive of 15% online discount (applicable only for 1st year premium) & Exclusive of taxes and levies as applicable. (Monthly Premium of 1003 i.e 33 per day).

9. The premium amount is exclusive of taxes & levies.

10. Buying policy online since there is no agent involved, there is no commission to be paid.

11. HDFC Life Click 2 Protect Ultimate(UIN: 101N179V01) A Non-Linked, Non-Participating, Individual, Pure Risk Premium/Savings Life Insurance Plan. The policy must be in force on the date of death, with all premiums fully paid, except for the exclusion clauses mentioned in Part F of the policy document.

12. HDFC Life Health Plus Rider – Non Linked (UIN No: 101B031V02) is a Non-Linked, Non-Participating/ Participating, Pure risk premium, Individual Health rider.

13. The views and opinions expressed in the article are solely of the individual and customer should consult their own financial advisor for any financial matter

14. The above premium rates are for a non-smoker healthy male, age is 25, Policy Term 20 year & Premium Paying Term is 20 year. inclusive of 5% online discount (applicable only for 1st year premium) and exclusive of taxes & levies as applicable. HDFC Life Click 2 Protect Supreme Plus (UIN: 101N189V03) is a Non-Linked, Non-Participating, Individual, Pure Risk Premium/ Savings Life Insurance Plan. Life Insurance Coverage is available in this product

15. The above premium rates are for a non-smoker healthy male, age is 25, Policy Term 20 year & Premium Paying Term is 20 year. inclusive of 5% online discount (applicable only for 1st year premium) and exclusive of taxes & levies as applicable. HDFC Life Click 2 Protect Ultimate(UIN: 101N179V01) A Non-Linked, Non-Participating, Individual, Pure Risk Premium/Savings Life Insurance Plan. Life Insurance Coverage is available in this product

16. The above premium rates are for a non-smoker healthy male, age is 25, Policy Term 20 year & Premium Paying Term is 15 year. inclusive of 5% online discount (applicable only for 1st year premium) and exclusive of taxes & levies as applicable HDFC Life Click 2 Protect Elite Plus (UIN:101N182V01) is a Non-Linked, Non-Participating, Individual, Pure Risk Premium/ Savings Life Insurance Plan. Life Insurance Coverage is available in this product.

17. The above premium rates are for a non-smoker healthy male, age is 25, Policy Term 20 year & Premium Paying Term is 20 year. inclusive of 5% online discount (applicable only for 1st year premium) and exclusive of taxes & levies as applicable. HDFC Life Click 2 Protect Life (UIN – 101N139V08) A Non Linked, Non Participating, Individual, Pure Risk Premium/Savings Life Insurance Plan Life Insurance Coverage is available in this product.

18. The above premium rates are for a non-smoker healthy male, age is 40, Policy Term 15 year & Premium Paying Term is 15 year. inclusive of 5% online discount (applicable only for 1st year premium) and exclusive of taxes & levies as applicable. HDFC Life Sanchay Legacy (UIN:101N177V04) is a Non-Linked, Non-Participating, Individual, Pure Risk Premium/ Savings Life Insurance Plan.Life Insurance Coverage is available in this product.

19. HDFC Life Click 2 Protect Supreme Plus(UIN:101N189V03) is a Non-Linked, Non-Participating, Individual, Pure Risk Premium/ Savings Life Insurance Plan. Life Insurance Coverage is available in this product: 10% discount on first year premium would be applicable for only Salaried customers, under Regular Pay & Limited Pay. A 15% discount on the base premium rates will be applicable for female lives.

20. This is an in-built value addition which can be availed through the Life Rewards app. Please refer to policy documents for Terms & Conditions.

22. The above premium rates are for a non-smoker healthy male, inclusive of 5% online discount (applicable only for 1st year premium) and Inclusive of taxes & levies as applicable. HDFC Life Click 2 Protect Supreme Plus (UIN: 101N189V03) is a Non-Linked, Non-Participating, Individual, Pure Risk Premium/ Savings Life Insurance Plan. Life Insurance Coverage is available in this product.(if you pay premium for 30 years that monthly premium is RS. 1181 or pay premium for 20 years that monthly premium of Rs. 1987. The premium differance is 40%)

23. The above premium rates are for a smoker healthy male, inclusive of 5% online discount (applicable only for 1st year premium) and Inclusive of taxes & levies as applicable. HDFC Life Click 2 Protect Supreme Plus (UIN: 101N189V03) is a Non-Linked, Non-Participating, Individual, Pure Risk Premium/ Savings Life Insurance Plan. Life Insurance Coverage is available in this product.(if he chooses to policy term & pay premium for 30 years the monthly premium is RS. 1181 or he choose premium pay 20 years instead of 30 years the monthly premium is RS. 1528. The premium differance is 22%)

24. The above premium rates are for a smoker healthy male, inclusive of 5% online discount (applicable only for 1st year premium) and Inclusive of taxes & levies as applicable. HDFC Life Click 2 Protect Supreme Plus (UIN: 101N189V03) is a Non-Linked, Non-Participating, Individual, Pure Risk Premium/ Savings Life Insurance Plan. Life Insurance Coverage is available in this product.(he chooses to pay his premiums annually which is Rs. 13299 instead of monthly which is RS. 1181 Per month X 12=14172 annually he saving 6% annually

25. The premium amount is exclusive of taxes & levies.

26. The premiums are inclusive of applicable levies, taxes and 5% discount for 1st year premiums only. The above illustration is for a healthy male applicable for HDFC Life Click 2 Protect Supreme Plus (UIN: 101N189V03) along with Critical illness cover. The monthly premium is RS. 1181 additionally he choose Critical illness cover which monthly premium is Rs. 301. so his premium is increase by 26%.

28. The above premium rates are for a non-smoker healthy male, inclusive of 5% online discount (applicable only for 1st year premium) and Inclusive of taxes & levies as applicable. HDFC Life Click 2 Protect Supreme Plus (UIN: 101N189V03) is a Non-Linked, Non-Participating, Individual, Pure Risk Premium/ Savings Life Insurance Plan. Life Insurance Coverage is available in this product.

29. 10% discount on first year premium would be applicable for only Salaried customers, under Regular Pay & Limited Pay. A 15% discount on the base premium rates will be applicable for female lives.

30. Check the product brochure for more details

31. Available under Life plan option

32. Option to receive the Death Benefit as lump sum followed by regular payouts through Parent Protect Care.

33. 10% discount on first year premium would be applicable for only Salaried customers, under Regular Pay & Limited Pay. A 15% discount on the base premium rates will be applicable for female lives.

34. This built-in value-added service is available through the Life Rewards App, for a limited period as defined by HDFC Life or until the end of the policy term, whichever is earlier. For more information, please refer the product brochure / policy document for the applicable terms and conditions.

35. Applicable if the policy has completed at least five (5) policy years from the risk commencement date and all the due premiums have been received in full and the policy is in force. If the premium break benefit has been exercised in the last 5 policy years, then the next premium break benefit shall not be allowed. The premium break benefit shall not be available during the last policy year of the premium payment term.

36. Applicable for all in force policies after a waiting period of 1 year. Please refer to policy documents for Terms & Conditions HDFC Life Click 2 Protect Supreme Plus (UIN:101N189V03) is a Non-Linked, Non-Participating, Individual, Pure Risk Premium/ Savings Life Insurance Plan. Life Insurance Coverage is available in this product.

This interactive does not constitute an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. HDFC Life Insurance Company Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information reported by the interactive.

The information being provided through this interactive is provided for your assistance/ information only and is not intended to be and must not alone be taken as the basis for an investment decision (“Information”). The recipient/ user assume the entire risk of any use made of this Information. Each recipient /user of this interactive should make such investigation as it deems necessary to arrive at an independent decision while making an investment and should consult his own advisors to determine the merits and risks of such investment. The investment discussed or views expressed may not be suitable for all investors. HDFC Life Insurance Company Limited and its affiliates, group companies, sales staff, financial consultants, officers, directors, and employees may have potential conflict of interest with respect to any recommendation, related information or opinions.

This Information should not be reproduced or redistributed or passed on directly or indirectly in any form to any other person or published, copied, in whole or in part, for any purpose. This Information is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject HDFC Life Insurance Company Limited and its affiliates/ group companies to any registration or licensing requirements within such jurisdiction. The distribution of this Information in certain jurisdictions may be restricted by law, and persons in whose possession this Information comes, should inform themselves about and observe, any such restrictions. The Information given in this interactive is as of the date of this report and there can be no assurance that future results or events will be consistent with this Information. This Information is subject to change without any prior notice. HDFC Life Insurance Company Limited reserves the right to make modifications and alterations to this statement as may be required from time to time. However, HDFC Life Insurance Company Limited is under no obligation to update or keep the Information current.

Neither HDFC Life Insurance Company Limited nor any of its affiliates, group companies, directors, employees, sales staff, financial consultants or representatives shall be liable for any damages whether direct, indirect, special or consequential including health, physical well being, lost revenue or lost profits that may arise from or in connection with the use of the Information. Past performance is not necessarily a guide to future performance.

ARN- ED/04/26/33662