Contact Us

![]()

For NRI Customers

(To Buy a Policy)

(If you're our existing customer)

For Online Policy Purchase

(New and Ongoing Applications)

Branch Locator

For Existing Customers

(Issued Policy)

Fund Performance Check

Login

![]()

![]() Customers

Customers

![]()

![]() Employees

Employees

![]()

![]() Partner

Partner

![]()

Save tax up to 46,800/-15

Returns that might help you beat inflation

Guaranteed2 Returns

Life Cover

What Are Form 15G and Form 15H: Uses, Eligibility & Benefits

Table of Content

3. What Are the Differences Between Forms 15G and 15H?

4. Important Features of Form 15G & 15H

5. Example to Understand Who Can Submit Form 15G & Form 15H

6. Eligibility Criteria for Form 15G and Form 15H

7. When Should You Submit Form 15G & Form 15H?

8. What to Do if I Forget to Submit Form 15G or 15H on Time?

9. What Are the Different Parts of Form 15G?

10. What are the Different Parts of Form 15H?

11. How to Fill Out Form 15G and 15H?

12. Places Where Form 15H and 15G Can Be Submitted

13. TDS Sections Where Form 15G and 15H Can Be Used

14. How to File Form 15G and 15H Online?

15. How to check the Filing Status?

16. Important Considerations while Filling Form 15G and 15Hss

17. Conclusion

Form 15G & Form 15H are self-declaration forms under the Income Tax Act 19611. These forms enable eligible individuals to request that banks, post offices, and institutions such as the EPFO not deduct TDS on specific income.

Both forms are mainly used when income, such as interest on fixed deposits, recurring deposits, EPF withdrawals, or dividend income, is below the taxable limit. Therefore, by submitting these forms, eligible taxpayers can avoid unnecessary TDS and ensure they receive their full earnings without deduction.

What is Form 15G?

Form 15G includes a declaration confirming that the individual’s estimated total income is within tax-exempt limits, ensuring they are not subject to TDS.

Purpose: Its purpose is to prevent TDS deduction when the individual’s total taxable income remains below the basic exemption limit.

Applicability: It applies to incomes like interest from fixed or recurring deposits, EPF withdrawals before five years, or certain other earnings where TDS is applicable.

Eligibility: Form 15G can be submitted by individuals below 60 years of age and Hindu Undivided Families (HUFs).

Form 15G Illustration

A 32-year-old resident of Pune earns ₹1,80,000 annually from a part-time job and ₹22,000 as interest from a fixed deposit. Without Form 15G, the bank would deduct TDS at 10% on the interest income under Section 194A because it exceeds the threshold.

However, since the individual’s total income is below the ₹2,50,000 basic exemption limit, submitting Form 15G ensures no TDS is deducted. As a result, the individual receives the full interest amount, helping maintain regular cash flow and avoid unnecessary refunds later.

What is Form 15H?

In accordance with the provisions of the Income Tax Act 19611, Form 15H requires the individual to declare that their tax liability is nil for the financial year. This separates it from Form 15G, which applies to non-senior individuals and HUFs. Here is a detailed overview of what Form 15H is:

Purpose: It allows them to request non-deduction of TDS when their total taxable income falls below the senior citizen exemption limit.

Applicability: This applies to income sources such as interest from fixed deposits, recurring deposits, and dividend income.

Eligibility: Form 15H is meant exclusively for senior citizens aged 60 years and above.

Form 15H Illustration

A 67-year-old resident of Jaipur earns ₹2,20,000 annually in interest from bank deposits and has no other sources of income. After standard deductions applicable to senior citizens, her taxable income falls below the ₹3,00,000 exemption limit. If she does not submit Form 15H, the bank will deduct TDS under Section 194A because interest income exceeds ₹40,000.

She prevents TDS, allowing her to receive the full ₹2,20,000 without deductions by submitting Form 15H. This helps her manage finances smoothly, especially when relying on interest income for regular expenses.

What Are the Differences Between Forms 15G and 15H?

Below is a comparison table indicating the differences between Form 15G & Form 15H:

Aspects |

Form 15G |

Form 15H |

Who is eligible to file? |

Any Indian resident below 60 years of age, HUF (Hindu Undivided Family), or trust. Companies and firms are not eligible. |

Indian residents aged 60 years or above. Companies, firms, and NRIs are not eligible. |

Income limit |

When total taxable income does not exceed ₹2.5 lakh, OR when interest income is the only source of income and the total income remains below ₹2.5 lakh. |

When final tax liability is nil, OR when interest income is the only source and the total income is below ₹3 lakh (or ₹5 lakh for super senior citizens aged 80+). |

Reason to submit |

Allows individuals and HUFs to save TDS on interest income. |

Allows senior citizens to save TDS on interest income. |

Where to submit? |

Banks, post offices, bond issuers, and EPFO (for corporate or AOP accounts). |

Banks, post offices, bond issuers, and EPFO (for corporate or AOP accounts). |

Validity |

Valid for one financial year; must be submitted annually. |

Valid for one financial year; must be resubmitted annually. |

Where to get the forms? |

Income Tax Department website, banks, insurance companies, and post offices. |

Income Tax Department website, banks, post offices, and insurance companies. |

Mandatory document |

PAN |

PAN |

NRI Eligibility |

Not eligible |

Not eligible |

Important Features of Form 15G & 15H

Forms 15G and 15H have distinct features that define their eligibility rules, age criteria, and income thresholds. Understanding these characteristics enables taxpayers to manage TDS efficiently and avoid unnecessary deductions on eligible income.

Key Features of Form 15G

Scope of Form 15G: Form 15G is a self-declaration form under the Income Tax Act 19611 for resident individuals and Hindu Undivided Families (HUFs) below 60 years of age.

Primary Objective of Form 15G: Its core purpose is to prevent automatic TDS deduction when the individual’s income is below the taxable threshold.

Financial Benefit: By filing Form 15G, taxpayers can maintain an uninterrupted cash flow and avoid the need to claim refunds later, supporting efficient financial management.

Applicability: It does not apply to companies, firms, or non-resident individuals, ensuring it is used only by eligible resident taxpayers. It applies to specific income sources such as interest from fixed deposits, recurring deposits, corporate bonds, and EPF withdrawals.

Income Threshold and Eligibility Requirements: The form is permissible when the individual’s estimated total taxable income falls below the basic exemption limit, ₹2.5 lakh under the old regime or ₹3 lakh under the new regime.

Validity: Form 15G is valid for one financial year and must be submitted afresh annually to continue availing of TDS non-deduction.

For individuals planning for tax-efficient investing, HDFC Life also offers insurance products that help reduce taxable income while providing long-term financial stability.

Key Features of Form 15H

Scope of Form 15H: Form 15H is a self-declaration form specifically for senior citizens aged 60 years and above who are residents under the Income Tax Act 19611.

Primary Objective of Form 15H: Its primary purpose is to safeguard senior citizens from unnecessary TDS deductions on income that ultimately attracts no tax.

Financial Benefit: By using Form 15H, senior citizens receive their full eligible income without TDS cuts, enabling smoother financial planning and improved liquidity management.

Applicability: The applicable exemption limits are ₹3 lakh for senior citizens and ₹5 lakh for super senior citizens aged 80 years and above.

Income Threshold: The form covers income such as interest from fixed and recurring deposits, corporate bonds, debentures, and certain insurance maturity proceeds for which TDS is normally deducted.

Eligibility: To be eligible, the individual's total estimated taxable income must result in a tax liability of zero for the financial year.

Validity: Like Form 15G, Form 15H remains valid for one financial year and must be submitted annually to ensure continued non-deduction of TDS.

Example to Understand Who Can Submit Form 15G & Form 15H

Here in this table, we have illustrated the applicability of Form 15G and Form 15H across various age groups and scenarios.

|

30 years |

50 years |

62 years |

81 years |

Income from salary |

Rs. 1,10,000 |

Rs. 6,20,000 |

- |

- |

Pension income |

- |

- |

Rs. 1,50,000 |

Rs. 1,50,000 |

Fixed deposit interest income |

Rs. 1,05,000 |

Rs. 2,60,000 |

Rs. 2,70,000 |

Rs. 2,80,000 |

Total income before Section 80 deductions |

Rs. 2,15,000 |

Rs. 8,80,000 |

Rs. 4,20,000 |

Rs. 4,30,000 |

Deductions under Section 80 |

Rs. 24,000 |

Rs. 1,20,000 |

Rs. 1,25,000 |

Rs. 55,000 |

Taxable income |

Rs. 1,91,000 |

Rs. 7,60,000 |

Rs. 2,95,000 |

Rs. 3,75,000 |

Minimum exempt income |

Rs. 2,50,000 |

Rs. 2,50,000 |

Rs. 3,00,000 |

Rs. 5,00,000 |

Eligible age |

Below 60 |

Below 60 |

Above 60 |

Above 80 |

Tax on total income is Nil |

Yes |

No |

Yes |

No |

Interest income is less than the basic exemption limit |

Yes |

No |

NA |

NA |

Form 15G/15H Eligibility |

Form 15G |

Not Eligible |

Form 15H |

Form 15H |

Note:

- The 30-year individual with a total taxable income of less than Rs. 2.5 lakh is eligible for Form 15G.

- The individual at the age of 50 years with a total taxable income exceeding Rs. 2.5 lakhs is disqualified from filing Form 15G.

- The 62-year-old person with a total income exceeding Rs. 2.5 lakh but below Rs. 3 lakhs is eligible for Form 15H.

- The individual at the age of 81 years (super senior citizen) with a total income of less than Rs. 5 lakh is eligible for Form 15H.

Eligibility Criteria for Form 15G and Form 15H

Eligibility Criteria for 15G

Eligible Applicants: Form 15G is meant for Indian residents below 60 years of age and Hindu Undivided Families (HUFs) whose estimated taxable income falls within the basic exemption limits.

Income Thresholds: Eligibility is based on having a total income below ₹2.5 lakh under the old tax regime or ₹3 lakh under the new regime.

Tax Liability Requirement: The individual must have zero tax liability for the financial year to qualify. Form 15G can only be submitted by resident individuals and HUFs.

Who Cannot Apply: Companies, firms, and NRIs are not permitted to use this declaration.

Applicable Income Sources: The form applies to eligible income sources where TDS may otherwise be deducted.

Eligibility Criteria for 15H

Eligible Age Group: Form 15H is exclusively for resident senior citizens aged 60 years and above. Super senior citizens aged 80 years or more enjoy a higher exemption threshold.

Exemption Limits: The applicable basic exemption limit is ₹3 lakh for senior citizens and ₹5 lakh for super senior citizens.

Tax Liability Condition: To qualify, the declarant must be an Indian resident whose total taxable income results in nil tax liability for the financial year.

Applicable Income Sources: It applies to income such as interest from bank deposits, corporate bonds, or similar sources where TDS would normally be deducted.

When Should You Submit Form 15G & Form 15H?

The ideal time to submit Form 15G or Form 15H is at the start of the financial year, before any interest income is credited, so that TDS is not deducted during the year. These forms can be submitted only when total taxable income remains within the applicable exemption limits, ₹2.5 lakh, ₹3 lakh, or ₹5 lakh, depending on age and tax regime.

Early submission ensures full receipt of interest without the need for refunds later. Individuals opening deposits mid-year should submit the form before the next interest payout. However, a one-time exception occurred in FY 2020–21, when the government extended the submission deadline due to pandemic-related disruptions.

Consider Rohan, a 28-year-old resident of Bengaluru who has two fixed deposits in the same bank. FD 1 earns ₹18,000 interest annually, and FD 2 earns ₹27,000, a combined total of ₹45,000. Since the bank calculates TDS based on total interest from all deposits, it will deduct TDS at 10% under Section 194A if Form 15G is not submitted.

However, Rohan’s total income for the year is ₹2,10,000, which is below the ₹2.5 lakh basic exemption limit. By submitting Form 15G at the start of the financial year, he ensures no TDS is deducted and receives the full interest amount seamlessly.

What to Do if I Forget to Submit Form 15G or 15H on Time?

If a taxpayer forgets to submit Form 15G or 15H on time, TDS may be deducted on eligible income. This section explains the steps to prevent further deductions and recover any TDS already deducted, ensuring smooth financial management.

Immediately Submit Form 15G or 15H

Taxpayers should submit Form 15G & Form 15H as soon as they realise the delay to stop further TDS on interest income. Most banks allow a 90-day or one-quarter submission window within the financial year.

Once submitted, future interest payouts are credited without TDS, preventing avoidable deductions. Even if TDS has already been deducted for earlier quarters, timely submission ensures no additional deductions occur for the remaining part of the fiscal year.

File IT Returns

Filing income tax returns helps reconcile and recover any TDS already deducted during the year. The Form 26AS statement records all TDS transactions, allowing taxpayers to verify deductions accurately.

If the individual was eligible to submit Form 15G and Form 15H, any excess TDS will be adjusted against the total tax liability or refunded. This process ensures that any unnecessary deductions are returned and provides an official record of deductions, claims, and refunds.

What Are the Different Parts of Form 15G?

The Form 15G is comprised of two parts: Part 1 and Part 2

Part 1 of Form 15G is shown in the figure given below:

In Part 1 of Form 15G, there are multiple fields which are to be filled out by the declarant to avoid TDS deductions. Some of the fields are as follows:

- Name of the assessee

- PAN

- Mobile number

- Address

- Residential status

- Aggregate income amount

- Estimated total income of the previous year

- Date

- Signature of the declarant

Part 2 of the Form 15G is given below:

In Part 2 of the form, there are fields such as:

- Bank details or tenant name that is responsible for providing information about the declarant (individual or entity)

- TAN details

- Amount of income paid

- Complete address

- Date of declaration

- Unique identification number

- Email ID and telephone/mobile number

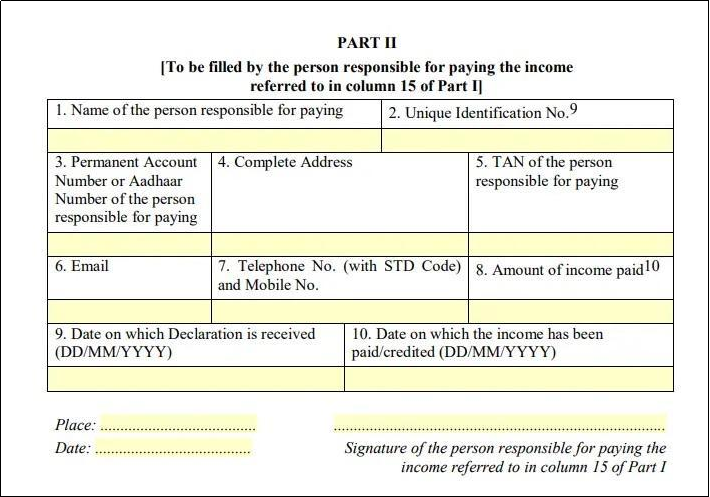

What are the Different Parts of Form 15H?

Like Form 15G, Form 15H is also composed of two parts, Part 1 and Part 2.

The Part 1 of the form is shown below:

Part 1 of 15H has to be filled by the Indian resident individuals who are 60 or above and claiming a non-deduction of tax due to their annual income below the taxable limit as per applicable income tax slabs and rates.

- Name and contact details of the assessee

- PAN or Aadhaar

- Total number of Form 15H submitted

- Estimated income

- Estimated total income in the previous year

The Part 2 of Form 15H is shown below:

Here are some of the fields to be filled in Part 2 of Form 15H:

- Name, contact details and address of the person responsible for paying

- Unique identification number

- PAN number or Aadhaar number

- TAN of Deductor

- Income paid for the fiscal year

How to Fill Out Form 15G and 15H?

Here are the simple steps to follow for filling up Form 15G & Form 15H:

Step 1: Download Form 15G from the Income Tax Department website or collect it from your bank/post office.

Step 2: Read the instructions to understand who can submit and the penalties for making false declarations.

Step 3: Enter your name, PAN (mandatory), status (Individual/HUF), residential status (Resident), and email/phone (optional but helpful).

Step 4: Fill in your address (flat/house number, street, city, PIN, state).

Step 5: Enter the financial year for which the form is being submitted.

Step 6: Provide the estimated total income for that financial year (all sources combined).

Step 7: State the total estimated income on which TDS is to be deducted.

Step 8: Tick/declare that the total estimated income is below the basic exemption limit and tax payable is nil (as per the form’s declaration).

Step 9: Sign the form, write the place and date. If submitting for an HUF, the Karta signs.

Step 10: Attach self-attested PAN copy (banks may insist). Some banks also ask for Aadhaar or account details.

Step 11: Submit to the branch/agency where interest will be paid; keep an acknowledgement/receipt.

Step 12: Keep a copy for your records and for reconciliation with Form 26AS later.

Practical Tips to Fill Up Form 15G and Form 15H

Here are some tips to consider while filling up Forms 15G and 15H:

PAN is Mandatory: Banks will typically reject the form without PAN.

Be Honest: False declarations attract penalties under the Income Tax Act 19611.

Estimate Conservatively: Include all income heads when estimating total income to avoid incorrect declarations.

Online Submission: Some banks accept online/electronic 15G/15H via NetBanking. Follow your bank’s portal if available.

Note: Check Form 26AS after the financial year to confirm no TDS was deducted (or to claim a refund via ITR if TDS was deducted).

Places Where Form 15H and 15G Can Be Submitted

Other than banks, here are some of the places from where Form 15H and 15G can be submitted:

- Insurance companies

- Post offices

- Online income tax portal

- Income tax department offices

- Employer’s offices

TDS Sections Where Form 15G and 15H Can Be Used

Eligible individuals can submit Form 15G & Form 15H to request non-deduction of TDS on specific types of income, provided their total taxable income is below the basic exemption limit. Understanding the relevant TDS sections helps taxpayers identify where these forms can be applied.

Below is a table covering TDS sections, nature of payment, threshold limits, and eligibility for Form 15G and Form 15H (senior citizens):

Section |

Nature of Payment |

Threshold Limit (FY) |

Eligible for Form 15G |

Eligible for Form 15H |

192A |

Premature withdrawal of EPF |

₹50,000 |

Yes |

Yes |

193 |

Interest on securities (debentures, government securities) |

₹5,000 or ₹10,000 |

Yes |

Yes |

194 |

Dividend income |

₹5,000 |

Yes |

Yes |

194A |

Interest from bank, FD, RD, etc. |

₹40,000 (₹50,000 for senior citizens) |

Yes |

Yes |

194EE |

NSS (National Savings Scheme) withdrawal |

₹2,500 |

Yes |

Yes |

194D |

Insurance commission |

₹20,000 |

Yes |

Yes |

194DA |

Life insurance maturity proceeds |

₹1,00,000 |

Yes |

Yes |

194-I |

Rent (land, building, plant, machinery) |

₹50,000 per month / ₹6 lakh per year |

Yes |

Yes |

194K |

Income from mutual fund units |

₹10,000 |

Yes |

Yes |

How to File Form 15G and 15H Online?

An assessee is required to submit Form 15G or 15H received quarterly on the e-filing website. He/she must quote the sequence number in the TDS statement even if no TDS has been deducted.

Here is the step-by-step guide to filing Form 15G & Form 15H online via the official e-filing website of the Income Tax Department.

Step 1: Navigate to the income tax e-filing website.

Step 2: Then, simply click on ‘e-file’ and then click on ‘Prepare & Submit Online Form’.

Step 3: Generate the XML zip file by selecting Form 15G/Form 15H (Consolidated).

Step 4: For filing Form 15G or 15H, it is essential to have a Digital Signature Certificate (DSC). Create the signature for the zip file using the provided utility.

Step 5: Subsequently, use your TAN to log in to the income tax website.

Step 6: Navigate to e-File and submit Form 15G/15H.

Step 7: Choose the form name, financial year, quarter, and filing type.

Step 8: Then, click on ‘validate’ and attach the ZIP and signature files, generated through the Digital Signature Certificate utility.

Step 9: To complete the process, download the DSC Management Utility and click on “Upload”. A success popup will appear on your screen upon successful upload.

How to check the Filing Status?

Here are the steps guiding you to check your filing status:

Step 1: Navigate to the ‘My Account’ section and select ‘View Form 15G/15H’ to access the filing status.

Step 2: The statement status will be initially marked as ‘Uploaded.’

Step 3: Then, the uploaded file will be processed followed by its validation.

Step 4: Following validation, the status will be updated to either ‘Accepted’ or ‘Rejected’ within 24 hours of the upload.

Step 5: Accepted statements are forwarded to CPC-TDS for further processing.

Step 6: If the status is ‘Rejected’, the rejection reason will be stated, and a corrected statement should be re-uploaded.

Important Considerations while Filling Form 15G and 15Hss

Before submitting Form 15G & Form 15H, individuals should carefully evaluate their eligibility and ensure compliance with income tax rules. These forms are declarations and must be filed truthfully to avoid legal consequences.

Eligibility Requirements

Form 15G should not be submitted if your total taxable income exceeds the basic exemption limit. Form 15H (for senior citizens aged 60+) can be filed even if income exceeds the basic exemption limit, provided total tax liability is zero after rebate under Section 87A.

NRIs (Non-Resident Indians) are not eligible to submit either form. These forms are mainly intended for individuals with limited interest income, helping avoid unnecessary TDS when income is genuinely below taxable limits.

Key Filing Rules

Submitting these forms does not replace filing an Income Tax Return (ITR), taxpayers must still file their returns separately. Forms must be furnished to the deductor, banks, post offices, EPFO, NBFCs, or mutual fund houses. They are also available via online portals and mobile banking apps.

Legal Risks of Wrong Declaration

Filing Form 15G & Form 15H fraudulently to avoid TDS despite having taxable income is a false declaration. Under Section 277, penalties include:

6 months to 7 years imprisonment + fine if tax sought to be evaded exceeds ₹25,000.

3 months to 2 years imprisonment + fine in other cases.

Looking to strengthen your tax planning beyond Form 15G and 15H? Explore HDFC Life’s tax-saving insurance plans under Section 80C and 10(10D). These solutions help you reduce tax liability while building long-term financial security for you and your family.

Conclusion

Form 15G & Form 15H serve as important self-declaration tools that help eligible individuals avoid unnecessary TDS on interest and other specified incomes. While Form 15G applies to individuals below 60 and HUFs whose taxable income is below the basic exemption limit, Form 15H is meant exclusively for senior citizens with nil tax liability after rebates.

Timely submission ensures full credit of interest income without deduction and supports smoother financial planning. Therefore, by following the eligibility rules and submitting these forms accurately, taxpayers can manage cash flows efficiently while remaining fully compliant with Income Tax regulations.

FAQs about Form 15G & Form 15H

1. What is the difference between Form 15G & Form 15H?

Ans. Form 15G is applicable for individuals below 60 years of age, HUFs and trust entities. Meanwhile, Form 15H is applicable only to individuals aged 60 or more.

2. What happens if I have submitted Form 15G/Form 15H but I also have taxable income?

Ans. If you have a taxable income and submitted any of the forms by mistake, the form will be invalid and you will have to pay taxes. This taxable income will also include the interest income earned during the year.

3. What is Form 15G used for?

Ans. Form 15G is used for the purpose of declaring your annual taxable income to avoid TDS liability from interest income generated from fixed deposits, recurring deposits or EPF. It is a declaration form under Section 197A of the Income Tax Act.

4. Do I need to submit Form 15G/Form 15H at all bank branches?

Ans. Yes, you have to submit the form at all bank branches where you have an interest-bearing deposit. Apart from banks, you can also submit these forms in a post office if you are holding an interest-bearing deposit account with them.

5. Will my interest income become tax-free if I submit Form 15G/Form 15H?

Ans. If the interest income in a year exceeds Rs. 40,000 (Rs. 50,000 for senior citizens) in a financial year, TDS is levied. However, if your total income is below the tax-exempt limit i.e. Rs. 2.5 lakh, you can avoid TDS deductions by submitting Form 15G or 15H.

6. If I am an NRI, should I submit Form 15G & Form 15H?

Ans. If you are an NRI, you are not eligible to submit Form 15G & Form 15H as a declaration to avoid TDS deduction. Only an Indian resident is eligible to avail the benefits. Therefore if you are an NRI, TDS deductions are compulsory on your interest income.

7. What are Forms 15G and 15H?

Form 15G & Form 15H are self-declaration forms submitted to prevent TDS deduction on interest and certain other types of income. Form 15G is for individuals below 60 and HUFs with income below the basic exemption limit, while Form 15H is exclusively for senior citizens with nil tax liability. These forms help ensure taxpayers receive income without premature TDS deductions.

8. TDS refund vs submitting Form 15G, which is better?

Submitting Form 15G or 15H is better if you meet the eligibility criteria because it prevents TDS from being deducted in the first place. A TDS refund requires filing an Income Tax Return and waiting for the refund to be processed. Using these forms helps avoid cash-flow issues, delays, and paperwork, ensuring interest income is received in full throughout the year.

9. What is the purpose of Form 15G and 15H?

The purpose of Form 15G & Form 15H is to help eligible taxpayers avoid TDS on interest and specific incomes when their tax liability is zero. These forms notify banks or institutions that the individual’s total income is below taxable limits, allowing income to be credited without deductions and easing financial management.

10. Is 15G required for FD?

Yes, Form 15G may be required for fixed deposits if the interest earned crosses the TDS threshold and your total taxable income is below the basic exemption limit. Hence, submitting Form 15G ensures banks do not deduct TDS on FD interest during the financial year, provided you meet all eligibility conditions.

11. What is the 15H form used for?

Form 15H allows senior citizens aged 60 and above to prevent TDS deduction on interest income and other eligible receipts when their tax liability is zero. It ensures that banks and financial institutions credit interest without deduction, helping seniors manage liquidity efficiently while complying with Income Tax rules.

Need Help to Buy a Right Plan?

Our expert will assist you in buying a right plan for you online.

Reach us between 9 AM - 9 PM IST.

For existing policy related assistance, click here.

A certified expert of HDFC Life will help you.

99.72% Claim Settlement Ratio

For FY 2025-2026

~5 Cr. Number Of Lives Insured

For FY 2024-2025

Disclaimer: By submitting your contact details, you agree to HDFC Life's Privacy Policy and authorize ...Read More

99.72% Claim Settlement Ratio

For FY 2025-2026

~5 Cr. Number Of Lives Insured

For FY 2024-2025

Francis Rodrigues

Francis Rodrigues

Francis Rodrigues has a decade long experience in the insurance sector, and as SVP, E-Commerce and Digital Marketing, HDFC Life, manages the online sales channel, as well as digital and performance marketing. He has had hands-on experience in setting up sales channels and functional teams from scratch over a career spanning 2 decades.

Here's all you should know about life insurance.

We help you to make informed insurance decisions for a lifetime.

HDFC Life

Reviewed by Life Insurance Experts

HDFC LIFE IS A TRUSTED LIFE INSURANCE PARTNER

We at HDFC Life are committed to offer innovative products and services that enable individuals live a ‘Life of Pride’. For over two decades we have been providing life insurance plans - protection, pension, savings, investment, annuity and health.

Popular Searches

- Term Insurance Calculator

- Investment Plans

- Investment Calculator

- Investment for Beginners

- Best Short Term Investments

- Best Long Term Investments

- 5 year Investment Plan

- savings plan

- ulip plan

- retirement plans

- health plans

- child insurance plans

- group insurance plans

- income tax calculator

- bmi calculator

- compound interest calculator

- income tax slab

- Income Tax Return

- what is term insurance

- Ulip vs SIP

- tax planning for salaried employees

- HRA Calculator

- Annuity From NPS

- Retirement Calculator

- Pension Calculator

- nps vs ppf

- short term investment plans

- safest investment options

- one time investment plans

- types of investments

- best investment options

- best investment options in India

- Term Insurance for Housewife

- Money Back Policy

- 1 Crore Term Insurance

- life Insurance policy

- NPS Calculator

- Savings Calculator

- life Insurance

- Gratuity Calculator

- Zero Cost Term Insurance

- critical illness insurance

- itc claim

- deductions under 80C

- section 80d

- Whole Life Insurance

- benefits of term insurance

- types of life insurance

- types of term insurance

- Benefits of Life Insurance

- Endowment Policy

- Term Insurance for NRI

- Term Insurance for Women

- Term Insurance for Self Employed

- Benefits of Health Insurance

- Health Insurance for Senior Citizens

- Health Insurance for NRI

- term insurance

1. Tax benefits & exemptions are subject to conditions of the Income Tax Act, 1961 and its provisions. Tax Laws are subject to change from time to time. Customer is requested to seek tax advice from his Chartered Accountant or personal tax advisor with respect to his personal tax liabilities under the Income-tax law.

2. Provided all due premiums have been paid and the policy is in force.

15. Save 46,800 on taxes if the insurance premium amount is Rs.1.5 lakh per annum and you are a Regular Individual, Fall under 30% income tax slab having taxable income less than Rs. 50 lakh and Opt for Old tax regime.

ARN – ED/12/25/29495