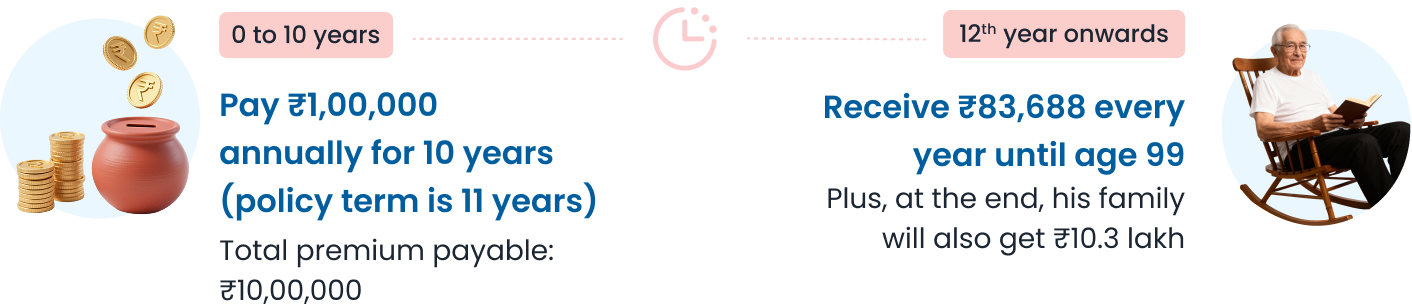

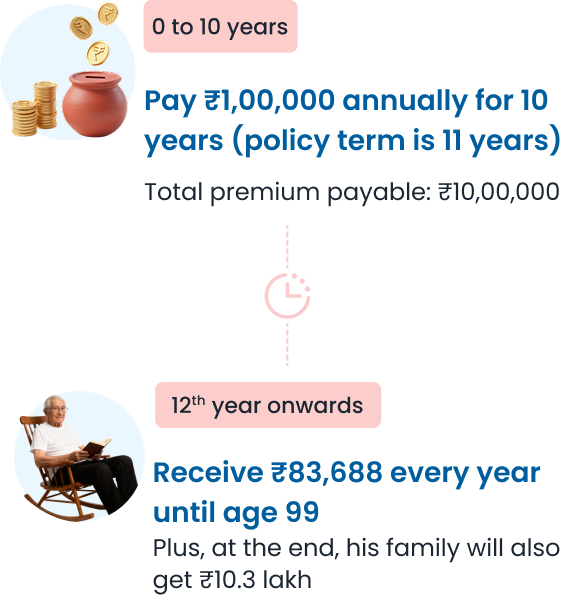

Scenario: Rohan, a 30-year-old software engineer, wants an insurance plan that secures his family, offers guaranteed returns (big lump sum) enough to fund his daughter’s college education or buy a family home.

That’s when Rohan’s advisor tells him about HDFC Life Sanchay Plus – Guaranteed Maturity, which he purchases online through the HDFC Life website.