Contact Us

![]()

For NRI Customers

(To Buy a Policy)

(If you're our existing customer)

For Online Policy Purchase

(New and Ongoing Applications)

Branch Locator

For Existing Customers

(Issued Policy)

Fund Performance Check

Login

![]()

![]() Customers

Customers

![]()

![]() Employees

Employees

![]()

![]() Partner

Partner

![]()

Save tax up to 46,800/-@

Returns that might help you beat inflation

Guaranteed@@ Returns

Life Cover

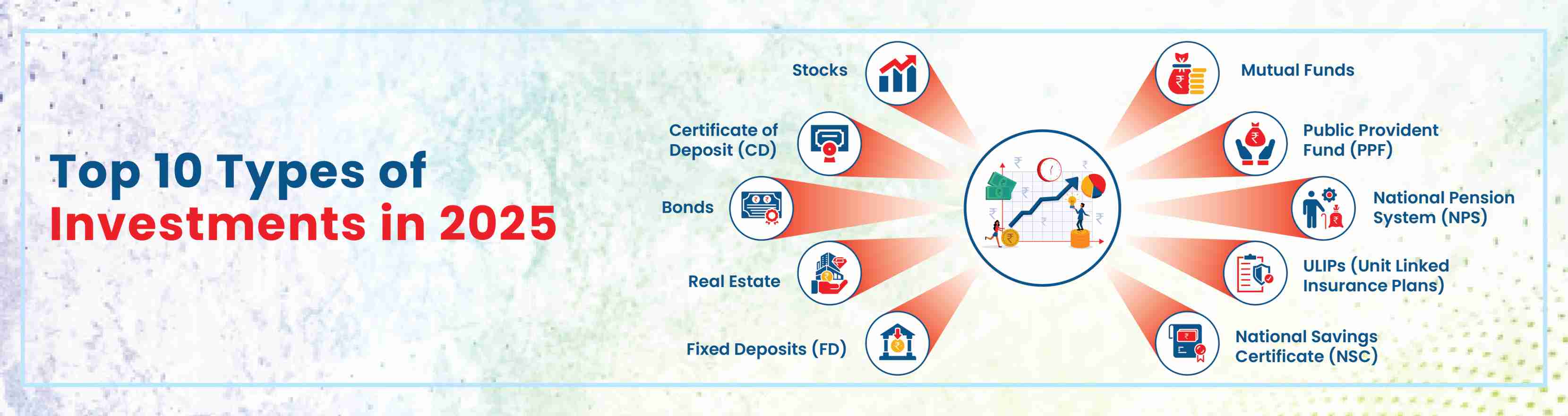

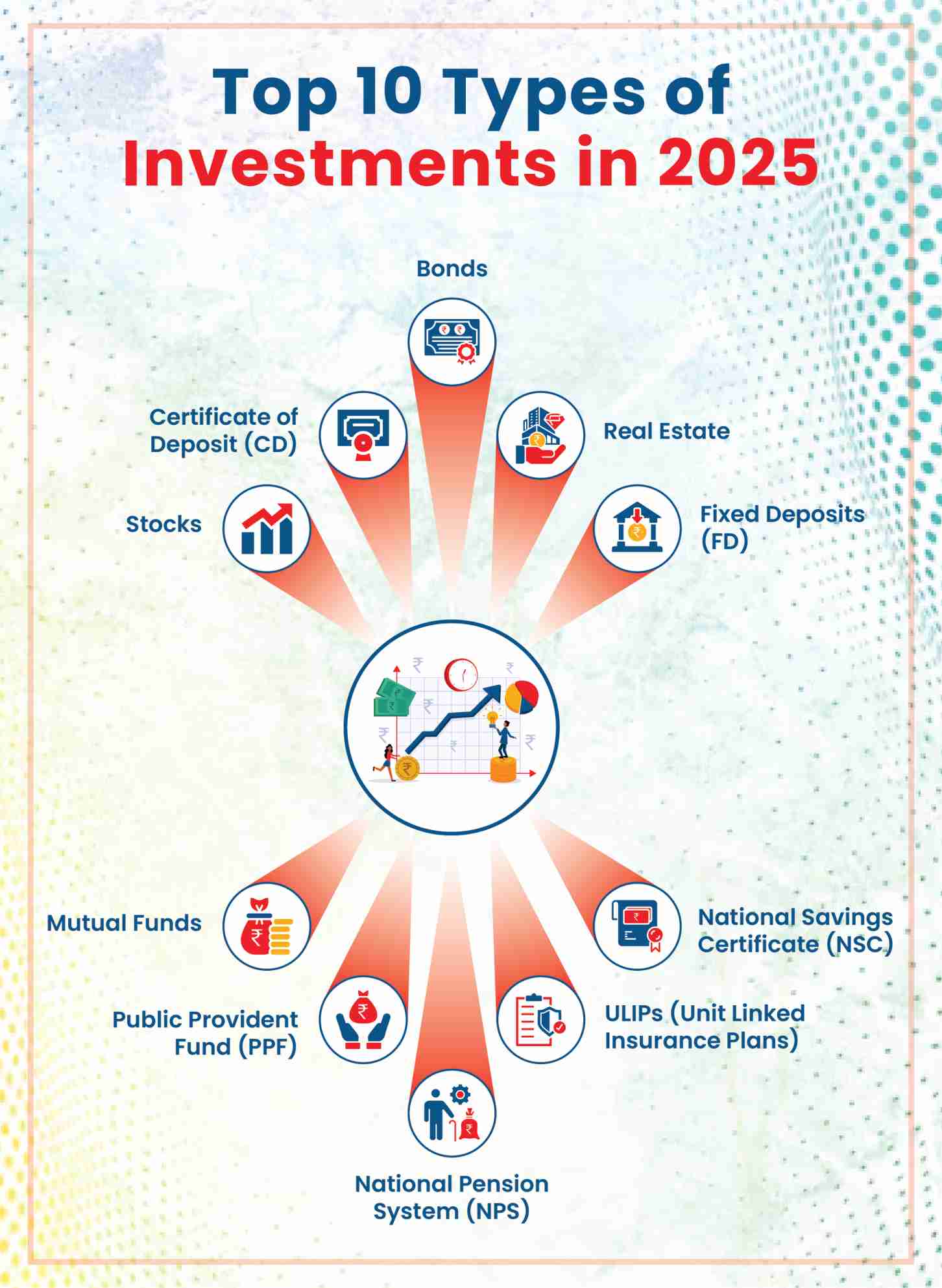

10 Types of Investment in 2025

September 04, 2025

Table of Content

1. List of Types of Investment Plans in India

3. How Does an Investment Plan Work?

4. Why is investing better than saving?

6. Investment Planning for Different Life Stages

8. Things to Keep in Mind While Investing

10. How Can Investing Grow My Money?

11. How to Buy the Right Investment Plan?

12. Identify Suitable Types of Investments for Your Goals

13. Conclusion

List of Types of Investment Plans in India

Sr. No |

Type of Investment |

Returns |

Objective of Investment |

Risk |

1 |

Stocks |

Returns are by way of capital gains and dividends and depend on market performance. |

Wealth accumulation over a period. |

High |

2 |

Certificate of Deposits |

Returns are by way of fixed interest for a particular period |

Fixed returns with capital protection and liquidity. |

Low |

3 |

Bonds |

Returns via fixed or variable coupon rates. |

Stable returns, risk distribution, and capital protection. |

Low to Moderate |

4 |

Real Estate |

Returns are by way of rental income or capital appreciation |

Regular income stream and capital appreciation. |

Moderate |

5 |

Fixed Deposit |

Interest rate locked in for a preferred tenure |

Guaranteed income and capital protection. |

Low |

6 |

Mutual Funds (MFs) |

Returns by way of dividends, interest, and capital gains. |

Wealth accumulation over a period and creating a corpus with small and consistent investments via SIPs. |

Varied (depending on underlying assets) |

7 |

Public Provident Fund (PPF) |

Returns by way of monthly interest and compounded annually. |

Retirement planning, to create a corpus for a financially stable retired life |

Low |

8 |

National Pension System (NPS) |

Variable market linked returns and annuity. |

Retirement planning, creating a corpus and a regular income stream |

Low |

9 |

Unit-linked Investment Plans (ULIPs) |

Market-linked |

Life Cover, Long-term wealth creation, and tax benefits. |

Higher (based on the selected fund's exposure to markets) |

10 |

National Saving Certificates |

Fixed interest |

Assured returns, capital protection feature, and tax benefits. |

Low |

Investing in stocks

Stocks are financial products that give you part of ownership in a publicly listed company. When you purchase shares, you become a shareholder. This means you can benefit in two ways, i.e., capital appreciation when the share price rises and dividends when the company gives away profits.

Being market-associated investments, stock values tend to fluctuate based on the performance of the company and broader economic trends. Stocks are well-suited for long-term investors who can manage moderate to high risk and remain invested despite short-term market fluctuations. Note that equity marketslike the Nifty 50, historically, have delivered inflation-beating returns over long time periods, making stocks an amazing wealth-building financial instrument.

Certificate of deposit (CD)

CDs are basically money market instruments. They are issued by commercial banks and select financial institutions. Such instruments offer fixed returns for a particular tenure. Regulated by the Reserve Bank of India (RBI), CDs are issued in demat form, come with fixed maturity and cannot be withdrawn before the maturity period.

Tenures usually range between seven days and 1 year for commercial banks. And in the case of financial institutions, it is one to three years. The minimum investment is ₹1 lakh with multiples thereafter. CDs are best for investors who are looking for low-risk and fixed-income financial options over the short to mid-term, offering high-level safety, predictable returns, and RBI oversight.

Bonds

Bonds are debt instruments. Here, you lend funds to a government/company in exchange for regular interest payments (i.e., coupons) and repayment of the principal at the time of maturity. Most bonds have fixed coupon rates;however, floating-rate bonds and zero-coupon bonds are becoming more popular.

They are usuallylower riskin nature as compared to equities, which makes them suitable for conservative investors lookingfor steady returns. Investors can purchase bonds directly or via debt mutual funds for added diversification. Government securities (G-Secs), corporate bonds, and tax-free bonds are popular options for balancing out risk and return in a diversified investment portfolio.

Investing in real estate

In real estate investment, you buyphysical property, i.e., residential, commercial or land, with the aim of generating returns via rental income or an increase in property value over a long time. It is usually a long-term commitment that requires considerable capital and ongoing maintenance.

For investors who want exposure to property without owning it directly, Real Estate Investment Trusts (REITs) are a good option. Here, in REITs, investors pool money to purchase and manage income-generating commercial properties as well as distribute rental income as dividends. Traded on stock exchanges, REITs endow diversification and liquidity benefits without the need for owning property directly.

The REIT market in India has grown significantly, particularly in office spaces, driven by high leasing demand. A report mentions India as one of Asia’s fastest-growing REIT markets, alongside China’s 85% market value surge. This growth makes Indian REITs an enticingchoice for investors looking for steady income as well as exposure to commercial real estate with lower capital and better liquidity benefits.

Fixed Deposits (FDs)

An FD is an investment offered by banks that offers assured returns over a fixed tenure. With interest rates locked at the time of deposit, FDs safeguard your capital as well as offer predictable earnings, making them best for risk-averse investors.

Tenures can be short or long, and while premature withdrawals are allowed, they generally attract penalties. FDs remain one of India's most trusted types of investments, offering great safety, flexibility, and stability benefits irrespective of market movements, making them a popular choice for both individuals and businesses lookingto preserve wealth.

Mutual funds (MFs)

MFs are professionally managed schemes that pool funds from investors to make investments in a diversified mix of instruments, namely, equities, debt instrumentsor other securities. Diversification assists in reducing risk while giving access to expert research as well as management.

Equity funds offer high-risk but long-term growth.

Debt funds aim at providinglow risk but steady income.

Hybrid funds balance out risk and return by investing in both equity and debt instruments.

Systematic Investment Plans (SIPs) permit disciplined and small-ticket monthly investingwhileEquity Linked Savings Schemes (ELSS) endow tax benefits as per Section 80C of the Income Tax Act, 1961*. Regulated by the Securities Exchange Board of India (SEBI), MFs are a convenient means to build a diversified portfolio in line with your financial goals.

Public Provident Fund (PPF)

PPF is a government-backed savings scheme. This financial product offers assured returns and a high safety level, making it a favourable instrument for long term investment planning. You can invest from ₹500 up to ₹1.5 lakh on an annual basis, with contributions eligible for deductions as per Section 80C. It has a lock-in of a 15-year period, with partial withdrawals and loans permitted after certain years.

Interest is compounded on an annual basis and computed on the lowest monthly balance between the 5th and the month-end, so depositing before the 5th maximises earnings. Selecting a bank or post office that supports online transfers makes contributions very simple to track, ensuring this investment option works smoothly for wealth building.

National pension system (NPS)

NPS is a low-cost and government-backed retirement plan. This plan is regulated by the Pension Fund Regulatory and Development Authority(PFRDA). Designed for long-term wealth creation, NPS also works well for investors evaluating it as a best investment plan for 5 years or more, especially when tax efficiency and disciplined savings are priorities. With this option, you tend to make investments in equity, corporate bonds, government securities and alternative assets. Investors can zero in on between Active Choice (i.e., self-selected asset allocation) or Auto Choice (i.e., age-based allocation).

At 60 years of age, you can withdraw up to 60% of the corpus (which is tax-free), with the remaining used to purchase an annuity plans to earn regular pension income. The scheme now extends investment up to 75 years of age. Alongside providing Section 80C of the Income Tax Act, 1961 benefits, NPS even endows an additional ₹50,000 deduction as per Section 80CCD(1B) of the Income Tax Act, 1961*, making it a prudent long-term investment strategy for the purpose of retirement planning.

Unit-linked insurance plans (ULIPs)

ULIPs endow dual-benefit clubbing life insurance with market-linked investments. A part of your premium goes towards life cover, and the remaining get invested in equity, debt or hybrid funds, based on your selected risk profile. ULIPs permit fund switching, endowing great flexibility to adjust asset allocation depending on market scenarios.

They come with a five-year lock-in and tax benefits as per Section 80C*. For those looking for both protection and wealth creation in one investment instrument, ULIPs offer a structured and long-term approach to meet life goals while safeguarding family security.

National Savings Certificate (NSC)

NSC is a fixed-income investment backed by the Government, best for small and mid-income investors,highly focused on safety as well as steady returns. Available at post offices in denominations beginning from ₹1,000, NSCs have a tenure of five years.

Interest components get compounded on an annual basis but are paid just at the time of maturity. Investments up to ₹1.5 lakh are eligible for Section 80C deductions, and the reinvested interest (except the final year’s) also qualify as per Section 80C of the Income Tax Act, 1961. With government assurance, fixed returnsand easy accessibility, NSCs come across as a trustworthy option for conservative investors, prioritising capital preservation.

.

What is Investing?

Investing is a simple act of committing your surplus funds or capital to an asset or venture. These assets or ventures may be stocks, bonds, mutual funds, property, or even a business with the expectation of yielding a return over a long time. Such returns can come as periodic income, like interest or dividends, or as capital appreciation when the value of the asset increases.

Unlike saving, which concentrates on keeping funds totally safe with minimal risk, investing aims to grow your parked funds and often involves higher risk. It also differs from speculation, which is basically short-term and driven by market timing, whereas investing is a long-term process and based on research and planning.

How Does an Investment Plan Work?

An investment plan is nothing but a structured way to put your funds in distinct financial instruments so that you can achieve your short-term or long-term goals. It begins with taking stock of where you are at present in terms of your income, expenditures and how much you can set aside for the purpose of investment.

Next, you figure out clear financial goals, like financing your child’s higher education in ten years or retiring at the age of 60 and link a realistic timeline to each. You then examine your risk appetite level, whether you prefer safe options, moderate growth or high-return (or high-risk) opportunities.

Depending on tolerance level, you zero in on appropriate assets, such as fixed deposits for safety, mutual funds for balance or stocks for higher growth potential. Before you start, it is prudent to keep a contingency fund for unanticipated expenditures.

An excellent plan disseminates investments throughout asset classes (diversification) and is assessed on a regular basis to adapt to life changes as well as market trends.

Why is investing better than saving?

AWhile saving keeps your funds totally safe, investing helps it grow, turning today's surplus into tomorrow's wealth. Here's why putting your funds today to work can outshine rather than just parking them in any savings account.

Attaining your financial goals

A savings account is an excellent option for meeting short-term needs like emergencies or upcoming bills. Note that the parked funds cannotgrow quickly enough for bigger dreams requiring a huge corpus.

Think purchasing a flat, paying for your child’s studies to pursue education abroad or retiring comfortably; all these require far more than interest earned on savings can provide.Disciplined investing via SIP mode, retirement fundsor other long-term investment plans steadily builds the wealth required to meet such life goals.

To overcome inflation

Inflation simply means things get costlier over time, i.e., your money today will buy less in the future. Savings accounts usually earn around 3–4% interest, often less than the average inflation rate.

That means your purchasing power is shrinking. Investments like equity mutual funds or ULIPs have the potential to beat inflation, helping your money not just keep up, but grow in real terms.

For significant returns

Savings accounts might yield 3–4% and fixed deposits nearly 6–7% or at times 8%. But long-term mutual fund investments, particularly equity funds, can offer an average return of 10–13% annually. Higher returns come with higher risk,yet prudent and long-term investment balancesthis out well.

All thanks to the compounding effect. By just investing an amount of ₹1 lakh at 10% annual returns, you can attain a total amount of over ₹2.5 lakh in 10 years. This is a growth that you can’t attain with plain savings.

Benefits of Investing

Investing is not just about growing your funds; it is all about securing your financial future, beating inflationand creating a steady flow of income. Let’s understand how investing prudently can make your funds work harder for you.

Growth of money

Investing permits your invested funds to work for you, yielding good returns through capital appreciation as well as reinvested earnings. Owing to the power of compounding, even meagre, consistent contributions can fetch a big corpus.

For instance, investing a small investible amount equaling ₹5,000 per month for a span of 10 years at 10% returns can fetch more than ₹10 lakh, which is far more than just saving.

The impact of inflation

Inflation means the prices of goods keep rising, which lowers the value of your money. Savings accounts can hardly overcome inflation. But investments like mutual funds, particularly in equity funds, can yield higher returns that preserve and grow your buying power, safeguarding your future lifestyle.

Income from other sources

Investments can yield passive income via dividends from shares, rental income from property or interest from bonds. This additional income can top up your salary, support yourpost-retirement, and endow a cushion in times of job loss, health issues or market slowdowns. Moreover, knowing how to save money from salary through investments can help you build a more secure financial future.

A disciplined approach towards finance

Investing on a regular basis builds strong money habits. Setting aside even a minor fixed amount each month not only grows your wealth but also assists you in avoiding impulse spending. Tools like SIPs or recurring deposits make this discipline effortless by automating your contributions.

Tax advantages

Certain financial investments permit you to save taxes while building wealth. Options such as ELSS, NPS, PPFand ULIPs offer tax deductions as per Section 80C* and 80CCD* and exemptions like Section 10(10D) of the Income Tax Act, 1961*. This implies you enjoy the dual advantage of growing money and reducing your tax bill.

Long-term financial security

Financial security means being able to mitigate future requirements with zero need for borrowing or depending on others. Investing assists in building funds for retirement, future exigencies or your child’s higher education. With a pragmatic investment plan, you can manage life's uncertainties well with great confidence and stability.

Investment Planning for Different Life Stages

Your financial goals, as well as your goals, change as you move through life. Personalising your financial strategy to match such stages aids you in growing and safeguarding your wealth at every step. Here's a look at what to concentrate on at each phase, along with apt investment options to guide your planning:

Life stage |

Key characteristics |

Suitable investment options |

Key focus areas |

Early career |

Starting out professionally, low income, high risk-taking ability |

SIPs in equity mutual funds, ELSS, ULIPs (optional), and an emergency fund |

Build savings habit, start early, leverage compounding |

Marriage andfamily |

Increased responsibilities – spouse, kids, loans |

ULIPs, term insurance, child plans, PPF, balanced mutual funds, health insurance |

Financial protection for dependents, plan for the family's future goals |

Mid-career |

Peak earning phase, clearer goals, higher disposable income |

Equity funds, NPS, real estate, tax-saving funds, asset rebalancing strategies |

Maximise returns, long-term wealth creation, plan for retirement and education |

Pre-retirement andretirement |

Preparing for or living post-retirement, fixed income reliance |

SCSS, annuities, debt funds, monthly income plans, liquid funds |

Capital preservation, steady income, focus on healthcare and estate planning |

Early career stage

When you're just starting your career, income may be limited, but your capacity to take risks is high. This is just the right time to begin early and allow compounding work its magic. Factor in high-growth investments, namely equity mutual funds, ELSS, and stock SIPs.

Build the habit with small and regular contributions via SIPs. Keep a contingency fund handy. And also, take up a term insurance in case you have dependents. If you prefer an insurance-cum-investment plan, then ULIPs may be a great fit.

Marriage and family building stage

With marriage and family, responsibilities grow, right from supporting a spouse and children to managing home loans and caring for parents, all must be taken care of really well. Balance out safety and growth by opting for ULIPs, child insurance plans, PPF and balanced mutual funds.

Make sure you hold adequate life as well as health insurance for protection. Begin goal-related investments for your child’s higher studies and your dream home. Maintain a financial cushion via fixed deposits or recurring deposits for meeting exigencies.

Mid-career and wealth accumulation stage

In your peak earning years, make sure you focus on accelerating wealth creation while securing certain goals. Diversify into equity funds, debt funds, NPS and possibly real estate. Assess and rebalance your investment portfolio on a regular basis. Make use of tax-saving tools like NPS and 80C-linked schemes.

Enhance contributions toward your retirement fund and secure higher education funds for kids. Shift a portion of your portfolio from high-risk assets to safer ones if a major goal is nearing.

Pre-retirement and retirement stage

As you are near retirement, the focus shifts to preserving capital andensuring a steady income. Zero in on low-risk options like SCSS, annuities, debt mutual fundsand monthly income plans. Keep funds liquid for medical requirements and daily expenditures.

Maintain a small equity exposure for inflation-beating returns, if you are comfortable with the risk. Plan out your estate by making a will, updating nominationsand setting up inheritance guidelines. Consider long-term healthcare or critical illness coverage if not already in place.

How to Invest?

The do-it-yourself (DIY) investor

If you enjoy researching as well as making your own choices, DIY investing enables you to pick stocks, mutual funds or other assets directly, giving you complete control.

Investments managed by professionals

For those who prefer guidance, professional fund managersmanage your funds in mutual funds or portfolio management services, aiming to maximise returns.

A roboadvisor for investing

Robo advisors utilise algorithms to create and manage your portfolio automatically, offering a low-cost and hands-off means to invest.

Start investing in small amounts

You do not require a huge sum to start. Begin small with options like SIPs or micro-investing apps and grow your wealth in a steady way over a long time.

Things to Keep in Mind While Investing

Before you make any investment, understanding basic principles assists you in making smarter and goal-aligned decisions that match your risk comfort and timeline.

Beware of your risk tolerance level

Risk tolerance level is how comfortable you are with potential losses. It changes with age, income, and goals, so match up your investments accordingly.

Line up investments with your goals

Break your life goals into short, medium and long term. Zero in on investments that match each timeline to remain disciplined and easily track your progress.

Use online investment calculators

Online investment calculators estimate returns for SIPs, FDs or retirement plans that assist you in comparing options and planning better before investing. Additionally, a lumpsum calculator can be a useful tool for evaluating the growth of one-time investments, helping you assess how your funds can perform over time.

Diversify your portfolio

Disseminating your investments throughout distinct assets to lower risk. Avoid depending too much on one financial product to safeguard your money.

Plan for retirement early

Beginning early enables compounding to grow your retirement corpus. Consider products like PPF, NPSand pension plans to secure your future.

Review your investments regularly

Check out your investment portfolio at least once a year to make sure it matches your life goals and adapts to market changes.

How Can I Start Investing?

Beginning your investment process is simpler than you think. Start by understanding your goals, risk comfort level and how much you can set aside on a regular basis. No matter whether you choose to invest directly or seek professional help, the key is to take that first step and remain consistent.

How Can Investing Grow My Money?

Investing puts your money to work, whichassists it in growing through capital appreciation and income, such as dividends or interest. Over a long time, this growth, boosted by compoundingeffect, can multiply your savings far beyond what simple savings offer, assisting you in attaining bigger goals.

How to Buy the Right Investment Plan?

Zeroing in on the correct investment plan begins with understanding your goals, risk comfort level and financial scenario, so you can make prudent and confident decisions that work for you.

Define your goals

Begin by clearly stating what you want to attain, whether it is purchasing a flat, financing education or planning out for post-retirement days. Distinct goals require different investment tools based on risk, return and time.

Goal-based investing keeps you disciplined as well as motivated, with options like retirement funds, child plans or ULIPs personalized to your needs.

Understand time constraints

Consider how long you plan to keep your funds invested, as this has an impact on the types of investments suitable for you.

Think about your budget

Examine how much you can comfortably invest with zero need for straining your finances, beginning small if required.

Decide on your risk appetite level

Know your comfort level with market ups and downs to pick investments that match your risk profile.

Evaluate liquidity needs

Liquidity means how quickly you can convert your investments into cash. Think about whether you might need funds for financial exigencies or life events.

Zero in on liquid options like mutual funds or savings accounts if you require easy access and be cautious about locking funds into long-term options like PPF, real estate or ULIPs.

Figure out the suitable investments for your goals

Match up your goals with the correct investment types. Short-term goals might call for safer and liquid assets. However, long-term ambitions can benefit from growth-oriented options like mutual funds, particularly equities.

Identify Suitable Types of Investments for Your Goals

With this guide, you can get started creating your financial plan for different types of investments in India. Investing your money in various types of investments can ensure that your funds are placed in instruments that can help you achieve your short-term and long-term financial objectives. While short term investment plans help meet near-term goals with easy access to funds, long-term investments are more suitable for building wealth and planning for key life stages like retirement. Financial planning is also an excellent way to prepare for retirement, so you can eventually step away from the daily grind and find time to pursue your dreams in your retirement years, whether it's something as simple as picking up a new hobby or something as grand as travelling the world. There are several forms of investment plans you can choose from as per your financial goals –

Conclusion

There is a wide spectrum of investment avenues, ranging from traditional fixed-income tools to market-linked instruments. Low-risk options like one-time investment plans, PPF, NSC, and fixed deposits are best for conservative or first-time investors, while equities, mutual funds and ULIPs suit those with higher risk tolerance levels and investment experience.

Selecting the correct investment depends on individual factors such as age, income, risk appetite, liquidity needsand long-term goals. Since there is no universal plan, investors must examine options very carefully, avoid impulsive decisions and prioritise their financial objectives. Discipline and periodic portfolio reviews are key to remaining on the right track and attaining life goals.

FAQs on Types of Investment

What is investment and its type?

What are the 7 types of investment?

What are the four types of investing?

What are the 6 classifications of investments?

What are the three investment categories?

What are the key points one should consider before investing in India?

Which type of investment is best for beginners?

How to choose an investment type based on risk tolerance?

Investment is allocating funds into various assets to generate yields over time. The various types of investments are equity, bonds, mutual funds, ULIPs, commodities (gold, silver, etc), Cryptocurrencies, real estate, fixed deposits, PPF, NPS, Certificate of Deposits, National Savings Certificate, etc.

Among the top 7 types of investments are stocks, bonds, mutual funds, property, money market funds, retirement plans, and insurance policies.

Bonds, stocks, Mutual Funds, and ULIPs are the four main types of investments.

Active versus passive management, growth versus value investing, and small or large companies are the 6 classifications of investments.

The three investment categories are:

1. Ownership such as investment in stocks of companies, real estate, and commodities like gold and silver.

2. Lending includes investment in bonds, which are loans to government entities or businesses.

3. Cash includes investments in liquid assets like treasury bills, money market accounts, savings accounts, etc.

1. Your investment goal should be clear.

2. Make sure you know how long you are planning to invest.

3. Be aware of your risk tolerance.

4. Allocation of assets is important.

5.Make sure you know which product to invest in.

The best types of investment for beginners are high-yield savings accounts like fixed deposits and options with guaranteed returns such as PPF, NPS, etc.

Assess how much loss you can comfortably handle. Conservative investors prefer fixed income, moderate investors mix debt and equity. However, aggressive investors concentrate more on equities for higher growth.

Similar Articles

- Tax Saving Investment Options for Tax-Free Income in 2021

- Compare Investment and Savings Plans

- A Beginner's Guide to Investment Plans

- Safe investment with high returns in India

- Investment in Gold – viability and liquidity!

- Long Term Investment

- Short Term Investment

Not sure which insurance to buy?

Talk to an

Advisor right away

Advisor right away

We help you to choose best insurance plan based on your needs

Francis Rodrigues

Francis Rodrigues

Francis Rodrigues has a decade long experience in the insurance sector, and as SVP, E-Commerce and Digital Marketing, HDFC Life, manages the online sales channel, as well as digital and performance marketing. He has had hands-on experience in setting up sales channels and functional teams from scratch over a career spanning 2 decades.

Here's all you should know about life insurance.

We help you to make informed insurance decisions for a lifetime.

HDFC Life

Reviewed by Life Insurance Experts

HDFC LIFE IS A TRUSTED LIFE INSURANCE PARTNER

We at HDFC Life are committed to offer innovative products and services that enable individuals live a ‘Life of Pride’. For over two decades we have been providing life insurance plans - protection, pension, savings, investment, annuity and health.

Popular Searches

- Term Insurance Calculator

- Investment Plans

- Investment Calculator

- Investment for Beginners

- Best Short Term Investments

- Best Long Term Investments

- 5 year Investment Plan

- savings plan

- ulip plan

- retirement plans

- health plans

- child insurance plans

- group insurance plans

- income tax calculator

- bmi calculator

- compound interest calculator

- income tax slab

- Income Tax Return

- what is term insurance

- Ulip vs SIP

- tax planning for salaried employees

- HRA Calculator

- Annuity From NPS

- Retirement Calculator

- Pension Calculator

- nps vs ppf

- short term investment plans

- safest investment options

- one time investment plans

- types of investments

- best investment options

- best investment options in India

- Term Insurance for Housewife

- Money Back Policy

- 1 Crore Term Insurance

- life Insurance policy

- NPS Calculator

- Savings Calculator

- life Insurance

- Gratuity Calculator

- Zero Cost Term Insurance

- critical illness insurance

- itc claim

- deductions under 80C

- section 80d

- Whole Life Insurance

- benefits of term insurance

- types of life insurance

- types of term insurance

- Benefits of Life Insurance

- Endowment Policy

- Term Insurance for NRI

- Term Insurance for Women

- Term Insurance for Self Employed

- Benefits of Health Insurance

- Health Insurance for Senior Citizens

- Health Insurance for NRI

- term insurance

@Save 46,800 on taxes if the insurance premium amount is Rs.1.5 lakh per annum and you are a Regular Individual, Fall under 30% income tax slab having taxable income less than Rs. 50 lakh and Opt for Old tax regime.

@@Provided all due premiums have been paid and the policy is in force.

This material has been prepared for information purposes only, should not be relied on for financial advice. You should consult your own financial consultant for any financial matters.

~ This is the return of the benchmark index fund and not indicative of HDFC Life Top 300 Alpha 50 fund performance (SFIN - ULIF07828/02/25Alpha300Fd101). Source: https://www.nseindia.com/

In unit linked policies, the investment risk in the investment portfolio is borne by the policyholder. The Unit Linked Insurance products do not offer any liquidity during the first five years of the contract. The policyholders will not be able to surrender/withdraw the monies invested in Unit Linked Insurance Products completely or partially till the end of fifth year. The name of the company, name of the brand and name of the contract does not in any way indicate the quality of the contract, its future prospects or returns.

Unit Linked Funds are subject to market risks and there is no assurance or guarantee that the objective of the investment fund will be achieved.

Unit Linked Insurance Products (ULIPS) are different from the traditional insurance products and are subject to the risk factors. The premium paid in the Unit Linked Life Insurance Policies is subject to investment risks associated with capital markets and the NAVs of the units may go up or down based on the performance of fund and factors influencing the capital market and the insured is responsible for his/her decisions. Please know the associated risks and the applicable charges, from your insurance agent or the intermediary or policy document of the insurer. The various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns.

* Tax benefits & exemptions are subject to the conditions of the Income Tax Act, 1961 and its provisions. Tax Laws are subject to change from time to time. Customer is requested to seek tax advice from his Chartered Accountant or personal tax advisor with respect to his personal tax liabilities under the Income-tax law.

The Unit Linked Insurance products do not offer any liquidity during the first five years of the contract. The policyholders will not be able to surrender or withdraw the monies invested in Unit Linked Insurance Products completely or partially till the end of fifth year.

Unit Linked Life Insurance products are different from the traditional insurance products and are subject to the risk factors. The premium paid in Unit Linked Life Insurance policies are subject to investment risks associated with capital markets and the NAVs of the units may go up or down based on the performance of fund and factors influencing the capital market and the insured is responsible for his/her decisions. HDFC Life Insurance Company Limited is only the name of the Insurance Company, The name of the company, name of the contract does not in any way indicate the quality of the contract, its future prospects or returns. Please know the associated risks and the applicable charges, from your Insurance agent or the Intermediary or policy document of the insurer. The various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans, their future prospects and returns.

** The returns mentioned is the 5-year benchmark return percentage of NIFTY India Consumption Index data as of 31st Oct, 2025, and is not indicative returns of India Consumption Advantage Fund (ULIF08421/11/25InCnsmAdFd101)

ARN- ED/08/25/25982