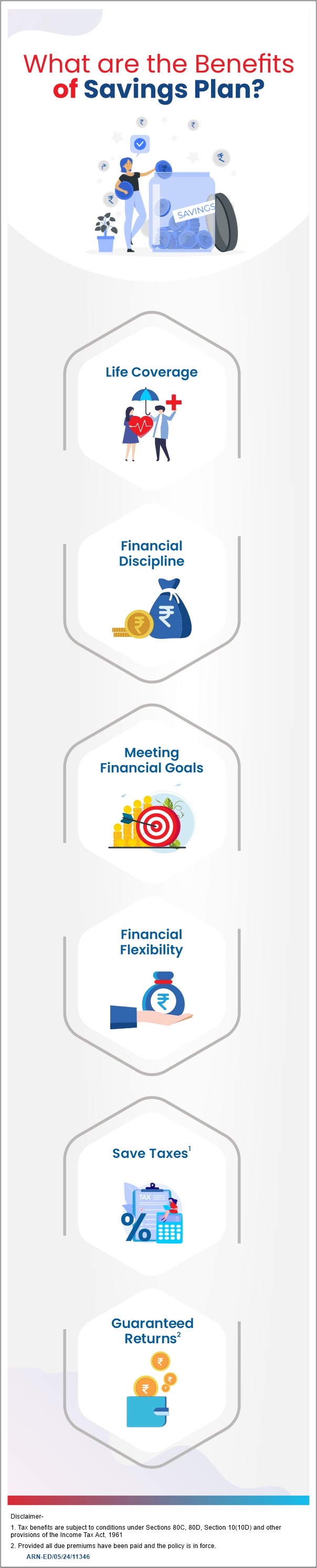

Importance of Buying the Best Savings Plan

A savings plan is not just a route where you set surplus funds aside and forget; it is more than this. It is a means that enables you to safeguard your hard-earned money, build substantial wealth steadily, and prepare for life’s uncertainties. A guaranteed savings insurance plan, in particular, offers the dual benefit of financial protection along with assured returns, making it a dependable choice for disciplined savings.

By aligning with your goals, Savings plans can support everything, right from your day-to-day requirements to your long-term aspirations, such as post-retirement life or your child’s higher education/wedding.

When you explore how to save money effectively, the right savings plan acts as a blueprint, helping you stay on track and work towards your financial milestones. Beyond numbers, the reassurance of having a structured savings pathway brings mental peace and utter financial confidence.

Security and Protection of Your Funds

A savings plan helps protect your money from impulsive spending or unplanned decisions. By investing regularly in such plans, you ensure not only capital preservation but also easy access whenever the need arises.

Gradually, you also build a strong financial foundation for everyday stability while also securing your financial future.

Potential for Higher Growth

Savings plans provide assured or market-associated returns, which can offer better growth in comparison to traditional savings options. This growth accelerates your ability to attain milestones.

These milestones may be buying a flat, financing your kid's higher studies or planning a retirement corpus. With the correct financial preparation, your investible funds in a savings plan with life insurance are put to better use and work harder for you.

Flexibility to Adjust Goals

Life priorities tend to change as you move ahead in life due to growing responsibilities and nd savings plans can help you adapt with them. You can do so by prudently adjusting your contributions, switching investment allocations or modifying certain benefits.

This kind of flexibility helps your financial planning to stay on track and continues to provide the financial support you need through distinct life phases.

Building Healthy Financial Habits

Making regular contributions to a savings plan develops great discipline in managing money. Over time, this habit assists you in building a rock-solid emergency fund.

Also, the insurance savings plan improves your financial resilience and promotes long-term stability, which keeps you on track with your goals(i.e., five years or above).

Protection Against Inflation

Certain savings plans are tailored to deliver returns that keep pace with or even beat inflation. This safeguards your buying power, which ensures you can comfortably mitigate your future expenditures with zero need for compromising on the quality of your life.