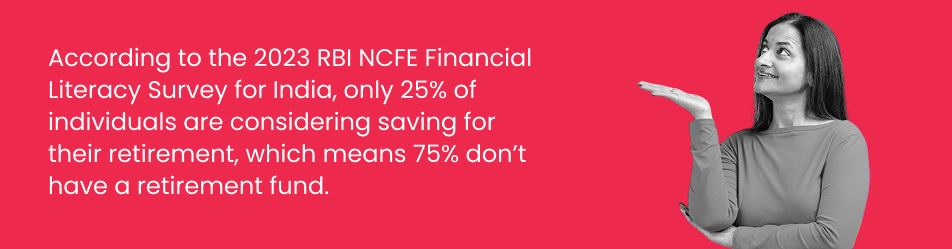

The total pension assets of India amount to approximately ₹ 49 lakh crore, which accounts for just 16% of the country's GDP. For other members of the Organisation for Economic Co-operation and Development (OCED) countries, pension assets accounted for 82% of their total GDP. The gap is enormous!

At 45, you need to have a pension plan in place if you want a peaceful and stress-free post-retirement life and not be part of the 75% that doesn’t have a backup plan for their senior years.

Importance of Starting Your Retirement Journey Early

If you start your investment journey at 45, it will take a lot more to catch up on your retirement corpus than for an average person who starts their journey in their early 30s.

To simplify how it matters when you start your retirement planning, here is a sample plan for two individuals—aged 35 and 45, respectively. Just by starting your investment ten years early, the person aged 35 will make more than three times as much as the person aged 45, thanks to the power of compounding.

For consistency, we have assumed the ROI to be 10%. The assumed investment period for the person aged 35 is 25 years, and for the person aged 45, it is 15 years

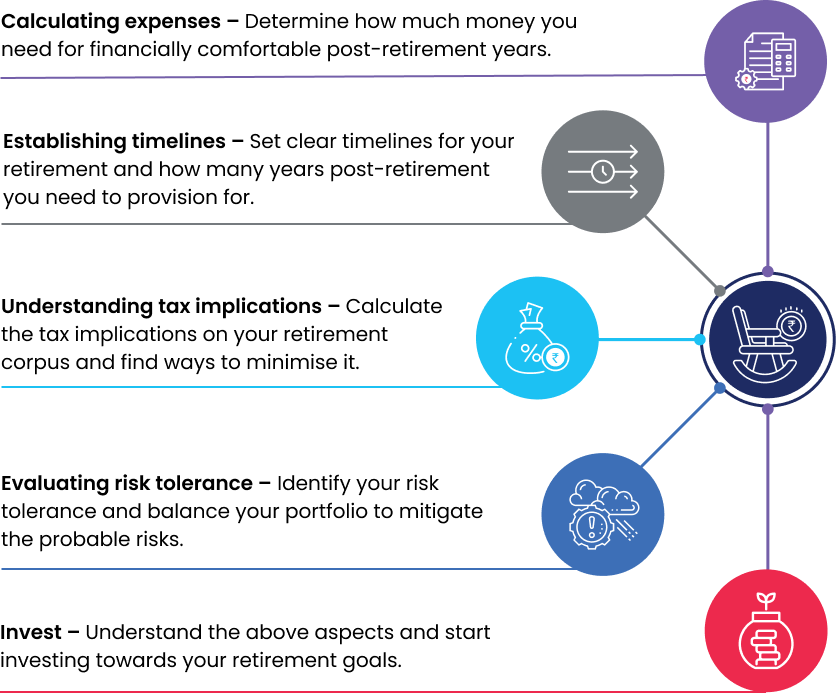

Check Your Retirement Readiness Quotient

Consider this your guide to getting retirement-ready and navigating these pivotal years with confidence and foresight. Here’s what you need to do to check your retirement readiness.

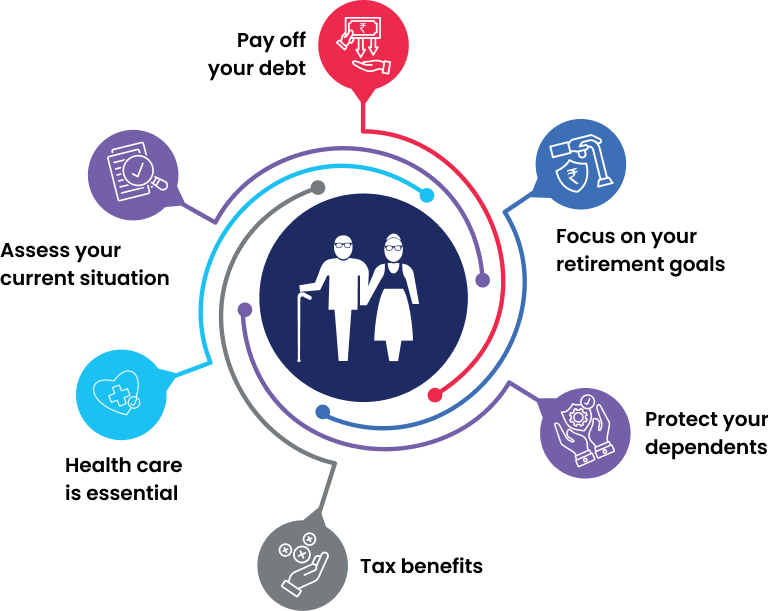

Assess your current situation

Take a hard look at your pension or retirement plan. Are you putting in enough each month? Can you add more?

Check out what you've saved so far by looking at your pension plan statements. These plans are the foundation of your financial future, so add up all your contributions. Assess whether you are on track and calculate how much you need based on your current expenses. Depending on what you have and how much you need, you will have to make adjustments.

And if you still need to start saving, start now. Don't wait – boost your pension and retirement plans and prepare for the future.

Pay off your debt

Tackle any debt that you have head-on. At 45, you need to ditch any lingering debt, as you are closer to retirement than before. Whether it is credit card debt, home loan, or car loan, aim to wipe that slate clean. Avoid taking on new debt at this stage – resist the urge to splurge through credit cards or personal loans. Paying off debt before retirement is crucial for peace of mind.

Focus on your retirement goals

Keep your financial goals separate and focused. Stay on track and avoid jeopardising your long-term financial security by dipping into retirement savings for other goals. This is the time to step up and maximise your pension plans, as they can help secure your financial future and a strategic approach to increasing the income you may receive from your pension plan during retirement. Focus on increasing your annual retirement plan by 10% every year from here on. Maximising your pension plan can lead to a more comfortable retirement.

Protect your dependents

Invest in a sturdy life insurance plan to provide financial protection for surviving spouses or dependents in the event of your death. This will ensure your investments, including your retirement corpus, are safe, and you won't have to dip into your retirement savings in case of any financial crunch.

Tax benefits

Investing towards your retirement in National Pension Scheme (NPS), Public Provident Fund (PPF), Equity Linked Savings Scheme (ELSS) mutual fund, Unit Linked Insurance Plans (ULIPs), etc, offers various tax benefits as per the Income Tax Act of 1961. Your premiums are eligible for tax deductions of up to Rs 1,50,000 under sections 80C, 80CCD, and others under the old tax regime.

Health care is essential

With healthcare expenses increasing, preparing for medical bills during retirement is crucial. Look into health insurance plans and establish an emergency fund specifically for unexpected medical needs. Given increasing life expectancies and rising living costs, optimising your healthcare benefits is crucial to safeguarding your financial well-being and mitigating the risk of outliving your retirement savings.

Maintain your optimism and stay focused on your objectives. This stage of life is a chance to grasp opportunities and pave the way for a prosperous future. Various pension systems in India offer financial security through consistent income post-retirement, provide freedom to customise and offer tax advantages up to Rs 1,50,000 under relevant sections of the old tax regime. By managing your finances, prioritising debt repayment, and maximising retirement contributions, you are building the foundation for a rewarding retirement.

https://www.pfrda.org.in/writereaddata/links/inaugural%

20adress%20by%20chairperson%20-iiml%2022jun2024d6812902-6358-496c-84f1-328c4b8342f0.pdf