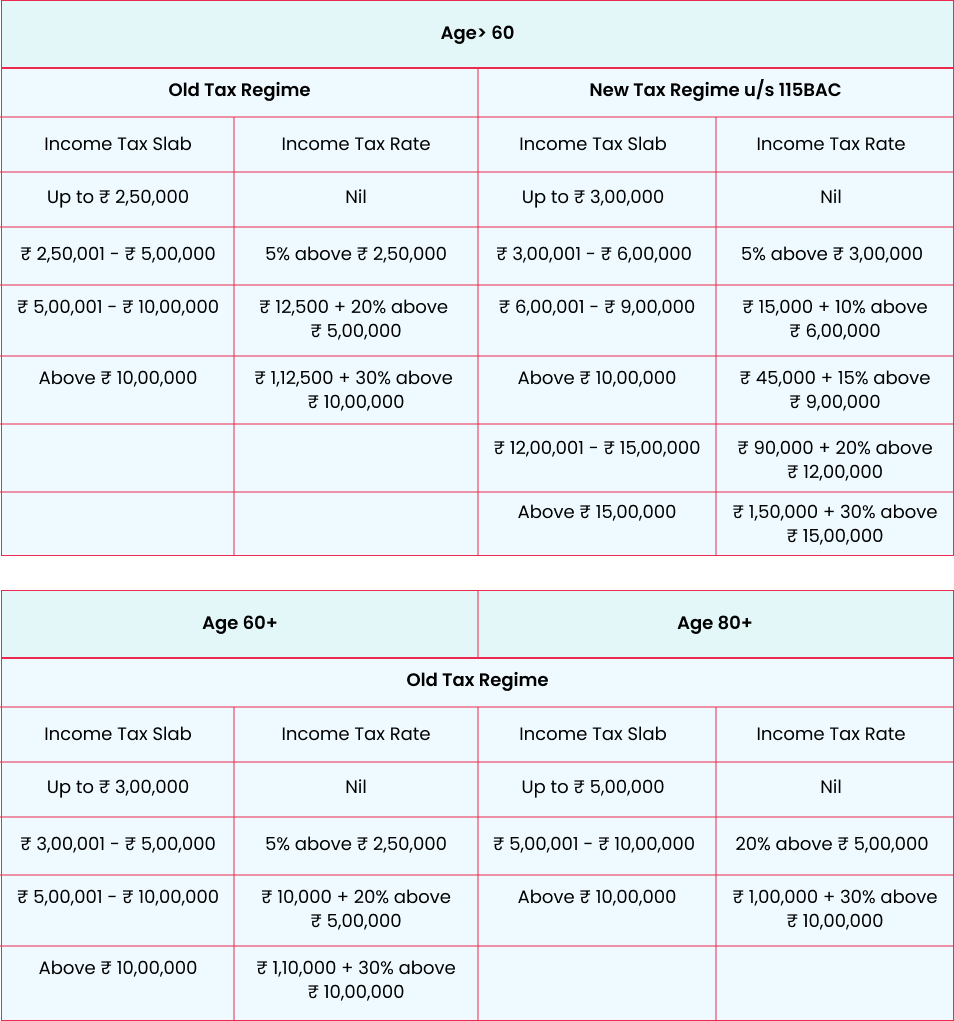

Income Tax Slabs in India

You are liable to pay taxes only if your annual income falls under a specific income slab. To understand tax planning, you need to know which tax slab you fall under. Indian citizens have the option to choose from two regimes, the new tax regime and the Income Tax Act 1961 (old tax regime.) Here is a brief comparison of the income tax slabs, you can work on tax planning once you determine which tax bracket you fall under.

Once you know your tax slab, then comes the choice – which tax regime works best for you. You can make that choice based on the deductions and exceptions you want to declare to reduce your tax burden.

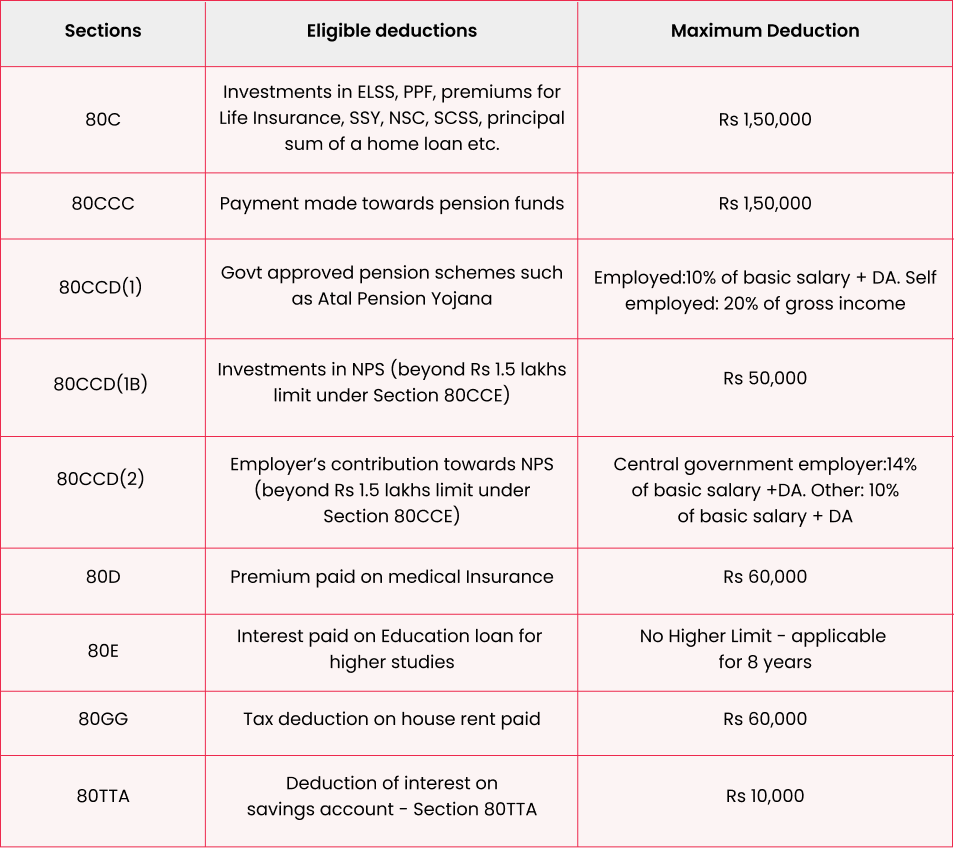

Tax Deductions

Deductions can be claimed by salaried and non-salaried to reduce the total taxable income. A deduction is a tax benefit that can be applied to lower taxable income. This deduction may represent either income or any expense incurred. The deduction amount is deducted from your annual earnings to determine your taxable income and, consequently, you are levied income tax on the remaining income.

Here is a list of income tax deductions that can help you save your tax liability.

Refer to the list of eligible deductions in the table shared above and claim deductions after reducing the applicable deduction amount from your gross income. The remaining amount is your taxable income.

How to Use Investments to Save Tax Liability

Here’s how you can invest to save taxes and prepare for life post retirement:

Retirement Plan

Investing in a retirement plan is non-negotiable, especially if you wish to maintain your current standard of living. Due to healthcare advancements, the average life expectancy in India has increased to 70.62 years. This requires you to be further prepared financially. And unless you come from wealth, the best way to address this predicament is to invest in a robust pension program. You can choose from choose from retirement mutual funds or a National Pension Scheme (NPS). These schemes allow you to claim an annual deduction of Rs. 1.5 lakhs under section 80CCD and an additional 50,000 under section 80CCD(1B).

Long-term Investments

If you wish to invest and save taxes, then long-term investments are your best bet. You can choose from Equity Linked Saving Scheme (ELSS) mutual funds, Unit Link Insurance Plans (ULIPs), or Public Provident Fund (PPF) for tax saving strategies. You can claim upto Rs. 1.5 lakhs deductions annually under Section 80C under the old tax regime.

Insurance

Though you will not create wealth, but insurance, whether it is life or health, will give you ample peace of mind and protection for your loved ones. Life insurance will facilitate the financial well being of your dependents in case of your untimely death and provide financial aid to you and your family in case of medical emergencies. Your loved ones will be protected from any financial burden in both cases. Life insurance policies offer upto Rs. 1.5 lakhs deductions under section 80CCD (both old and new tax regime) and health insurance offers upto Rs. 25,000 under section 80D of the old tax regime.

https://www.incometax.gov.in/iec/foportal/help/individual-business-profession

https://timesofindia.indiatimes.com/blogs/spreading-light/income-tax-law-applicability-in-india-to-individuals-regressive-and-unjust/